The Other Half of the Survey

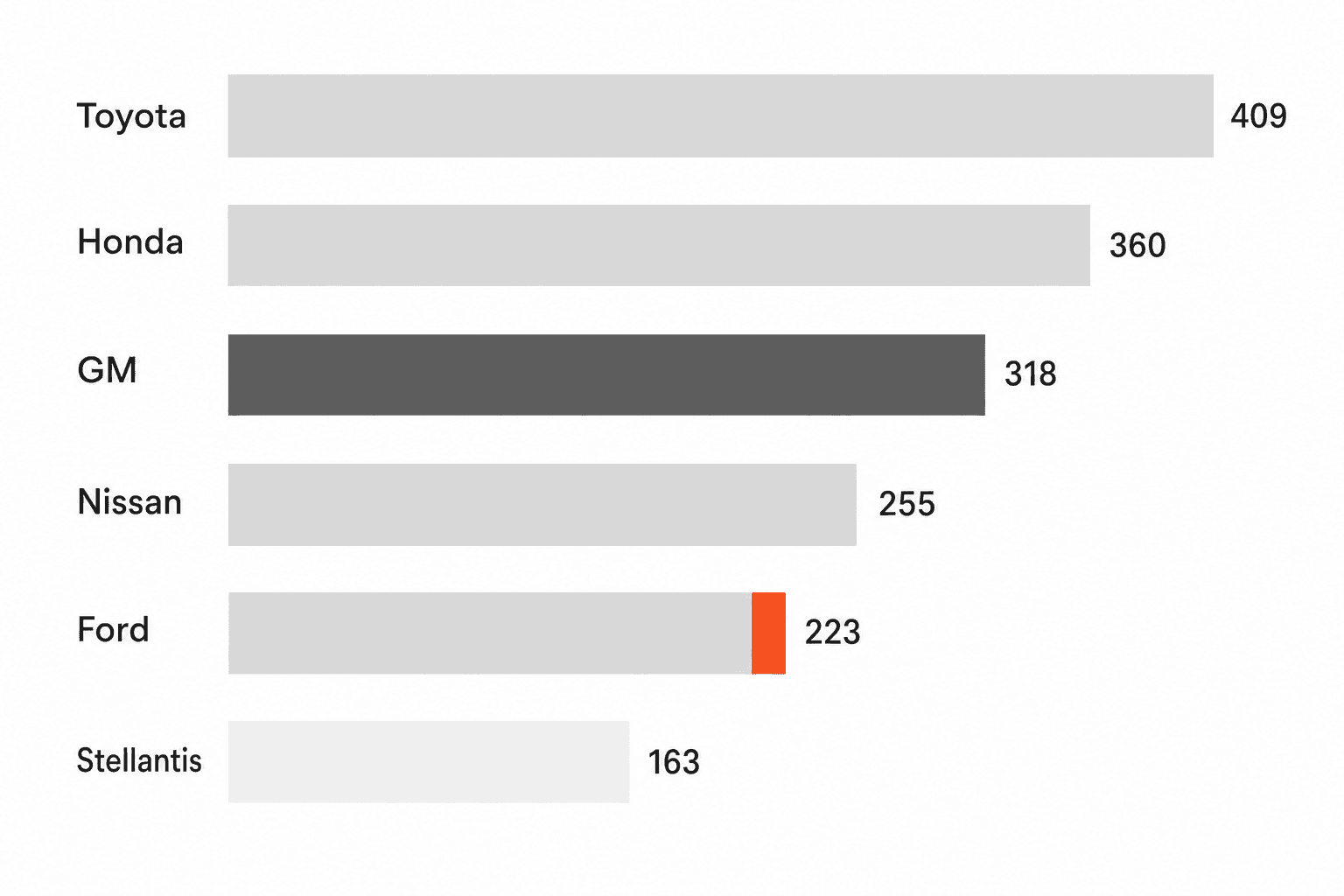

Plante Moran's 2026 Working Relations Index made headlines for the right reason: for the first time in 26 years, all six North American OEMs improved their supplier relations scores simultaneously. Toyota hit 409, Ford posted the largest single-year gain in company history (+32), and even Stellantis -- perennial last place -- climbed 22 points to 163.

But the most revealing data point in the entire study wasn't the headline scores. It was a quiet analytical footnote buried beneath them.

When Plante Moran isolated the Top 50 North American suppliers and compared their responses to the broader sample, the results diverged sharply. The Top 50 rated Toyota, Honda, and Nissan above their overall averages. They rated GM, Ford, and Stellantis below theirs -- particularly on trust, communication, and profit opportunity. The gap was large enough for the study's authors to call it out explicitly.

The math is inescapable: if the biggest suppliers are pulling Detroit's scores down, someone else is pulling them up. That someone is suppliers ranked 51 through 100 -- the mid-tier Tier 1s who don't make the Automotive News top banner but represent billions in annual buy. Their responses tell a different story than the mega-suppliers'. And in many ways, it's a more useful one.

The Top 50 tell you what the system has been. Suppliers 51-100 tell you where it's actually moving.

What Institutional Memory Actually Costs

Dr. Angela Johnson, the principal leading Plante Moran's WRI practice, put it plainly: "Organizational memory is very long. The Detroit Three are still fighting to overcome the cultural inertia of historically adversarial purchasing organizations."

She's referencing specific history, not vague sentiment. At GM, Jose Ignacio Lopez de Arriortua ran purchasing in the early 1990s with a style that Automotive News later described as using "emotion, flattery, jokes, threats, ruthlessness, even lying if need be" to extract price cuts from suppliers. He shredded contracts, demanded price reduction after price reduction, and saved GM roughly $4 billion in a single year -- while leaving a supply base that still remembers the experience three decades later. As late as 2016, trade press still described GM as "changing its heavy-handed ways a bit" after "decades as the procurement bad guy."

At Chrysler -- now part of Stellantis -- Sergio Marchionne's cost focus through the 2010s left a similar mark. By 2022, Stellantis's WRI score had dropped to 128, the lowest in the study, after losing 122 points over nine years. His successor Carlos Tavares, who resigned under pressure in December 2024, continued the cost-cutting ethos until the board and the UAW effectively forced him out. Stellantis is now under CEO Antonio Filosa, who suppliers describe as "more predictable" -- a low bar that still represents progress.

