Plante Moran released its 2026 Working Relations Index (WRI) study on May 18, and the headline result is one that hasn’t happened in the study’s 26-year history: all six major North American OEMs improved their supplier relations scores. Toyota, Honda, GM, Nissan, Ford, and Stellantis all moved up.

That’s notable not because of the direction -- improvement is always the goal -- but because of the context in which it happened. The survey was conducted from March through mid-April 2026, a period in which suppliers were navigating tariff uncertainty, EV-related cost write-offs, and the early economic fallout from the Iran war. This wasn’t a year of calm waters and easy wins. Suppliers gave higher marks despite operating under more pressure than usual.

The WRI study, founded in 2001 by Dr. John Henke and acquired by Plante Moran in 2019, surveys Tier 1 supplier executives about their working relationships with the six OEMs. This year’s sample was the largest ever: 750 responses (up from 665 in 2025), representing 78 of the top 100 North American automotive suppliers and covering 2,348 buying situations. Suppliers also submitted more than 10,000 written comments -- more than three times the roughly 2,800 received in prior years.

The study is one of the few empirical benchmarks that tracks how automakers actually treat the companies that build their vehicles. And 26 years of data show a consistent correlation: OEMs with stronger supplier relations earn better commercial outcomes -- more favorable pricing, earlier access to new technology, and preferential capacity allocation when supply is tight.

Here’s what the 2026 numbers show.

The Scores

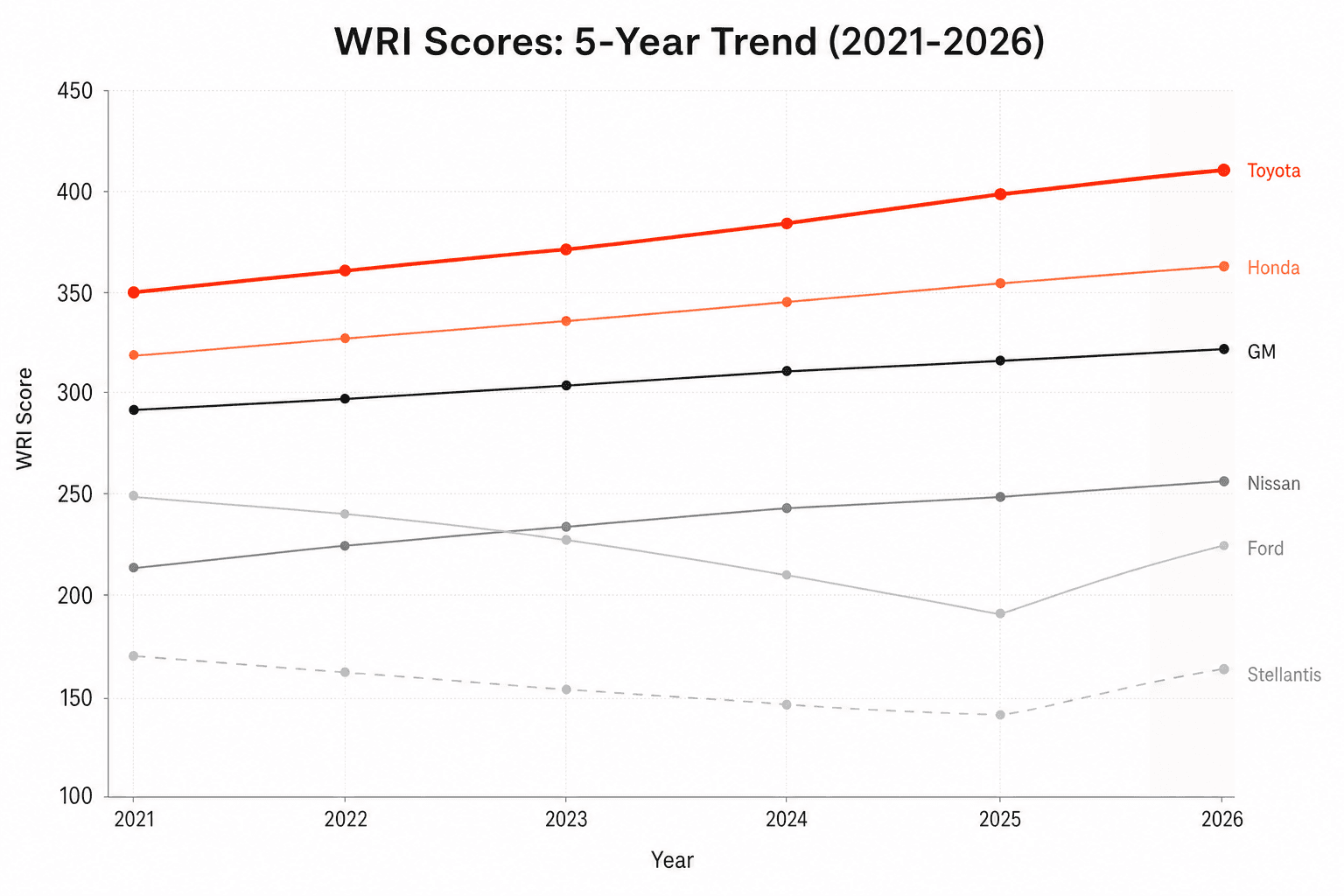

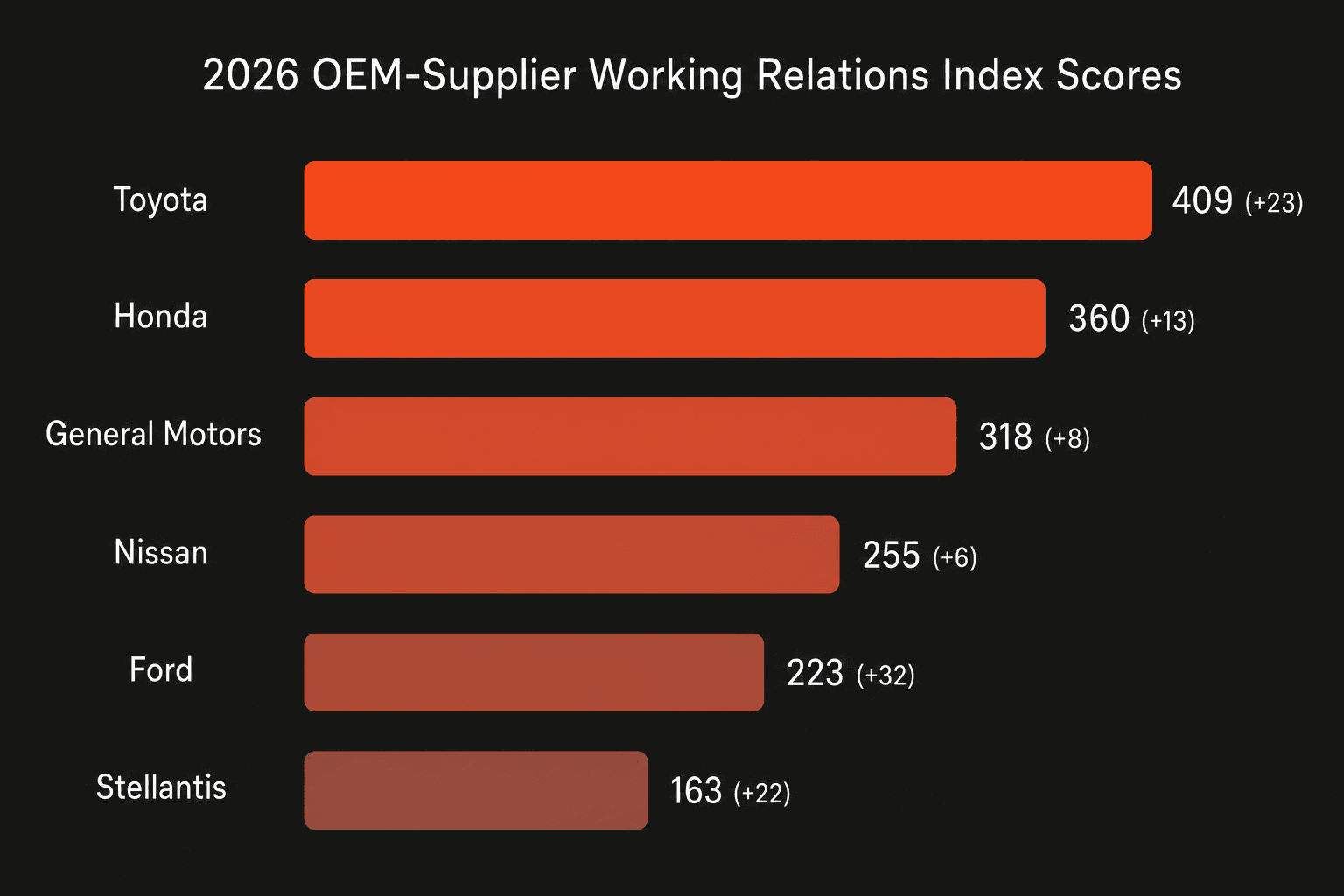

Rank | OEM | 2026 Score | YoY Change | Historical Context |

|---|---|---|---|---|

1 | Toyota | 409 | +23 | Highest since 2007; second-best score ever (415 in 2005 and 2007) |