Ford's history is less dramatic but consistent. A 2008 dispute where Navistar halted engine shipments to Ford -- because Ford had demanded the supplier sell at a loss -- became a textbook example of the procurement relationship gone wrong.

These aren't just stories. They're the institutional memory that the WRI measures -- and the Top 50 suppliers carry them in ways that the 51-100 cohort does not.

Why Smaller Suppliers See Things Differently

The Top 50 North American automotive suppliers are companies like Magna, Denso, BorgWarner, Aptiv, and ZF -- firms with $5-40 billion in annual revenue, thousands of employees dedicated to OEM account management, and decades-deep relationships with every major automaker. When a Magna VP fills out the WRI survey, they're drawing on 30 years of experience with that OEM, including every contract dispute, every unilateral cost-down, and every broken promise from 2003.

A supplier ranked 65th looks different. Maybe $1-3 billion in revenue. Maybe they won their first GM contract in 2018. Maybe the buyer they work with was hired in 2020 and has no memory of the Lopez era because she wasn't born when it happened.

Three things change when you move down the supplier ranking:

Shorter institutional memory. A mid-tier supplier's relationship with an OEM might be 8-10 years old, not 30. Their frame of reference is the current purchasing team, not the historical purchasing culture. When that team is responsive and fair -- as the 2026 data suggests many were -- the score reflects reality as-is, not reality-as-inherited.

Less political calculation. Large suppliers have sophisticated OEM relationship management. Their survey responses may pass through internal review. They consider the strategic implications of their ratings. A mid-tier supplier's sales VP fills out the survey based on last quarter's experience. The response is more personal, less filtered, and more directly tied to what's actually happening in the buying relationship today.

Different pain thresholds. Academic research on B2B relationship satisfaction shows that smaller firms place extraordinary weight on procedural fairness -- whether the process feels respectful -- sometimes even more than on financial outcomes. A mid-tier supplier might rate an OEM well because the buyer returns calls within 24 hours and provides stable forecasts, even if margins are tight. A Top 50 supplier expects all of that as table stakes and grades on whether the OEM is sharing cost savings and offering long-term program commitments.

The result: mid-tier suppliers are grading on what's happening now, while the mega-suppliers are grading on a 25-year cumulative track record. Both perspectives are valid. But only one of them tells you whether the OEM's behavior is actually changing.

The Japanese Halo May Be Thinner Than It Looks

Here's the flip side that most WRI coverage ignores: if the Top 50 are rating Japanese OEMs above average, then suppliers 51-100 must be rating them below average. Toyota and Honda still lead the overall rankings by a wide margin -- but their advantage may be concentrated among their oldest, deepest partnerships.

This makes structural sense. Toyota's keiretsu model -- close-knit supplier networks built on decades of mutual investment and shared success -- is genuinely excellent. ASU professor Thomas Choi described it as a "supplier-partnering hierarchy" where Toyota operates on the belief that "the suppliers' success is absolutely crucial to their own." The result: 17 consecutive years atop the WRI.

But keiretsu relationships are densest among the largest suppliers. Denso, Aisin, and other traditional Toyota partners benefit from decades of co-development, shared engineering resources, and stable long-term contracts. A $1.5 billion supplier that won a Toyota contract six years ago gets a different version of the Toyota experience -- likely still good, but perhaps not the platinum-tier partnership that earns 409 scores.

This doesn't diminish Toyota's lead. It contextualizes it. The keiretsu advantage is real, but it's not uniformly distributed. And if Japanese OEMs assume their supplier reputation sells itself to every tier of partner, they may be surprised when the mid-tier starts comparing their experience with a Detroit OEM that's actively improving its purchasing behavior.

10,000 Comments and the Candor Signal

The 2026 WRI study collected more than 10,000 written supplier comments -- a 3.5x increase over the roughly 2,800 comments in prior years. The respondent count only increased from 665 to 750. So the comment-per-respondent ratio roughly tripled.

This isn't noise. When people write more, it means they have more to say -- and they believe it's worth saying. Dr. Johnson described the comments as revealing "an emerging, collective recognition that working together is the best way to face permacrisis challenges."

But there's a reading-between-the-lines interpretation too. A 3.5x increase in qualitative feedback suggests that suppliers outside the traditional Top 50 power structure are engaging with the survey more actively. For years, the WRI was primarily a megasupplier exercise -- a prestigious check-in between the largest Tier 1s and their OEM customers. The broader respondent engagement in 2026 means mid-tier suppliers aren't just ticking boxes. They're writing paragraphs. They're using the survey as a communication channel, not just a scorecard.

That shift matters because it changes whose voice the WRI captures. When 42 of the Top 50 suppliers dominate the sample, you get a study that mostly reflects the concerns of $10 billion companies. When the other 36 respondents from the 51-100 tier write three times as many comments, the study starts to reflect a broader -- and arguably more representative -- supplier experience.

The Six Cs Through a Different Lens

Plante Moran's Six Cs framework -- Commercial fairness, Consistency, Clear expectations, Communication, Continuity, and Collaboration -- describes the controllable behaviors that separate strong OEM-supplier relationships from weak ones. Johnson structures them as a pyramid from transactional (commercial fairness at the base) to relational (collaboration at the apex).

The 2026 data showed that the Top 50's harshest ratings for the Detroit Three concentrated in trust, communication, and profit opportunity. Mapped onto the Six Cs, that's a deficit in Commercial Fairness and Communication -- the foundational layers.

But when you consider that overall scores rose despite the Top 50 pulling them down, the 51-100 cohort must be rating these foundational behaviors positively. This tells us something specific: the day-to-day purchasing experience at Detroit OEMs has genuinely improved for suppliers who don't carry historical baggage.

The 2026 WRI review on this blog covered the macro story -- all six OEMs improving, Ford's +32 point surge under Liz Door, the framework itself. But the Top 50 gap suggests that improvement is felt unevenly. If you're a $2 billion supplier who values clear communication and consistent forecasts, the Detroit Three are better partners than they were five years ago. If you're a $15 billion supplier who remembers what happened the last three times an OEM promised to share cost savings, you're not convinced yet.

This is the fundamental tension the WRI exposes: current behavior vs. cumulative reputation. The Top 50 are measuring reputation. The 51-100 are measuring behavior. Both are real. But for an OEM trying to understand whether its improvement initiatives are working, the mid-tier signal is the leading indicator.

Don't Mistake Relief for Trust

Ford's 32-point surge -- driven largely by Chief Supply Chain Officer Liz Door's commitment to getting out into the supply base, implementing two-way supplier scorecards, and driving transparency -- is the clearest example of behavioral change producing results. Johnson noted specifically that Door "started with how she was spending her time and how much she was getting out there in the supply base." That's Communication and Consistency in the Six Cs framework. It's the exact set of behaviors that mid-tier suppliers reward most heavily.

But Ford's Top 50 scores still lagged its overall average. The mega-suppliers noticed the improvement but haven't fully credited it yet. They're waiting to see whether it sticks. And they should -- consistency over time is what separates a real cultural shift from a single good year under a charismatic leader.

Here's what OEM executives should understand about the difference: a mid-tier supplier whose buyer is suddenly accessible and whose forecasts are suddenly stable may score the OEM higher. But that's relief, not trust. Relief is what you feel when something stops being bad. Trust is what builds after years of consistent behavior. The 51-100 cohort is expressing relief. The Top 50 won't express trust until the pattern holds.

And the real risk of poor supplier relations isn't that suppliers refuse the business. It's quieter than that. Suppliers who don't trust an OEM still accept contracts -- but they assign their B-team engineers, hold back their best ideas, price in risk premiums, and reduce discretionary support. The WRI measures perception. The financial impact shows up later, in launch delays, quality escapes, and uncompetitive pricing.

GM's all-time-high score of 318 sits in a revealing middle ground. Strong enough to reach "adequate" on the WRI scale, but still 91 points below Honda. GM has made genuine progress -- particularly on EV cost recovery -- but the legacy of Lopez still shows up in how the largest suppliers rate trust.

Stellantis at 163, even with a 22-point improvement, remains in "poor" territory. The Filosa era is young. Suppliers are watching, and the 51-100 cohort is giving him credit for predictability and accessibility. Whether the Top 50 follow depends on whether Stellantis can sustain this for three or four consecutive years -- long enough to begin overwriting the Marchionne and Tavares chapters.

The Leading Indicator

Twenty-six years of WRI data shows a clear correlation between supplier relations scores and OEM profitability. OEMs with stronger partnerships receive competitive pricing, faster innovation cycles, and lower operating costs. The Top 50 suppliers control the bulk of that value. So while the 51-100 cohort may be more candid and more present-tense in their evaluations, the Top 50's grudging approval is ultimately what moves the needle on financial performance.

If you're an OEM executive reading the WRI, the top-line score is your report card. But the gap between how your largest suppliers rate you and how your mid-tier suppliers rate you is your leading indicator. A shrinking gap means you're building trust that compounds. A persistent gap means your improvement is real but hasn't overcome the weight of history yet.

The good news for the Detroit Three: the 51-100 data proves the behavioral change is real. Buyers are more accessible. Forecasts are more stable. Communication has improved. The hard news: the suppliers with the longest memories are the ones writing the biggest checks. Winning them over takes years, not quarters.

Sources

Plante Moran 2026 WRI Press Release -- Full study results, Top 50 analysis, Six Cs framework, and Dr. Johnson quotes

Automotive Logistics: North American OEMs Improve Supplier Relations in 2026 WRI -- Detailed analysis of OEM improvements, Liz Door's impact, and institutional memory

Assembly Magazine: Automaker-Supplier Relations Improve Despite Tariff, EV Pressures -- Score breakdowns, scoring scale details, and supply chain transparency tensions

Collision Repair Magazine: A Price on Friendship -- Stellantis Supplier Relations Decline -- Stellantis's 122-point decline over nine years

SCDigest: GM Changes Its Heavy-Handed Ways -- Lopez era history, GM's adversarial purchasing reputation, and Ford-Navistar dispute

ASU W.P. Carey: Deep Supplier Relationships Drive Automakers' Success -- Toyota keiretsu model, supplier-partnering hierarchy

CNN: Stellantis CEO Carlos Tavares Steps Down -- Tavares resignation context, December 2024

UCLouvain: Fairness and Relationship Quality in B2B Partnerships -- Academic research on procedural fairness weighting by firm size

Frequently Asked Questions

What is the Plante Moran Working Relations Index?

The Working Relations Index is an annual study founded by Dr. John Henke in 2001 and acquired by Plante Moran in 2019. It surveys Tier 1 supplier executives across 23 variables covering trust, communication, help, hindrance, and profit opportunity to quantitatively rank how six major North American OEMs are perceived by their supply base. In 2026, the study collected 750 responses representing 78 of the top 100 North American automotive suppliers.

Why do Top 50 suppliers rate Detroit OEMs differently than smaller suppliers?

The Top 50 North American suppliers have decades-deep relationships with OEMs and carry institutional memory of past adversarial purchasing practices -- GM's Lopez era in the 1990s, Stellantis's cost-cutting under Marchionne and Tavares, and Ford's historically combative procurement culture. Suppliers ranked 51-100 tend to have shorter relationship histories, less political calculation in their survey responses, and more focus on current purchasing behavior rather than cumulative reputation.

What are the Six Cs in the WRI framework?

Plante Moran's Six Cs are six controllable behaviors that distinguish strong OEM-supplier relationships: Commercial fairness, Consistency, Clear expectations, Communication, Continuity, and Collaboration. They're structured as a pyramid progressing from transactional (commercial fairness) to relational (collaboration), with the idea that OEMs must get the foundational behaviors right before higher-level partnership is possible.

How did Ford improve its WRI score by 32 points in one year?

Ford's improvement was driven primarily by Chief Supply Chain Officer Liz Door, who was appointed in June 2023 and focused on supplier engagement, accessibility, and implementing a two-way supplier scorecard for transparency. Dr. Angela Johnson specifically credited Door with getting out into the supply base and driving her purchasing team to do the same -- behaviors that map directly to Communication and Consistency in the Six Cs framework.