2 | Honda | 360 | +13 | Highest since 2007; entered the study’s “good to very good” range |

3 | GM | 318 | +8 | All-time high WRI score |

4 | Nissan | 255 | +6 | Matches 2024 level; best since 2014 |

5 | Ford | 223 | +32 | Second-largest single-year jump in company history (largest was 41 points in 2008-2009) |

6 | Stellantis | 163 | +22 | Best score since 2021 |

The gap between first and last is still 246 points. Toyota’s score is more than double Stellantis’s. But the direction matters: every OEM moved in the same direction for the first time since the study began.

Ford’s 32-point jump stands out. That’s not a statistical wobble -- it’s the kind of move that reflects organizational change. Honda’s return to the “good to very good” category and GM’s all-time high are equally significant, even if the point changes are smaller.

What Drove the Improvement

Dr. Angela Johnson, the Plante Moran principal who leads the study, identified four areas where suppliers reported better perceptions across the board.

Long-Term Profit Ability

Toyota maintains the frontrunner position on suppliers’ confidence in long-term profitability. But Ford, Stellantis, and Nissan showed strong gains here -- a signal that suppliers are becoming more optimistic about these OEMs’ strategic direction, even if short-term margins remain pressured.

Commercial Fairness and Cost Management

This is the area most directly shaped by macro conditions. Tariffs and EV cost recovery were the two biggest factors influencing suppliers’ perceptions of fairness. Purchasing teams that lacked full control over how much their OEM absorbed those costs compensated by leaning into relationship-building behaviors within their control.

Ford and Stellantis posted the largest gains in fairness perceptions. Toyota and Honda led in cost reduction support. GM made the biggest advances in sunk cost and EV recovery coverage -- though it faced pushback from suppliers on supply chain resiliency initiatives.

Buyer Performance

Accessibility, engagement, and responsiveness improved across all six OEMs. The study notes that return-to-office mandates contributed to this: more buyers physically in the office meant more availability for supplier meetings and issue resolution. Issue resolution ability -- the capacity to actually fix problems, not just acknowledge them -- showed the strongest gains.

This is one of those areas where the sourcing bottleneck matters. When buyers are overwhelmed with manual processes, responsiveness suffers. When the operational load is lighter, they can invest more in supplier relationships.

Communication and Trust-Building

Toyota and Honda continue to lead in trust metrics. Ford and Stellantis made the biggest jumps. Ford’s Liz Door was noted for the largest trust improvement among purchasing chiefs -- a result tied to increased transparency and proactive communication with the supply base.

Dr. Johnson observed: “In 2026, all six automakers improved trust scores through enhanced communication, accessibility and their ability to solve problems.”

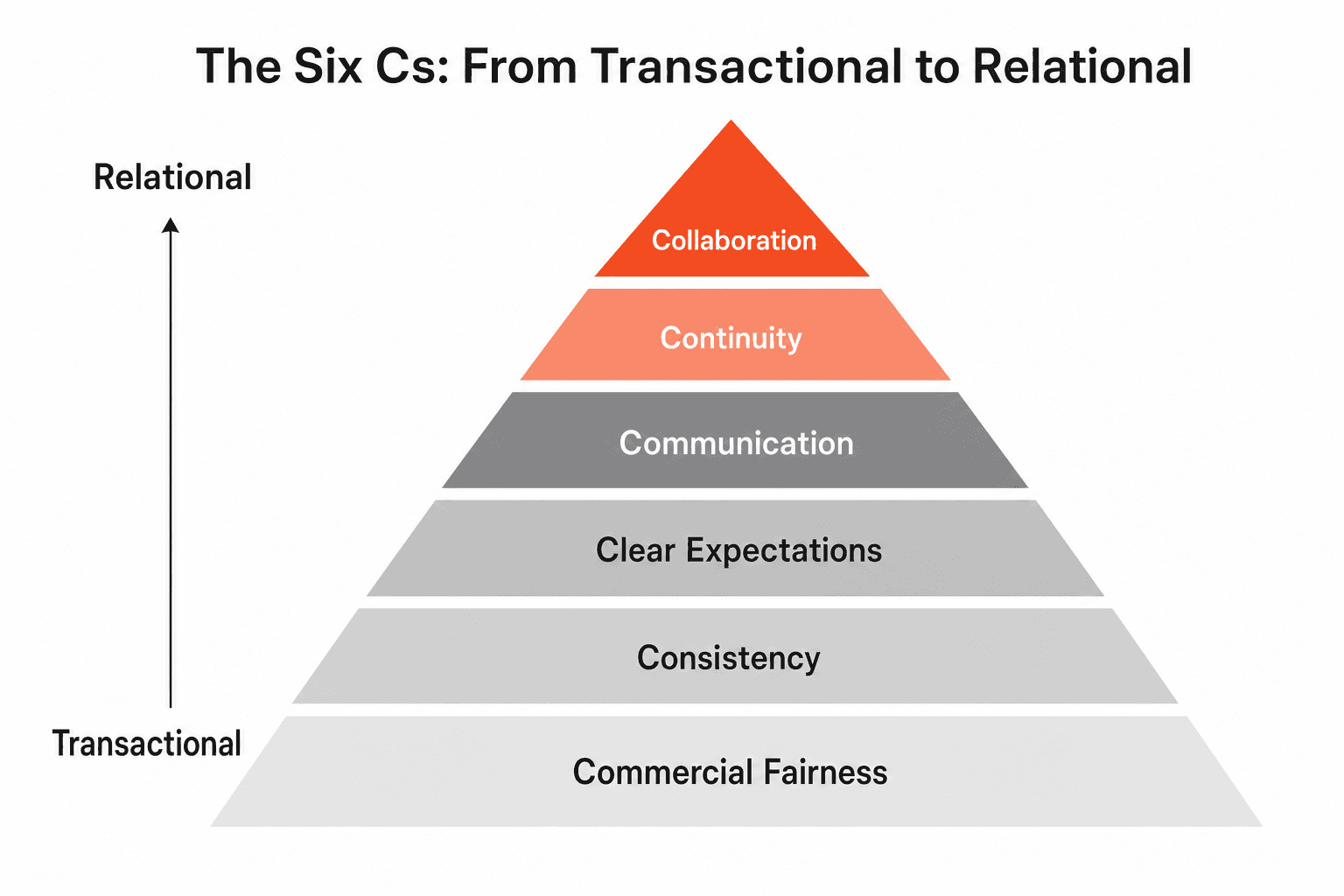

The Six Cs: What Separates Top from Bottom

The study introduced a framework Dr. Johnson calls the “Six Cs” -- controllable behaviors that distinguish OEMs with strong supplier relations from those still building trust. She describes them as a pyramid, progressing from transactional to relational:

Commercial fairness -- equitable risk and cost sharing. The foundation.

Consistency -- longer-term scheduling and production plans that suppliers can actually build capacity against.

Clear expectations -- unambiguous requirements. Not shifting goalposts.

Communication -- proactive, clear, simple messaging. Not email storms with no context.