Does the WRI score correlate with OEM financial performance?

Twenty-six years of WRI data demonstrates a correlation between supplier relations scores and OEM operating performance. OEMs with stronger partnerships tend to receive competitive pricing, greater supplier investment in innovation, reduced operating costs, and faster time to market. The relationship is not strictly causal -- many factors contribute to profitability -- but the directional correlation has been consistent across the study's history.

What is the risk of poor supplier relations if suppliers still accept contracts?

The real cost of weak OEM-supplier relations is not supplier refusal -- it's diminished discretionary effort. Suppliers who lack trust in an OEM still take the business but may assign less experienced teams, withhold their best innovations, add risk premiums to pricing, and reduce voluntary support during launch crises. These effects don't show up in the WRI score but eventually appear in launch timing, quality, and total cost.

The Other Half of the Survey

Plante Moran's 2026 Working Relations Index made headlines for the right reason: for the first time in 26 years, all six North American OEMs improved their supplier relations scores simultaneously. Toyota hit 409, Ford posted the largest single-year gain in company history (+32), and even Stellantis -- perennial last place -- climbed 22 points to 163.

But the most revealing data point in the entire study wasn't the headline scores. It was a quiet analytical footnote buried beneath them.

When Plante Moran isolated the Top 50 North American suppliers and compared their responses to the broader sample, the results diverged sharply. The Top 50 rated Toyota, Honda, and Nissan above their overall averages. They rated GM, Ford, and Stellantis below theirs -- particularly on trust, communication, and profit opportunity. The gap was large enough for the study's authors to call it out explicitly.

The math is inescapable: if the biggest suppliers are pulling Detroit's scores down, someone else is pulling them up. That someone is suppliers ranked 51 through 100 -- the mid-tier Tier 1s who don't make the Automotive News top banner but represent billions in annual buy. Their responses tell a different story than the mega-suppliers'. And in many ways, it's a more useful one.

The Top 50 tell you what the system has been. Suppliers 51-100 tell you where it's actually moving.

What Institutional Memory Actually Costs

Dr. Angela Johnson, the principal leading Plante Moran's WRI practice, put it plainly: "Organizational memory is very long. The Detroit Three are still fighting to overcome the cultural inertia of historically adversarial purchasing organizations."

She's referencing specific history, not vague sentiment. At GM, Jose Ignacio Lopez de Arriortua ran purchasing in the early 1990s with a style that Automotive News later described as using "emotion, flattery, jokes, threats, ruthlessness, even lying if need be" to extract price cuts from suppliers. He shredded contracts, demanded price reduction after price reduction, and saved GM roughly $4 billion in a single year -- while leaving a supply base that still remembers the experience three decades later. As late as 2016, trade press still described GM as "changing its heavy-handed ways a bit" after "decades as the procurement bad guy."

At Chrysler -- now part of Stellantis -- Sergio Marchionne's cost focus through the 2010s left a similar mark. By 2022, Stellantis's WRI score had dropped to 128, the lowest in the study, after losing 122 points over nine years. His successor Carlos Tavares, who resigned under pressure in December 2024, continued the cost-cutting ethos until the board and the UAW effectively forced him out. Stellantis is now under CEO Antonio Filosa, who suppliers describe as "more predictable" -- a low bar that still represents progress.

Ford's history is less dramatic but consistent. A 2008 dispute where Navistar halted engine shipments to Ford -- because Ford had demanded the supplier sell at a loss -- became a textbook example of the procurement relationship gone wrong.

These aren't just stories. They're the institutional memory that the WRI measures -- and the Top 50 suppliers carry them in ways that the 51-100 cohort does not.

Why Smaller Suppliers See Things Differently

The Top 50 North American automotive suppliers are companies like Magna, Denso, BorgWarner, Aptiv, and ZF -- firms with $5-40 billion in annual revenue, thousands of employees dedicated to OEM account management, and decades-deep relationships with every major automaker. When a Magna VP fills out the WRI survey, they're drawing on 30 years of experience with that OEM, including every contract dispute, every unilateral cost-down, and every broken promise from 2003.

A supplier ranked 65th looks different. Maybe $1-3 billion in revenue. Maybe they won their first GM contract in 2018. Maybe the buyer they work with was hired in 2020 and has no memory of the Lopez era because she wasn't born when it happened.

Three things change when you move down the supplier ranking:

Shorter institutional memory. A mid-tier supplier's relationship with an OEM might be 8-10 years old, not 30. Their frame of reference is the current purchasing team, not the historical purchasing culture. When that team is responsive and fair -- as the 2026 data suggests many were -- the score reflects reality as-is, not reality-as-inherited.

Less political calculation. Large suppliers have sophisticated OEM relationship management. Their survey responses may pass through internal review. They consider the strategic implications of their ratings. A mid-tier supplier's sales VP fills out the survey based on last quarter's experience. The response is more personal, less filtered, and more directly tied to what's actually happening in the buying relationship today.

Different pain thresholds. Academic research on B2B relationship satisfaction shows that smaller firms place extraordinary weight on procedural fairness -- whether the process feels respectful -- sometimes even more than on financial outcomes. A mid-tier supplier might rate an OEM well because the buyer returns calls within 24 hours and provides stable forecasts, even if margins are tight. A Top 50 supplier expects all of that as table stakes and grades on whether the OEM is sharing cost savings and offering long-term program commitments.

The result: mid-tier suppliers are grading on what's happening now, while the mega-suppliers are grading on a 25-year cumulative track record. Both perspectives are valid. But only one of them tells you whether the OEM's behavior is actually changing.

The Japanese Halo May Be Thinner Than It Looks

Here's the flip side that most WRI coverage ignores: if the Top 50 are rating Japanese OEMs above average, then suppliers 51-100 must be rating them below average. Toyota and Honda still lead the overall rankings by a wide margin -- but their advantage may be concentrated among their oldest, deepest partnerships.

This makes structural sense. Toyota's keiretsu model -- close-knit supplier networks built on decades of mutual investment and shared success -- is genuinely excellent. ASU professor Thomas Choi described it as a "supplier-partnering hierarchy" where Toyota operates on the belief that "the suppliers' success is absolutely crucial to their own." The result: 17 consecutive years atop the WRI.

But keiretsu relationships are densest among the largest suppliers. Denso, Aisin, and other traditional Toyota partners benefit from decades of co-development, shared engineering resources, and stable long-term contracts. A $1.5 billion supplier that won a Toyota contract six years ago gets a different version of the Toyota experience -- likely still good, but perhaps not the platinum-tier partnership that earns 409 scores.

This doesn't diminish Toyota's lead. It contextualizes it. The keiretsu advantage is real, but it's not uniformly distributed. And if Japanese OEMs assume their supplier reputation sells itself to every tier of partner, they may be surprised when the mid-tier starts comparing their experience with a Detroit OEM that's actively improving its purchasing behavior.

10,000 Comments and the Candor Signal

The 2026 WRI study collected more than 10,000 written supplier comments -- a 3.5x increase over the roughly 2,800 comments in prior years. The respondent count only increased from 665 to 750. So the comment-per-respondent ratio roughly tripled.

This isn't noise. When people write more, it means they have more to say -- and they believe it's worth saying. Dr. Johnson described the comments as revealing "an emerging, collective recognition that working together is the best way to face permacrisis challenges."

But there's a reading-between-the-lines interpretation too. A 3.5x increase in qualitative feedback suggests that suppliers outside the traditional Top 50 power structure are engaging with the survey more actively. For years, the WRI was primarily a megasupplier exercise -- a prestigious check-in between the largest Tier 1s and their OEM customers. The broader respondent engagement in 2026 means mid-tier suppliers aren't just ticking boxes. They're writing paragraphs. They're using the survey as a communication channel, not just a scorecard.

That shift matters because it changes whose voice the WRI captures. When 42 of the Top 50 suppliers dominate the sample, you get a study that mostly reflects the concerns of $10 billion companies. When the other 36 respondents from the 51-100 tier write three times as many comments, the study starts to reflect a broader -- and arguably more representative -- supplier experience.

The Six Cs Through a Different Lens

Plante Moran's Six Cs framework -- Commercial fairness, Consistency, Clear expectations, Communication, Continuity, and Collaboration -- describes the controllable behaviors that separate strong OEM-supplier relationships from weak ones. Johnson structures them as a pyramid from transactional (commercial fairness at the base) to relational (collaboration at the apex).

The 2026 data showed that the Top 50's harshest ratings for the Detroit Three concentrated in trust, communication, and profit opportunity. Mapped onto the Six Cs, that's a deficit in Commercial Fairness and Communication -- the foundational layers.

But when you consider that overall scores rose despite the Top 50 pulling them down, the 51-100 cohort must be rating these foundational behaviors positively. This tells us something specific: the day-to-day purchasing experience at Detroit OEMs has genuinely improved for suppliers who don't carry historical baggage.

The 2026 WRI review on this blog covered the macro story -- all six OEMs improving, Ford's +32 point surge under Liz Door, the framework itself. But the Top 50 gap suggests that improvement is felt unevenly. If you're a $2 billion supplier who values clear communication and consistent forecasts, the Detroit Three are better partners than they were five years ago. If you're a $15 billion supplier who remembers what happened the last three times an OEM promised to share cost savings, you're not convinced yet.

This is the fundamental tension the WRI exposes: current behavior vs. cumulative reputation. The Top 50 are measuring reputation. The 51-100 are measuring behavior. Both are real. But for an OEM trying to understand whether its improvement initiatives are working, the mid-tier signal is the leading indicator.

Don't Mistake Relief for Trust

Ford's 32-point surge -- driven largely by Chief Supply Chain Officer Liz Door's commitment to getting out into the supply base, implementing two-way supplier scorecards, and driving transparency -- is the clearest example of behavioral change producing results. Johnson noted specifically that Door "started with how she was spending her time and how much she was getting out there in the supply base." That's Communication and Consistency in the Six Cs framework. It's the exact set of behaviors that mid-tier suppliers reward most heavily.

But Ford's Top 50 scores still lagged its overall average. The mega-suppliers noticed the improvement but haven't fully credited it yet. They're waiting to see whether it sticks. And they should -- consistency over time is what separates a real cultural shift from a single good year under a charismatic leader.

Here's what OEM executives should understand about the difference: a mid-tier supplier whose buyer is suddenly accessible and whose forecasts are suddenly stable may score the OEM higher. But that's relief, not trust. Relief is what you feel when something stops being bad. Trust is what builds after years of consistent behavior. The 51-100 cohort is expressing relief. The Top 50 won't express trust until the pattern holds.

And the real risk of poor supplier relations isn't that suppliers refuse the business. It's quieter than that. Suppliers who don't trust an OEM still accept contracts -- but they assign their B-team engineers, hold back their best ideas, price in risk premiums, and reduce discretionary support. The WRI measures perception. The financial impact shows up later, in launch delays, quality escapes, and uncompetitive pricing.

GM's all-time-high score of 318 sits in a revealing middle ground. Strong enough to reach "adequate" on the WRI scale, but still 91 points below Honda. GM has made genuine progress -- particularly on EV cost recovery -- but the legacy of Lopez still shows up in how the largest suppliers rate trust.

Stellantis at 163, even with a 22-point improvement, remains in "poor" territory. The Filosa era is young. Suppliers are watching, and the 51-100 cohort is giving him credit for predictability and accessibility. Whether the Top 50 follow depends on whether Stellantis can sustain this for three or four consecutive years -- long enough to begin overwriting the Marchionne and Tavares chapters.

The Leading Indicator

Twenty-six years of WRI data shows a clear correlation between supplier relations scores and OEM profitability. OEMs with stronger partnerships receive competitive pricing, faster innovation cycles, and lower operating costs. The Top 50 suppliers control the bulk of that value. So while the 51-100 cohort may be more candid and more present-tense in their evaluations, the Top 50's grudging approval is ultimately what moves the needle on financial performance.

If you're an OEM executive reading the WRI, the top-line score is your report card. But the gap between how your largest suppliers rate you and how your mid-tier suppliers rate you is your leading indicator. A shrinking gap means you're building trust that compounds. A persistent gap means your improvement is real but hasn't overcome the weight of history yet.