Continuity -- long-term OEM-supplier strategy that survives leadership changes.

Collaboration -- genuine joint problem-solving. The top of the pyramid.

The insight here is that the behaviors at the bottom of the pyramid (commercial fairness, consistency) are necessary but not sufficient. OEMs that excel on those basics but fail on communication and collaboration still don’t earn top marks. The suppliers who rated OEMs highest credited them for demonstrating all six.

This framework maps directly to what we see in supplier performance management more broadly: the relationship between a buyer and supplier isn’t just a set of commercial terms. It’s an operating system that either enables or constrains both parties.

The Top 50 Supplier Perspective

The study breaks out ratings from the Top 50 North American suppliers separately -- and the results tell a different story from the overall averages.

Top 50 suppliers rated Nissan, Honda, and Toyota above their overall averages. They rated GM, Stellantis, and Ford below their respective averages. The disparity was most noticeable in measures of trust, communication, and profit opportunity.

Why? Two reasons.

First, these are the suppliers with the deepest relationships and the most at stake. They’ve been through multiple OEM leadership cycles, restructuring programs, and strategic pivots. Their ratings carry more institutional memory -- both positive and negative.

Second, the tariff and EV cost recovery impacts hit Top 50 suppliers harder. Larger suppliers carry more exposure to commodity price swings, tooling amortization on canceled EV programs, and the logistics disruptions discussed in the Hormuz crisis. Their assessments of commercial fairness are grounded in larger dollar figures and higher-stakes negotiations.

Dr. Johnson put it directly: “Organizational memory is very long. The Detroit Three are still fighting to overcome the cultural inertia of historically adversarial purchasing organizations.”

That doesn’t discredit the progress. All six OEMs improved even in the Top 50 segment. But it does explain why Toyota, Honda, and Nissan -- OEMs with historically collaborative supplier cultures -- continue to outperform on relationship metrics even when their commercial terms aren’t always the most generous. For a deeper analysis of what this perception gap reveals about institutional memory and why mid-tier supplier responses may be the more useful leading indicator, see What Suppliers 51-100 Tell You That the Top 50 Won’t.

The Permacrisis Effect

One of the study’s most interesting findings isn’t in the scores. It’s in the comments.

Suppliers submitted more than 10,000 written comments this year -- more than triple the roughly 2,800 received in prior years. Dr. Johnson noted: “We saw an emerging, collective recognition that working together is the best way to face permacrisis challenges, innovate, and grow.”

The word “permacrisis” keeps showing up in procurement circles, and the WRI data suggests it’s changing supplier behavior. When the external environment is volatile -- tariffs shifting, raw materials spiking, geopolitical disruptions hitting shipping lanes -- suppliers appear to credit OEMs more for the effort of trying, even when outcomes aren’t perfect.

As Dr. Johnson observed: “Suppliers appeared to acknowledge efforts OEMs made over the past year to control what they could and to help suppliers navigate industry uncertainty. Even if suppliers didn’t experience their ideal outcome, they credited the OEMs for taking their meetings, listening and acting.”

That’s a pragmatic shift. In prior years, the study often captured supplier frustration with OEMs that didn’t listen. In 2026, suppliers seem to be saying: “You can’t control the tariffs. But you can control whether you call me back.”

A Few Honest Questions About the Data

The WRI is the best longitudinal dataset we have on automaker-supplier relations. That said, reading the 2026 results with an operator’s eye raises a few questions worth sitting with.

Is universal improvement a signal or noise?

When all six OEMs move in the same direction, it’s worth asking whether the shift is driven by OEM behavior or by the environment. The “permacrisis” framing cuts both ways. If suppliers are grading on a curve -- giving credit for effort during hard times -- then the scores may partly reflect lowered expectations rather than genuinely improved behavior. A buyer who answers the phone during a war isn’t necessarily a better buyer than one who answered the phone during peacetime. They’re just more appreciated.

The 2027 study will be the real test. If the macro environment stabilizes and scores hold, the improvement is structural. If scores dip when the pressure eases, 2026 was sentiment, not systems.

The Toyota gap is structural, not just cultural

Toyota’s 246-point lead over Stellantis isn’t just about attitude. It’s about architecture. Their 10-K filings reveal the strategic DNA behind these differences. Toyota’s keiretsu model -- long-term equity relationships with key suppliers, shared production knowledge through jishuken (inter-company kaizen), and a purchasing philosophy built around “co-prosperity” -- is a fundamentally different operating system than the adversarial bid-and-beat approach that defined Detroit purchasing for decades. Toyota’s purchasing staff handbook instructs buyers to “make efforts to improve performance at supplier plants.” That’s not a KPI. That’s a cultural directive embedded in onboarding materials.

The Detroit Three can’t replicate the keiretsu overnight. GM, Ford, and Stellantis are publicly traded companies under quarterly earnings pressure, managing pension obligations, union relationships, and legacy cost structures that Toyota doesn’t carry in North America. Improving WRI scores within those constraints is genuinely hard. The study deserves credit for tracking the effort. But the structural gap between Toyota’s supplier model and Detroit’s supplier model is wider than any annual score swing can close.

Stellantis context matters

Stellantis’s 22-point jump looks encouraging until you remember where it came from. Carlos Tavares resigned as CEO in December 2024 after a period of aggressive cost-cutting that cratered supplier relationships. Stellantis’s Q3 2024 shipments declined 20% year-over-year. The supply chain organization was reorganized under Arnaud Deboeuf, with Maxime Picat refocusing on supplier partner performance. A 22-point gain from a score of 141 may reflect relief at the leadership change as much as genuine operational improvement. Stellantis at 163 is still in the study’s lowest tier -- well below the industry average and less than half of Toyota’s score.

What the study doesn’t measure

The WRI tracks supplier perception of OEM behavior. It does not directly measure what suppliers do in response -- whether they actually allocate better pricing, technology, or capacity to higher-scoring OEMs. The correlation between WRI scores and OEM profitability is cited often, but correlation across a six-company sample over time is a weaker statistical claim than it sounds. Toyota is profitable and has high WRI scores, but Toyota is also profitable for many reasons that have nothing to do with supplier sentiment (production system efficiency, product strategy, balance sheet strength).

The study also surveys Tier 1 executives -- the people who sit across the table from OEM buyers. It doesn’t capture the Tier 2 and Tier 3 perspective, where much of the actual supply chain friction lives. A Tier 1 supplier may rate an OEM highly while simultaneously passing the same OEM’s cost pressures down to smaller suppliers who have no voice in the study.

None of this diminishes the WRI’s value. It’s the best instrument available for tracking this dimension of the industry. But reading the scores as an objective measure of “how good this OEM is to work with” overstates what the data can tell us. They’re a perception index. Perception matters enormously -- but it’s not the whole picture.

What This Means for Procurement Leaders

The WRI study confirms something that 26 years of data have consistently shown: how you treat suppliers is a competitive variable, not just a cultural nicety.

OEMs that rank higher on the WRI consistently report better outcomes on five dimensions that matter to the business:

Pricing: Suppliers give preferred pricing to OEMs they trust, because they know the relationship will be fair over time.

Technology access: New innovations go first to the OEMs that suppliers want to work with.

Capacity allocation: When supply is tight -- as it has been for much of the past three years -- preferred customers get priority.

Quality investment: Suppliers invest more in quality systems and continuous improvement for customers who reciprocate.

Problem-solving speed: When something goes wrong (a quality escape, a delivery delay, a spec change), the speed of resolution depends on the relationship underneath it.

For procurement leaders outside of automotive, the framework translates directly. The Six Cs -- commercial fairness, consistency, clear expectations, communication, continuity, and collaboration -- aren’t automotive-specific. They’re the behaviors that distinguish strategic partnerships from transactional vendor management in any industry.

At LightSource, the supplier side of the platform is built around these same principles -- giving suppliers visibility into timelines, structured feedback on wins and losses, and a communication channel that doesn’t disappear when a buyer changes roles. The WRI data is a 26-year empirical case that this approach works.

The 2026 WRI results are encouraging, but one year of universal improvement doesn’t erase decades of accumulated supplier experience. The real test is whether the behaviors that drove this year’s gains persist when economic conditions change -- when margins tighten, when new leadership arrives, when the pressure to extract cost from suppliers becomes acute again.

Dr. Johnson asks the right question: “Will subsequent WRI studies show the industry is adapting to its permacrisis existence by embracing an era of mutualism?” The 2027 study will be the first real check on whether 2026 was a turning point or a one-year anomaly.

Sources

Plante Moran -- 2026 Working Relations Index Study -- Original study results, methodology, and Six Cs framework

GlobeNewsWire -- All OEMs Raise Their Scores: First Time in WRI History -- Press release with full score data

Automotive Logistics -- North American OEMs Improve Supplier Relations in 2026 -- Industry analysis of WRI results

Assembly Magazine -- Automaker-Supplier Relations Improve Despite Tariff, EV Pressures -- Coverage of key improvement areas

WardsAuto -- Toyota, Honda, GM Improve Supplier Relationships -- Analysis of Top 50 supplier segment

Frequently Asked Questions

What is the Working Relations Index?

The Working Relations Index (WRI) is an annual study conducted by Plante Moran that measures Tier 1 automotive suppliers’ perceptions of their working relationships with the six major North American OEMs: Toyota, Honda, GM, Nissan, Ford, and Stellantis. Founded in 2001, it’s the longest-running empirical benchmark of automaker-supplier relations, with 26 years of data showing a consistent correlation between higher WRI scores and better commercial outcomes for OEMs.

Why did all six OEMs improve in 2026?

The study identifies several converging factors: OEMs leaned into controllable relationship behaviors (communication, accessibility, problem-solving) when they couldn’t control external pressures like tariffs and EV cost recovery. Return-to-office mandates increased buyer availability. And a growing “permacrisis” awareness drove both OEMs and suppliers toward more collaborative approaches. The 10,000+ supplier comments -- triple prior years -- suggest an industry-wide shift toward mutual recognition that cooperation beats adversarial negotiation in volatile conditions.

What are the Six Cs in the WRI framework?

The Six Cs are controllable behaviors that Dr. Angela Johnson identified as distinguishing OEMs with strong supplier relations: commercial fairness (equitable risk sharing), consistency (reliable scheduling), clear expectations (unambiguous requirements), communication (proactive and simple), continuity (strategy that survives leadership changes), and collaboration (genuine joint problem-solving). They form a progression from transactional to relational.

Why do Top 50 suppliers rate the Detroit Three lower than Japanese OEMs?

Top 50 North American suppliers carry deeper institutional memory from decades of OEM interactions. Toyota, Honda, and Nissan benefit from historically collaborative supplier cultures, while GM, Ford, and Stellantis are still working to overcome what Dr. Johnson calls “the cultural inertia of historically adversarial purchasing organizations.” Top 50 suppliers also face larger dollar impacts from tariffs and EV write-offs, making their assessments of commercial fairness more pointed.

How does the WRI correlate with business outcomes?

Twenty-six years of WRI data demonstrate that OEMs with higher supplier relations scores consistently receive better pricing, earlier access to new technology, preferential capacity allocation during shortages, greater supplier investment in quality systems, and faster problem resolution. The relationship is bidirectional -- OEMs that invest in supplier relations earn returns that contribute to operating profits and competitive strength.

How can non-automotive procurement leaders apply the WRI findings?

The Six Cs framework translates directly to any industry. Commercial fairness, consistency, clear expectations, communication, continuity, and collaboration are the behaviors that distinguish strategic supplier partnerships from transactional vendor management regardless of sector. Companies that measure and improve these dimensions with their supply base consistently see better cost outcomes, faster innovation cycles, and more resilient supply chains.

Plante Moran released its 2026 Working Relations Index (WRI) study on May 18, and the headline result is one that hasn’t happened in the study’s 26-year history: all six major North American OEMs improved their supplier relations scores. Toyota, Honda, GM, Nissan, Ford, and Stellantis all moved up.

That’s notable not because of the direction -- improvement is always the goal -- but because of the context in which it happened. The survey was conducted from March through mid-April 2026, a period in which suppliers were navigating tariff uncertainty, EV-related cost write-offs, and the early economic fallout from the Iran war. This wasn’t a year of calm waters and easy wins. Suppliers gave higher marks despite operating under more pressure than usual.

The WRI study, founded in 2001 by Dr. John Henke and acquired by Plante Moran in 2019, surveys Tier 1 supplier executives about their working relationships with the six OEMs. This year’s sample was the largest ever: 750 responses (up from 665 in 2025), representing 78 of the top 100 North American automotive suppliers and covering 2,348 buying situations. Suppliers also submitted more than 10,000 written comments -- more than three times the roughly 2,800 received in prior years.

The study is one of the few empirical benchmarks that tracks how automakers actually treat the companies that build their vehicles. And 26 years of data show a consistent correlation: OEMs with stronger supplier relations earn better commercial outcomes -- more favorable pricing, earlier access to new technology, and preferential capacity allocation when supply is tight.

Here’s what the 2026 numbers show.

The Scores

Rank | OEM | 2026 Score | YoY Change | Historical Context |

|---|---|---|---|---|

1 | Toyota | 409 | +23 | Highest since 2007; second-best score ever (415 in 2005 and 2007) |

2 | Honda | 360 | +13 | Highest since 2007; entered the study’s “good to very good” range |

3 | GM | 318 | +8 | All-time high WRI score |

4 | Nissan | 255 | +6 | Matches 2024 level; best since 2014 |

5 | Ford | 223 | +32 | Second-largest single-year jump in company history (largest was 41 points in 2008-2009) |

6 | Stellantis | 163 | +22 | Best score since 2021 |

The gap between first and last is still 246 points. Toyota’s score is more than double Stellantis’s. But the direction matters: every OEM moved in the same direction for the first time since the study began.

Ford’s 32-point jump stands out. That’s not a statistical wobble -- it’s the kind of move that reflects organizational change. Honda’s return to the “good to very good” category and GM’s all-time high are equally significant, even if the point changes are smaller.

What Drove the Improvement

Dr. Angela Johnson, the Plante Moran principal who leads the study, identified four areas where suppliers reported better perceptions across the board.

Long-Term Profit Ability

Toyota maintains the frontrunner position on suppliers’ confidence in long-term profitability. But Ford, Stellantis, and Nissan showed strong gains here -- a signal that suppliers are becoming more optimistic about these OEMs’ strategic direction, even if short-term margins remain pressured.

Commercial Fairness and Cost Management

This is the area most directly shaped by macro conditions. Tariffs and EV cost recovery were the two biggest factors influencing suppliers’ perceptions of fairness. Purchasing teams that lacked full control over how much their OEM absorbed those costs compensated by leaning into relationship-building behaviors within their control.

Ford and Stellantis posted the largest gains in fairness perceptions. Toyota and Honda led in cost reduction support. GM made the biggest advances in sunk cost and EV recovery coverage -- though it faced pushback from suppliers on supply chain resiliency initiatives.

Buyer Performance

Accessibility, engagement, and responsiveness improved across all six OEMs. The study notes that return-to-office mandates contributed to this: more buyers physically in the office meant more availability for supplier meetings and issue resolution. Issue resolution ability -- the capacity to actually fix problems, not just acknowledge them -- showed the strongest gains.

This is one of those areas where the sourcing bottleneck matters. When buyers are overwhelmed with manual processes, responsiveness suffers. When the operational load is lighter, they can invest more in supplier relationships.

Communication and Trust-Building

Toyota and Honda continue to lead in trust metrics. Ford and Stellantis made the biggest jumps. Ford’s Liz Door was noted for the largest trust improvement among purchasing chiefs -- a result tied to increased transparency and proactive communication with the supply base.

Dr. Johnson observed: “In 2026, all six automakers improved trust scores through enhanced communication, accessibility and their ability to solve problems.”

The Six Cs: What Separates Top from Bottom

The study introduced a framework Dr. Johnson calls the “Six Cs” -- controllable behaviors that distinguish OEMs with strong supplier relations from those still building trust. She describes them as a pyramid, progressing from transactional to relational:

Commercial fairness -- equitable risk and cost sharing. The foundation.