The good news for the Detroit Three: the 51-100 data proves the behavioral change is real. Buyers are more accessible. Forecasts are more stable. Communication has improved. The hard news: the suppliers with the longest memories are the ones writing the biggest checks. Winning them over takes years, not quarters.

Sources

Plante Moran 2026 WRI Press Release -- Full study results, Top 50 analysis, Six Cs framework, and Dr. Johnson quotes

Automotive Logistics: North American OEMs Improve Supplier Relations in 2026 WRI -- Detailed analysis of OEM improvements, Liz Door's impact, and institutional memory

Assembly Magazine: Automaker-Supplier Relations Improve Despite Tariff, EV Pressures -- Score breakdowns, scoring scale details, and supply chain transparency tensions

Collision Repair Magazine: A Price on Friendship -- Stellantis Supplier Relations Decline -- Stellantis's 122-point decline over nine years

SCDigest: GM Changes Its Heavy-Handed Ways -- Lopez era history, GM's adversarial purchasing reputation, and Ford-Navistar dispute

ASU W.P. Carey: Deep Supplier Relationships Drive Automakers' Success -- Toyota keiretsu model, supplier-partnering hierarchy

CNN: Stellantis CEO Carlos Tavares Steps Down -- Tavares resignation context, December 2024

UCLouvain: Fairness and Relationship Quality in B2B Partnerships -- Academic research on procedural fairness weighting by firm size

Frequently Asked Questions

What is the Plante Moran Working Relations Index?

The Working Relations Index is an annual study founded by Dr. John Henke in 2001 and acquired by Plante Moran in 2019. It surveys Tier 1 supplier executives across 23 variables covering trust, communication, help, hindrance, and profit opportunity to quantitatively rank how six major North American OEMs are perceived by their supply base. In 2026, the study collected 750 responses representing 78 of the top 100 North American automotive suppliers.

Why do Top 50 suppliers rate Detroit OEMs differently than smaller suppliers?

The Top 50 North American suppliers have decades-deep relationships with OEMs and carry institutional memory of past adversarial purchasing practices -- GM's Lopez era in the 1990s, Stellantis's cost-cutting under Marchionne and Tavares, and Ford's historically combative procurement culture. Suppliers ranked 51-100 tend to have shorter relationship histories, less political calculation in their survey responses, and more focus on current purchasing behavior rather than cumulative reputation.

What are the Six Cs in the WRI framework?

Plante Moran's Six Cs are six controllable behaviors that distinguish strong OEM-supplier relationships: Commercial fairness, Consistency, Clear expectations, Communication, Continuity, and Collaboration. They're structured as a pyramid progressing from transactional (commercial fairness) to relational (collaboration), with the idea that OEMs must get the foundational behaviors right before higher-level partnership is possible.

How did Ford improve its WRI score by 32 points in one year?

Ford's improvement was driven primarily by Chief Supply Chain Officer Liz Door, who was appointed in June 2023 and focused on supplier engagement, accessibility, and implementing a two-way supplier scorecard for transparency. Dr. Angela Johnson specifically credited Door with getting out into the supply base and driving her purchasing team to do the same -- behaviors that map directly to Communication and Consistency in the Six Cs framework.

Does the WRI score correlate with OEM financial performance?

Twenty-six years of WRI data demonstrates a correlation between supplier relations scores and OEM operating performance. OEMs with stronger partnerships tend to receive competitive pricing, greater supplier investment in innovation, reduced operating costs, and faster time to market. The relationship is not strictly causal -- many factors contribute to profitability -- but the directional correlation has been consistent across the study's history.

What is the risk of poor supplier relations if suppliers still accept contracts?

The real cost of weak OEM-supplier relations is not supplier refusal -- it's diminished discretionary effort. Suppliers who lack trust in an OEM still take the business but may assign less experienced teams, withhold their best innovations, add risk premiums to pricing, and reduce voluntary support during launch crises. These effects don't show up in the WRI score but eventually appear in launch timing, quality, and total cost.

The Other Half of the Survey

Plante Moran's 2026 Working Relations Index made headlines for the right reason: for the first time in 26 years, all six North American OEMs improved their supplier relations scores simultaneously. Toyota hit 409, Ford posted the largest single-year gain in company history (+32), and even Stellantis -- perennial last place -- climbed 22 points to 163.

But the most revealing data point in the entire study wasn't the headline scores. It was a quiet analytical footnote buried beneath them.

When Plante Moran isolated the Top 50 North American suppliers and compared their responses to the broader sample, the results diverged sharply. The Top 50 rated Toyota, Honda, and Nissan above their overall averages. They rated GM, Ford, and Stellantis below theirs -- particularly on trust, communication, and profit opportunity. The gap was large enough for the study's authors to call it out explicitly.

The math is inescapable: if the biggest suppliers are pulling Detroit's scores down, someone else is pulling them up. That someone is suppliers ranked 51 through 100 -- the mid-tier Tier 1s who don't make the Automotive News top banner but represent billions in annual buy. Their responses tell a different story than the mega-suppliers'. And in many ways, it's a more useful one.

The Top 50 tell you what the system has been. Suppliers 51-100 tell you where it's actually moving.

What Institutional Memory Actually Costs

Dr. Angela Johnson, the principal leading Plante Moran's WRI practice, put it plainly: "Organizational memory is very long. The Detroit Three are still fighting to overcome the cultural inertia of historically adversarial purchasing organizations."

She's referencing specific history, not vague sentiment. At GM, Jose Ignacio Lopez de Arriortua ran purchasing in the early 1990s with a style that Automotive News later described as using "emotion, flattery, jokes, threats, ruthlessness, even lying if need be" to extract price cuts from suppliers. He shredded contracts, demanded price reduction after price reduction, and saved GM roughly $4 billion in a single year -- while leaving a supply base that still remembers the experience three decades later. As late as 2016, trade press still described GM as "changing its heavy-handed ways a bit" after "decades as the procurement bad guy."