Consistency -- longer-term scheduling and production plans that suppliers can actually build capacity against.

Clear expectations -- unambiguous requirements. Not shifting goalposts.

Communication -- proactive, clear, simple messaging. Not email storms with no context.

Continuity -- long-term OEM-supplier strategy that survives leadership changes.

Collaboration -- genuine joint problem-solving. The top of the pyramid.

The insight here is that the behaviors at the bottom of the pyramid (commercial fairness, consistency) are necessary but not sufficient. OEMs that excel on those basics but fail on communication and collaboration still don’t earn top marks. The suppliers who rated OEMs highest credited them for demonstrating all six.

This framework maps directly to what we see in supplier performance management more broadly: the relationship between a buyer and supplier isn’t just a set of commercial terms. It’s an operating system that either enables or constrains both parties.

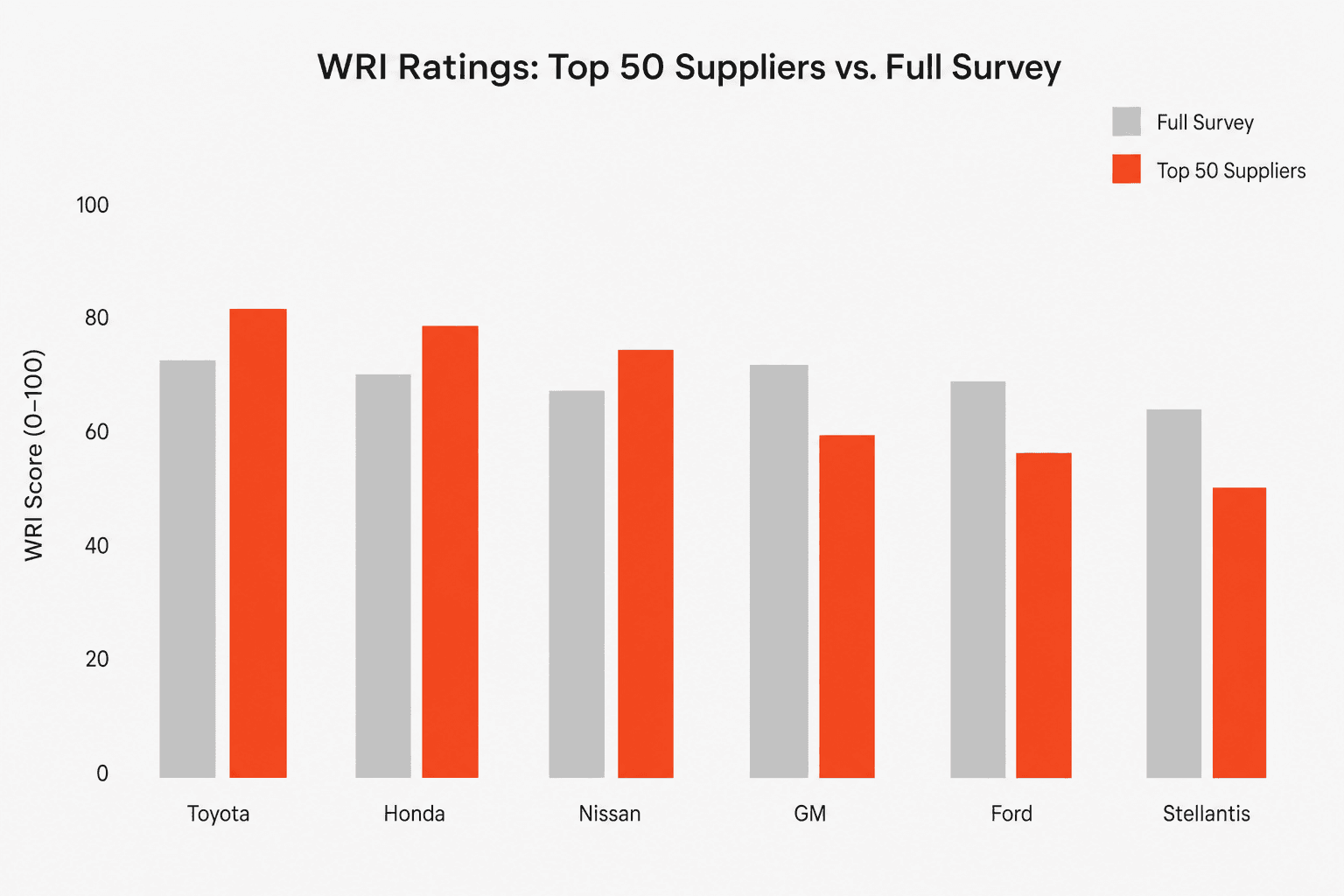

The Top 50 Supplier Perspective

The study breaks out ratings from the Top 50 North American suppliers separately -- and the results tell a different story from the overall averages.

Top 50 suppliers rated Nissan, Honda, and Toyota above their overall averages. They rated GM, Stellantis, and Ford below their respective averages. The disparity was most noticeable in measures of trust, communication, and profit opportunity.

Why? Two reasons.

First, these are the suppliers with the deepest relationships and the most at stake. They’ve been through multiple OEM leadership cycles, restructuring programs, and strategic pivots. Their ratings carry more institutional memory -- both positive and negative.

Second, the tariff and EV cost recovery impacts hit Top 50 suppliers harder. Larger suppliers carry more exposure to commodity price swings, tooling amortization on canceled EV programs, and the logistics disruptions discussed in the Hormuz crisis. Their assessments of commercial fairness are grounded in larger dollar figures and higher-stakes negotiations.

Dr. Johnson put it directly: “Organizational memory is very long. The Detroit Three are still fighting to overcome the cultural inertia of historically adversarial purchasing organizations.”

That doesn’t discredit the progress. All six OEMs improved even in the Top 50 segment. But it does explain why Toyota, Honda, and Nissan -- OEMs with historically collaborative supplier cultures -- continue to outperform on relationship metrics even when their commercial terms aren’t always the most generous. For a deeper analysis of what this perception gap reveals about institutional memory and why mid-tier supplier responses may be the more useful leading indicator, see What Suppliers 51-100 Tell You That the Top 50 Won’t.

The Permacrisis Effect

One of the study’s most interesting findings isn’t in the scores. It’s in the comments.

Suppliers submitted more than 10,000 written comments this year -- more than triple the roughly 2,800 received in prior years. Dr. Johnson noted: “We saw an emerging, collective recognition that working together is the best way to face permacrisis challenges, innovate, and grow.”

The word “permacrisis” keeps showing up in procurement circles, and the WRI data suggests it’s changing supplier behavior. When the external environment is volatile -- tariffs shifting, raw materials spiking, geopolitical disruptions hitting shipping lanes -- suppliers appear to credit OEMs more for the effort of trying, even when outcomes aren’t perfect.

As Dr. Johnson observed: “Suppliers appeared to acknowledge efforts OEMs made over the past year to control what they could and to help suppliers navigate industry uncertainty. Even if suppliers didn’t experience their ideal outcome, they credited the OEMs for taking their meetings, listening and acting.”

That’s a pragmatic shift. In prior years, the study often captured supplier frustration with OEMs that didn’t listen. In 2026, suppliers seem to be saying: “You can’t control the tariffs. But you can control whether you call me back.”

A Few Honest Questions About the Data

The WRI is the best longitudinal dataset we have on automaker-supplier relations. That said, reading the 2026 results with an operator’s eye raises a few questions worth sitting with.

Is universal improvement a signal or noise?

When all six OEMs move in the same direction, it’s worth asking whether the shift is driven by OEM behavior or by the environment. The “permacrisis” framing cuts both ways. If suppliers are grading on a curve -- giving credit for effort during hard times -- then the scores may partly reflect lowered expectations rather than genuinely improved behavior. A buyer who answers the phone during a war isn’t necessarily a better buyer than one who answered the phone during peacetime. They’re just more appreciated.

The 2027 study will be the real test. If the macro environment stabilizes and scores hold, the improvement is structural. If scores dip when the pressure eases, 2026 was sentiment, not systems.