At Chrysler -- now part of Stellantis -- Sergio Marchionne's cost focus through the 2010s left a similar mark. By 2022, Stellantis's WRI score had dropped to 128, the lowest in the study, after losing 122 points over nine years. His successor Carlos Tavares, who resigned under pressure in December 2024, continued the cost-cutting ethos until the board and the UAW effectively forced him out. Stellantis is now under CEO Antonio Filosa, who suppliers describe as "more predictable" -- a low bar that still represents progress.

Ford's history is less dramatic but consistent. A 2008 dispute where Navistar halted engine shipments to Ford -- because Ford had demanded the supplier sell at a loss -- became a textbook example of the procurement relationship gone wrong.

These aren't just stories. They're the institutional memory that the WRI measures -- and the Top 50 suppliers carry them in ways that the 51-100 cohort does not.

Why Smaller Suppliers See Things Differently

The Top 50 North American automotive suppliers are companies like Magna, Denso, BorgWarner, Aptiv, and ZF -- firms with $5-40 billion in annual revenue, thousands of employees dedicated to OEM account management, and decades-deep relationships with every major automaker. When a Magna VP fills out the WRI survey, they're drawing on 30 years of experience with that OEM, including every contract dispute, every unilateral cost-down, and every broken promise from 2003.

A supplier ranked 65th looks different. Maybe $1-3 billion in revenue. Maybe they won their first GM contract in 2018. Maybe the buyer they work with was hired in 2020 and has no memory of the Lopez era because she wasn't born when it happened.

Three things change when you move down the supplier ranking:

Shorter institutional memory. A mid-tier supplier's relationship with an OEM might be 8-10 years old, not 30. Their frame of reference is the current purchasing team, not the historical purchasing culture. When that team is responsive and fair -- as the 2026 data suggests many were -- the score reflects reality as-is, not reality-as-inherited.

Less political calculation. Large suppliers have sophisticated OEM relationship management. Their survey responses may pass through internal review. They consider the strategic implications of their ratings. A mid-tier supplier's sales VP fills out the survey based on last quarter's experience. The response is more personal, less filtered, and more directly tied to what's actually happening in the buying relationship today.

Different pain thresholds. Academic research on B2B relationship satisfaction shows that smaller firms place extraordinary weight on procedural fairness -- whether the process feels respectful -- sometimes even more than on financial outcomes. A mid-tier supplier might rate an OEM well because the buyer returns calls within 24 hours and provides stable forecasts, even if margins are tight. A Top 50 supplier expects all of that as table stakes and grades on whether the OEM is sharing cost savings and offering long-term program commitments.

The result: mid-tier suppliers are grading on what's happening now, while the mega-suppliers are grading on a 25-year cumulative track record. Both perspectives are valid. But only one of them tells you whether the OEM's behavior is actually changing.

The Japanese Halo May Be Thinner Than It Looks

Here's the flip side that most WRI coverage ignores: if the Top 50 are rating Japanese OEMs above average, then suppliers 51-100 must be rating them below average. Toyota and Honda still lead the overall rankings by a wide margin -- but their advantage may be concentrated among their oldest, deepest partnerships.

This makes structural sense. Toyota's keiretsu model -- close-knit supplier networks built on decades of mutual investment and shared success -- is genuinely excellent. ASU professor Thomas Choi described it as a "supplier-partnering hierarchy" where Toyota operates on the belief that "the suppliers' success is absolutely crucial to their own." The result: 17 consecutive years atop the WRI.

But keiretsu relationships are densest among the largest suppliers. Denso, Aisin, and other traditional Toyota partners benefit from decades of co-development, shared engineering resources, and stable long-term contracts. A $1.5 billion supplier that won a Toyota contract six years ago gets a different version of the Toyota experience -- likely still good, but perhaps not the platinum-tier partnership that earns 409 scores.

This doesn't diminish Toyota's lead. It contextualizes it. The keiretsu advantage is real, but it's not uniformly distributed. And if Japanese OEMs assume their supplier reputation sells itself to every tier of partner, they may be surprised when the mid-tier starts comparing their experience with a Detroit OEM that's actively improving its purchasing behavior.

10,000 Comments and the Candor Signal

The 2026 WRI study collected more than 10,000 written supplier comments -- a 3.5x increase over the roughly 2,800 comments in prior years. The respondent count only increased from 665 to 750. So the comment-per-respondent ratio roughly tripled.

This isn't noise. When people write more, it means they have more to say -- and they believe it's worth saying. Dr. Johnson described the comments as revealing "an emerging, collective recognition that working together is the best way to face permacrisis challenges."

But there's a reading-between-the-lines interpretation too. A 3.5x increase in qualitative feedback suggests that suppliers outside the traditional Top 50 power structure are engaging with the survey more actively. For years, the WRI was primarily a megasupplier exercise -- a prestigious check-in between the largest Tier 1s and their OEM customers. The broader respondent engagement in 2026 means mid-tier suppliers aren't just ticking boxes. They're writing paragraphs. They're using the survey as a communication channel, not just a scorecard.

That shift matters because it changes whose voice the WRI captures. When 42 of the Top 50 suppliers dominate the sample, you get a study that mostly reflects the concerns of $10 billion companies. When the other 36 respondents from the 51-100 tier write three times as many comments, the study starts to reflect a broader -- and arguably more representative -- supplier experience.

The Six Cs Through a Different Lens

Plante Moran's Six Cs framework -- Commercial fairness, Consistency, Clear expectations, Communication, Continuity, and Collaboration -- describes the controllable behaviors that separate strong OEM-supplier relationships from weak ones. Johnson structures them as a pyramid from transactional (commercial fairness at the base) to relational (collaboration at the apex).

The 2026 data showed that the Top 50's harshest ratings for the Detroit Three concentrated in trust, communication, and profit opportunity. Mapped onto the Six Cs, that's a deficit in Commercial Fairness and Communication -- the foundational layers.

But when you consider that overall scores rose despite the Top 50 pulling them down, the 51-100 cohort must be rating these foundational behaviors positively. This tells us something specific: the day-to-day purchasing experience at Detroit OEMs has genuinely improved for suppliers who don't carry historical baggage.