The Toyota gap is structural, not just cultural

Toyota’s 246-point lead over Stellantis isn’t just about attitude. It’s about architecture. Their 10-K filings reveal the strategic DNA behind these differences. Toyota’s keiretsu model -- long-term equity relationships with key suppliers, shared production knowledge through jishuken (inter-company kaizen), and a purchasing philosophy built around “co-prosperity” -- is a fundamentally different operating system than the adversarial bid-and-beat approach that defined Detroit purchasing for decades. Toyota’s purchasing staff handbook instructs buyers to “make efforts to improve performance at supplier plants.” That’s not a KPI. That’s a cultural directive embedded in onboarding materials.

The Detroit Three can’t replicate the keiretsu overnight. GM, Ford, and Stellantis are publicly traded companies under quarterly earnings pressure, managing pension obligations, union relationships, and legacy cost structures that Toyota doesn’t carry in North America. Improving WRI scores within those constraints is genuinely hard. The study deserves credit for tracking the effort. But the structural gap between Toyota’s supplier model and Detroit’s supplier model is wider than any annual score swing can close.

Stellantis context matters

Stellantis’s 22-point jump looks encouraging until you remember where it came from. Carlos Tavares resigned as CEO in December 2024 after a period of aggressive cost-cutting that cratered supplier relationships. Stellantis’s Q3 2024 shipments declined 20% year-over-year. The supply chain organization was reorganized under Arnaud Deboeuf, with Maxime Picat refocusing on supplier partner performance. A 22-point gain from a score of 141 may reflect relief at the leadership change as much as genuine operational improvement. Stellantis at 163 is still in the study’s lowest tier -- well below the industry average and less than half of Toyota’s score.

What the study doesn’t measure

The WRI tracks supplier perception of OEM behavior. It does not directly measure what suppliers do in response -- whether they actually allocate better pricing, technology, or capacity to higher-scoring OEMs. The correlation between WRI scores and OEM profitability is cited often, but correlation across a six-company sample over time is a weaker statistical claim than it sounds. Toyota is profitable and has high WRI scores, but Toyota is also profitable for many reasons that have nothing to do with supplier sentiment (production system efficiency, product strategy, balance sheet strength).

The study also surveys Tier 1 executives -- the people who sit across the table from OEM buyers. It doesn’t capture the Tier 2 and Tier 3 perspective, where much of the actual supply chain friction lives. A Tier 1 supplier may rate an OEM highly while simultaneously passing the same OEM’s cost pressures down to smaller suppliers who have no voice in the study.

None of this diminishes the WRI’s value. It’s the best instrument available for tracking this dimension of the industry. But reading the scores as an objective measure of “how good this OEM is to work with” overstates what the data can tell us. They’re a perception index. Perception matters enormously -- but it’s not the whole picture.

What This Means for Procurement Leaders

The WRI study confirms something that 26 years of data have consistently shown: how you treat suppliers is a competitive variable, not just a cultural nicety.

OEMs that rank higher on the WRI consistently report better outcomes on five dimensions that matter to the business:

Pricing: Suppliers give preferred pricing to OEMs they trust, because they know the relationship will be fair over time.

Technology access: New innovations go first to the OEMs that suppliers want to work with.

Capacity allocation: When supply is tight -- as it has been for much of the past three years -- preferred customers get priority.

Quality investment: Suppliers invest more in quality systems and continuous improvement for customers who reciprocate.

Problem-solving speed: When something goes wrong (a quality escape, a delivery delay, a spec change), the speed of resolution depends on the relationship underneath it.

For procurement leaders outside of automotive, the framework translates directly. The Six Cs -- commercial fairness, consistency, clear expectations, communication, continuity, and collaboration -- aren’t automotive-specific. They’re the behaviors that distinguish strategic partnerships from transactional vendor management in any industry.

At LightSource, the supplier side of the platform is built around these same principles -- giving suppliers visibility into timelines, structured feedback on wins and losses, and a communication channel that doesn’t disappear when a buyer changes roles. The WRI data is a 26-year empirical case that this approach works.

The 2026 WRI results are encouraging, but one year of universal improvement doesn’t erase decades of accumulated supplier experience. The real test is whether the behaviors that drove this year’s gains persist when economic conditions change -- when margins tighten, when new leadership arrives, when the pressure to extract cost from suppliers becomes acute again.

Dr. Johnson asks the right question: “Will subsequent WRI studies show the industry is adapting to its permacrisis existence by embracing an era of mutualism?” The 2027 study will be the first real check on whether 2026 was a turning point or a one-year anomaly.

Sources

Plante Moran -- 2026 Working Relations Index Study -- Original study results, methodology, and Six Cs framework

GlobeNewsWire -- All OEMs Raise Their Scores: First Time in WRI History -- Press release with full score data

Automotive Logistics -- North American OEMs Improve Supplier Relations in 2026 -- Industry analysis of WRI results

Assembly Magazine -- Automaker-Supplier Relations Improve Despite Tariff, EV Pressures -- Coverage of key improvement areas

WardsAuto -- Toyota, Honda, GM Improve Supplier Relationships -- Analysis of Top 50 supplier segment

Frequently Asked Questions

What is the Working Relations Index?

The Working Relations Index (WRI) is an annual study conducted by Plante Moran that measures Tier 1 automotive suppliers’ perceptions of their working relationships with the six major North American OEMs: Toyota, Honda, GM, Nissan, Ford, and Stellantis. Founded in 2001, it’s the longest-running empirical benchmark of automaker-supplier relations, with 26 years of data showing a consistent correlation between higher WRI scores and better commercial outcomes for OEMs.

Why did all six OEMs improve in 2026?

The study identifies several converging factors: OEMs leaned into controllable relationship behaviors (communication, accessibility, problem-solving) when they couldn’t control external pressures like tariffs and EV cost recovery. Return-to-office mandates increased buyer availability. And a growing “permacrisis” awareness drove both OEMs and suppliers toward more collaborative approaches. The 10,000+ supplier comments -- triple prior years -- suggest an industry-wide shift toward mutual recognition that cooperation beats adversarial negotiation in volatile conditions.

What are the Six Cs in the WRI framework?

The Six Cs are controllable behaviors that Dr. Angela Johnson identified as distinguishing OEMs with strong supplier relations: commercial fairness (equitable risk sharing), consistency (reliable scheduling), clear expectations (unambiguous requirements), communication (proactive and simple), continuity (strategy that survives leadership changes), and collaboration (genuine joint problem-solving). They form a progression from transactional to relational.

Why do Top 50 suppliers rate the Detroit Three lower than Japanese OEMs?

Top 50 North American suppliers carry deeper institutional memory from decades of OEM interactions. Toyota, Honda, and Nissan benefit from historically collaborative supplier cultures, while GM, Ford, and Stellantis are still working to overcome what Dr. Johnson calls “the cultural inertia of historically adversarial purchasing organizations.” Top 50 suppliers also face larger dollar impacts from tariffs and EV write-offs, making their assessments of commercial fairness more pointed.

How does the WRI correlate with business outcomes?

Twenty-six years of WRI data demonstrate that OEMs with higher supplier relations scores consistently receive better pricing, earlier access to new technology, preferential capacity allocation during shortages, greater supplier investment in quality systems, and faster problem resolution. The relationship is bidirectional -- OEMs that invest in supplier relations earn returns that contribute to operating profits and competitive strength.

How can non-automotive procurement leaders apply the WRI findings?

The Six Cs framework translates directly to any industry. Commercial fairness, consistency, clear expectations, communication, continuity, and collaboration are the behaviors that distinguish strategic supplier partnerships from transactional vendor management regardless of sector. Companies that measure and improve these dimensions with their supply base consistently see better cost outcomes, faster innovation cycles, and more resilient supply chains.

Plante Moran released its 2026 Working Relations Index (WRI) study on May 18, and the headline result is one that hasn’t happened in the study’s 26-year history: all six major North American OEMs improved their supplier relations scores. Toyota, Honda, GM, Nissan, Ford, and Stellantis all moved up.

That’s notable not because of the direction -- improvement is always the goal -- but because of the context in which it happened. The survey was conducted from March through mid-April 2026, a period in which suppliers were navigating tariff uncertainty, EV-related cost write-offs, and the early economic fallout from the Iran war. This wasn’t a year of calm waters and easy wins. Suppliers gave higher marks despite operating under more pressure than usual.

The WRI study, founded in 2001 by Dr. John Henke and acquired by Plante Moran in 2019, surveys Tier 1 supplier executives about their working relationships with the six OEMs. This year’s sample was the largest ever: 750 responses (up from 665 in 2025), representing 78 of the top 100 North American automotive suppliers and covering 2,348 buying situations. Suppliers also submitted more than 10,000 written comments -- more than three times the roughly 2,800 received in prior years.

The study is one of the few empirical benchmarks that tracks how automakers actually treat the companies that build their vehicles. And 26 years of data show a consistent correlation: OEMs with stronger supplier relations earn better commercial outcomes -- more favorable pricing, earlier access to new technology, and preferential capacity allocation when supply is tight.

Here’s what the 2026 numbers show.

The Scores

Rank | OEM | 2026 Score | YoY Change | Historical Context |

|---|---|---|---|---|

1 | Toyota | 409 | +23 | Highest since 2007; second-best score ever (415 in 2005 and 2007) |

2 | Honda | 360 | +13 | Highest since 2007; entered the study’s “good to very good” range |

3 | GM | 318 | +8 | All-time high WRI score |

4 | Nissan | 255 | +6 | Matches 2024 level; best since 2014 |

5 | Ford | 223 | +32 | Second-largest single-year jump in company history (largest was 41 points in 2008-2009) |

6 | Stellantis | 163 | +22 | Best score since 2021 |

The gap between first and last is still 246 points. Toyota’s score is more than double Stellantis’s. But the direction matters: every OEM moved in the same direction for the first time since the study began.

Ford’s 32-point jump stands out. That’s not a statistical wobble -- it’s the kind of move that reflects organizational change. Honda’s return to the “good to very good” category and GM’s all-time high are equally significant, even if the point changes are smaller.

What Drove the Improvement

Dr. Angela Johnson, the Plante Moran principal who leads the study, identified four areas where suppliers reported better perceptions across the board.

Long-Term Profit Ability

Toyota maintains the frontrunner position on suppliers’ confidence in long-term profitability. But Ford, Stellantis, and Nissan showed strong gains here -- a signal that suppliers are becoming more optimistic about these OEMs’ strategic direction, even if short-term margins remain pressured.

Commercial Fairness and Cost Management

This is the area most directly shaped by macro conditions. Tariffs and EV cost recovery were the two biggest factors influencing suppliers’ perceptions of fairness. Purchasing teams that lacked full control over how much their OEM absorbed those costs compensated by leaning into relationship-building behaviors within their control.

Ford and Stellantis posted the largest gains in fairness perceptions. Toyota and Honda led in cost reduction support. GM made the biggest advances in sunk cost and EV recovery coverage -- though it faced pushback from suppliers on supply chain resiliency initiatives.

Buyer Performance

Accessibility, engagement, and responsiveness improved across all six OEMs. The study notes that return-to-office mandates contributed to this: more buyers physically in the office meant more availability for supplier meetings and issue resolution. Issue resolution ability -- the capacity to actually fix problems, not just acknowledge them -- showed the strongest gains.

This is one of those areas where the sourcing bottleneck matters. When buyers are overwhelmed with manual processes, responsiveness suffers. When the operational load is lighter, they can invest more in supplier relationships.

Communication and Trust-Building

Toyota and Honda continue to lead in trust metrics. Ford and Stellantis made the biggest jumps. Ford’s Liz Door was noted for the largest trust improvement among purchasing chiefs -- a result tied to increased transparency and proactive communication with the supply base.

Dr. Johnson observed: “In 2026, all six automakers improved trust scores through enhanced communication, accessibility and their ability to solve problems.”

The Six Cs: What Separates Top from Bottom

The study introduced a framework Dr. Johnson calls the “Six Cs” -- controllable behaviors that distinguish OEMs with strong supplier relations from those still building trust. She describes them as a pyramid, progressing from transactional to relational:

Commercial fairness -- equitable risk and cost sharing. The foundation.

Consistency -- longer-term scheduling and production plans that suppliers can actually build capacity against.

Clear expectations -- unambiguous requirements. Not shifting goalposts.

Communication -- proactive, clear, simple messaging. Not email storms with no context.

Continuity -- long-term OEM-supplier strategy that survives leadership changes.

Collaboration -- genuine joint problem-solving. The top of the pyramid.

The insight here is that the behaviors at the bottom of the pyramid (commercial fairness, consistency) are necessary but not sufficient. OEMs that excel on those basics but fail on communication and collaboration still don’t earn top marks. The suppliers who rated OEMs highest credited them for demonstrating all six.

This framework maps directly to what we see in supplier performance management more broadly: the relationship between a buyer and supplier isn’t just a set of commercial terms. It’s an operating system that either enables or constrains both parties.

The Top 50 Supplier Perspective

The study breaks out ratings from the Top 50 North American suppliers separately -- and the results tell a different story from the overall averages.

Top 50 suppliers rated Nissan, Honda, and Toyota above their overall averages. They rated GM, Stellantis, and Ford below their respective averages. The disparity was most noticeable in measures of trust, communication, and profit opportunity.

Why? Two reasons.

First, these are the suppliers with the deepest relationships and the most at stake. They’ve been through multiple OEM leadership cycles, restructuring programs, and strategic pivots. Their ratings carry more institutional memory -- both positive and negative.

Second, the tariff and EV cost recovery impacts hit Top 50 suppliers harder. Larger suppliers carry more exposure to commodity price swings, tooling amortization on canceled EV programs, and the logistics disruptions discussed in the Hormuz crisis. Their assessments of commercial fairness are grounded in larger dollar figures and higher-stakes negotiations.

Dr. Johnson put it directly: “Organizational memory is very long. The Detroit Three are still fighting to overcome the cultural inertia of historically adversarial purchasing organizations.”

That doesn’t discredit the progress. All six OEMs improved even in the Top 50 segment. But it does explain why Toyota, Honda, and Nissan -- OEMs with historically collaborative supplier cultures -- continue to outperform on relationship metrics even when their commercial terms aren’t always the most generous. For a deeper analysis of what this perception gap reveals about institutional memory and why mid-tier supplier responses may be the more useful leading indicator, see What Suppliers 51-100 Tell You That the Top 50 Won’t.

The Permacrisis Effect

One of the study’s most interesting findings isn’t in the scores. It’s in the comments.

Suppliers submitted more than 10,000 written comments this year -- more than triple the roughly 2,800 received in prior years. Dr. Johnson noted: “We saw an emerging, collective recognition that working together is the best way to face permacrisis challenges, innovate, and grow.”

The word “permacrisis” keeps showing up in procurement circles, and the WRI data suggests it’s changing supplier behavior. When the external environment is volatile -- tariffs shifting, raw materials spiking, geopolitical disruptions hitting shipping lanes -- suppliers appear to credit OEMs more for the effort of trying, even when outcomes aren’t perfect.

As Dr. Johnson observed: “Suppliers appeared to acknowledge efforts OEMs made over the past year to control what they could and to help suppliers navigate industry uncertainty. Even if suppliers didn’t experience their ideal outcome, they credited the OEMs for taking their meetings, listening and acting.”

That’s a pragmatic shift. In prior years, the study often captured supplier frustration with OEMs that didn’t listen. In 2026, suppliers seem to be saying: “You can’t control the tariffs. But you can control whether you call me back.”

A Few Honest Questions About the Data

The WRI is the best longitudinal dataset we have on automaker-supplier relations. That said, reading the 2026 results with an operator’s eye raises a few questions worth sitting with.

Is universal improvement a signal or noise?

When all six OEMs move in the same direction, it’s worth asking whether the shift is driven by OEM behavior or by the environment. The “permacrisis” framing cuts both ways. If suppliers are grading on a curve -- giving credit for effort during hard times -- then the scores may partly reflect lowered expectations rather than genuinely improved behavior. A buyer who answers the phone during a war isn’t necessarily a better buyer than one who answered the phone during peacetime. They’re just more appreciated.