The 2026 WRI review on this blog covered the macro story -- all six OEMs improving, Ford's +32 point surge under Liz Door, the framework itself. But the Top 50 gap suggests that improvement is felt unevenly. If you're a $2 billion supplier who values clear communication and consistent forecasts, the Detroit Three are better partners than they were five years ago. If you're a $15 billion supplier who remembers what happened the last three times an OEM promised to share cost savings, you're not convinced yet.

This is the fundamental tension the WRI exposes: current behavior vs. cumulative reputation. The Top 50 are measuring reputation. The 51-100 are measuring behavior. Both are real. But for an OEM trying to understand whether its improvement initiatives are working, the mid-tier signal is the leading indicator.

Don't Mistake Relief for Trust

Ford's 32-point surge -- driven largely by Chief Supply Chain Officer Liz Door's commitment to getting out into the supply base, implementing two-way supplier scorecards, and driving transparency -- is the clearest example of behavioral change producing results. Johnson noted specifically that Door "started with how she was spending her time and how much she was getting out there in the supply base." That's Communication and Consistency in the Six Cs framework. It's the exact set of behaviors that mid-tier suppliers reward most heavily.

But Ford's Top 50 scores still lagged its overall average. The mega-suppliers noticed the improvement but haven't fully credited it yet. They're waiting to see whether it sticks. And they should -- consistency over time is what separates a real cultural shift from a single good year under a charismatic leader.

Here's what OEM executives should understand about the difference: a mid-tier supplier whose buyer is suddenly accessible and whose forecasts are suddenly stable may score the OEM higher. But that's relief, not trust. Relief is what you feel when something stops being bad. Trust is what builds after years of consistent behavior. The 51-100 cohort is expressing relief. The Top 50 won't express trust until the pattern holds.

And the real risk of poor supplier relations isn't that suppliers refuse the business. It's quieter than that. Suppliers who don't trust an OEM still accept contracts -- but they assign their B-team engineers, hold back their best ideas, price in risk premiums, and reduce discretionary support. The WRI measures perception. The financial impact shows up later, in launch delays, quality escapes, and uncompetitive pricing.

GM's all-time-high score of 318 sits in a revealing middle ground. Strong enough to reach "adequate" on the WRI scale, but still 91 points below Honda. GM has made genuine progress -- particularly on EV cost recovery -- but the legacy of Lopez still shows up in how the largest suppliers rate trust.

Stellantis at 163, even with a 22-point improvement, remains in "poor" territory. The Filosa era is young. Suppliers are watching, and the 51-100 cohort is giving him credit for predictability and accessibility. Whether the Top 50 follow depends on whether Stellantis can sustain this for three or four consecutive years -- long enough to begin overwriting the Marchionne and Tavares chapters.

The Leading Indicator

Twenty-six years of WRI data shows a clear correlation between supplier relations scores and OEM profitability. OEMs with stronger partnerships receive competitive pricing, faster innovation cycles, and lower operating costs. The Top 50 suppliers control the bulk of that value. So while the 51-100 cohort may be more candid and more present-tense in their evaluations, the Top 50's grudging approval is ultimately what moves the needle on financial performance.

If you're an OEM executive reading the WRI, the top-line score is your report card. But the gap between how your largest suppliers rate you and how your mid-tier suppliers rate you is your leading indicator. A shrinking gap means you're building trust that compounds. A persistent gap means your improvement is real but hasn't overcome the weight of history yet.

The good news for the Detroit Three: the 51-100 data proves the behavioral change is real. Buyers are more accessible. Forecasts are more stable. Communication has improved. The hard news: the suppliers with the longest memories are the ones writing the biggest checks. Winning them over takes years, not quarters.

Sources

Plante Moran 2026 WRI Press Release -- Full study results, Top 50 analysis, Six Cs framework, and Dr. Johnson quotes

Automotive Logistics: North American OEMs Improve Supplier Relations in 2026 WRI -- Detailed analysis of OEM improvements, Liz Door's impact, and institutional memory

Assembly Magazine: Automaker-Supplier Relations Improve Despite Tariff, EV Pressures -- Score breakdowns, scoring scale details, and supply chain transparency tensions

Collision Repair Magazine: A Price on Friendship -- Stellantis Supplier Relations Decline -- Stellantis's 122-point decline over nine years

SCDigest: GM Changes Its Heavy-Handed Ways -- Lopez era history, GM's adversarial purchasing reputation, and Ford-Navistar dispute

ASU W.P. Carey: Deep Supplier Relationships Drive Automakers' Success -- Toyota keiretsu model, supplier-partnering hierarchy

CNN: Stellantis CEO Carlos Tavares Steps Down -- Tavares resignation context, December 2024

UCLouvain: Fairness and Relationship Quality in B2B Partnerships -- Academic research on procedural fairness weighting by firm size

Frequently Asked Questions

What is the Plante Moran Working Relations Index?

The Working Relations Index is an annual study founded by Dr. John Henke in 2001 and acquired by Plante Moran in 2019. It surveys Tier 1 supplier executives across 23 variables covering trust, communication, help, hindrance, and profit opportunity to quantitatively rank how six major North American OEMs are perceived by their supply base. In 2026, the study collected 750 responses representing 78 of the top 100 North American automotive suppliers.

Why do Top 50 suppliers rate Detroit OEMs differently than smaller suppliers?

The Top 50 North American suppliers have decades-deep relationships with OEMs and carry institutional memory of past adversarial purchasing practices -- GM's Lopez era in the 1990s, Stellantis's cost-cutting under Marchionne and Tavares, and Ford's historically combative procurement culture. Suppliers ranked 51-100 tend to have shorter relationship histories, less political calculation in their survey responses, and more focus on current purchasing behavior rather than cumulative reputation.

What are the Six Cs in the WRI framework?

Plante Moran's Six Cs are six controllable behaviors that distinguish strong OEM-supplier relationships: Commercial fairness, Consistency, Clear expectations, Communication, Continuity, and Collaboration. They're structured as a pyramid progressing from transactional (commercial fairness) to relational (collaboration), with the idea that OEMs must get the foundational behaviors right before higher-level partnership is possible.

How did Ford improve its WRI score by 32 points in one year?

Ford's improvement was driven primarily by Chief Supply Chain Officer Liz Door, who was appointed in June 2023 and