The 2027 study will be the real test. If the macro environment stabilizes and scores hold, the improvement is structural. If scores dip when the pressure eases, 2026 was sentiment, not systems.

The Toyota gap is structural, not just cultural

Toyota’s 246-point lead over Stellantis isn’t just about attitude. It’s about architecture. Their 10-K filings reveal the strategic DNA behind these differences. Toyota’s keiretsu model -- long-term equity relationships with key suppliers, shared production knowledge through jishuken (inter-company kaizen), and a purchasing philosophy built around “co-prosperity” -- is a fundamentally different operating system than the adversarial bid-and-beat approach that defined Detroit purchasing for decades. Toyota’s purchasing staff handbook instructs buyers to “make efforts to improve performance at supplier plants.” That’s not a KPI. That’s a cultural directive embedded in onboarding materials.

The Detroit Three can’t replicate the keiretsu overnight. GM, Ford, and Stellantis are publicly traded companies under quarterly earnings pressure, managing pension obligations, union relationships, and legacy cost structures that Toyota doesn’t carry in North America. Improving WRI scores within those constraints is genuinely hard. The study deserves credit for tracking the effort. But the structural gap between Toyota’s supplier model and Detroit’s supplier model is wider than any annual score swing can close.

Stellantis context matters

Stellantis’s 22-point jump looks encouraging until you remember where it came from. Carlos Tavares resigned as CEO in December 2024 after a period of aggressive cost-cutting that cratered supplier relationships. Stellantis’s Q3 2024 shipments declined 20% year-over-year. The supply chain organization was reorganized under Arnaud Deboeuf, with Maxime Picat refocusing on supplier partner performance. A 22-point gain from a score of 141 may reflect relief at the leadership change as much as genuine operational improvement. Stellantis at 163 is still in the study’s lowest tier -- well below the industry average and less than half of Toyota’s score.

What the study doesn’t measure

The WRI tracks supplier perception of OEM behavior. It does not directly measure what suppliers do in response -- whether they actually allocate better pricing, technology, or capacity to higher-scoring OEMs. The correlation between WRI scores and OEM profitability is cited often, but correlation across a six-company sample over time is a weaker statistical claim than it sounds. Toyota is profitable and has high WRI scores, but Toyota is also profitable for many reasons that have nothing to do with supplier sentiment (production system efficiency, product strategy, balance sheet strength).

The study also surveys Tier 1 executives -- the people who sit across the table from OEM buyers. It doesn’t capture the Tier 2 and Tier 3 perspective, where much of the actual supply chain friction lives. A Tier 1 supplier may rate an OEM highly while simultaneously passing the same OEM’s cost pressures down to smaller suppliers who have no voice in the study.

None of this diminishes the WRI’s value. It’s the best instrument available for tracking this dimension of the industry. But reading the scores as an objective measure of “how good this OEM is to work with” overstates what the data can tell us. They’re a perception index. Perception matters enormously -- but it’s not the whole picture.

What This Means for Procurement Leaders

The WRI study confirms something that 26 years of data have consistently shown: how you treat suppliers is a competitive variable, not just a cultural nicety.

OEMs that rank higher on the WRI consistently report better outcomes on five dimensions that matter to the business:

Pricing: Suppliers give preferred pricing to OEMs they trust, because they know the relationship will be fair over time.

Technology access: New innovations go first to the OEMs that suppliers want to work with.

Capacity allocation: When supply is tight -- as it has been for much of the past three years -- preferred customers get priority.

Quality investment: Suppliers invest more in quality systems and continuous improvement for customers who reciprocate.

Problem-solving speed: When something goes wrong (a quality escape, a delivery delay, a spec change), the speed of resolution depends on the relationship underneath it.

For procurement leaders outside of automotive, the framework translates directly. The Six Cs -- commercial fairness, consistency, clear expectations, communication, continuity, and collaboration -- aren’t automotive-specific. They’re the behaviors that distinguish strategic partnerships from transactional vendor management in any industry.

At LightSource, the supplier side of the platform is built around these same principles -- giving suppliers visibility into timelines, structured feedback on wins and losses, and a communication channel that doesn’t disappear when a buyer changes roles. The WRI data is a 26-year empirical case that this approach works.

The 2026 WRI results are encouraging, but one year of universal improvement doesn’t erase decades of accumulated supplier experience. The real test is whether the behaviors that drove this year’s gains persist when economic conditions change -- when margins tighten, when new leadership arrives, when the pressure to extract cost from suppliers becomes acute again.

Dr. Johnson asks the right question: “Will subsequent WRI studies show the industry is adapting to its permacrisis existence by embracing an era of mutualism?” The 2027 study will be the first real check on whether 2026 was a turning point or a one-year anomaly.

Sources

Plante Moran -- 2026 Working Relations Index Study -- Original study results, methodology, and Six Cs framework

GlobeNewsWire -- All OEMs Raise Their Scores: First Time in WRI History -- Press release with full score data

Automotive Logistics -- North American OEMs Improve Supplier Relations in 2026 -- Industry analysis of WRI results

Assembly Magazine -- Automaker-Supplier Relations Improve Despite Tariff, EV Pressures -- Coverage of key improvement areas

WardsAuto -- Toyota, Honda, GM Improve Supplier Relationships -- Analysis of Top 50 supplier segment

Frequently Asked Questions

What is the Working Relations Index?

The Working Relations Index (WRI) is an annual study conducted by Plante Moran that measures Tier 1 automotive suppliers’ perceptions of their working relationships with the six major North American OEMs: Toyota, Honda, GM, Nissan, Ford, and Stellantis. Founded in 2001, it’s the longest-running empirical benchmark of automaker-supplier relations, with 26 years of data showing a consistent correlation between higher WRI scores and better commercial outcomes for OEMs.

Why did all six OEMs improve in 2026?

The study identifies several converging factors: OEMs leaned into controllable relationship behaviors (communication, accessibility, problem-solving) when they couldn’t control external pressures like tariffs and EV cost recovery. Return-to-office mandates increased buyer availability. And a growing “permacrisis” awareness drove both OEMs and suppliers toward more collaborative approaches. The 10,000+ supplier comments -- triple prior years -- suggest an industry-wide shift toward mutual recognition that cooperation beats adversarial negotiation in volatile conditions.

What are the Six Cs in the WRI framework?

The Six Cs are controllable behaviors that Dr. Angela Johnson identified as distinguishing OEMs with strong supplier relations: commercial fairness (equitable risk sharing), consistency (reliable scheduling), clear expectations (unambiguous requirements), communication (proactive and simple), continuity (strategy that survives leadership changes), and collaboration (genuine joint problem-solving). They form a progression from transactional to relational.

Why do Top 50 suppliers rate the Detroit Three lower than Japanese OEMs?

Top 50 North American suppliers carry deeper institutional memory from decades of OEM interactions. Toyota, Honda, and Nissan benefit from historically collaborative supplier cultures, while GM, Ford, and Stellantis are still working to overcome what Dr. Johnson calls “the cultural inertia of historically adversarial purchasing organizations.” Top 50 suppliers also face larger dollar impacts from tariffs and EV write-offs, making their assessments of commercial fairness more pointed.

How does the WRI correlate with business outcomes?

Twenty-six years of WRI data demonstrate that OEMs with higher supplier relations scores consistently receive better pricing, earlier access to new technology, preferential capacity allocation during shortages, greater supplier investment in quality systems, and faster problem resolution. The relationship is bidirectional -- OEMs that invest in supplier relations earn returns that contribute to operating profits and competitive strength.

How can non-automotive procurement leaders apply the WRI findings?

The Six Cs framework translates directly to any industry. Commercial fairness, consistency, clear expectations, communication, continuity, and collaboration are the behaviors that distinguish strategic supplier partnerships from transactional vendor management regardless of sector. Companies that measure and improve these dimensions with their supply base consistently see better cost outcomes, faster innovation cycles, and more resilient supply chains.

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Trusted by:

Trusted by:

Trusted by: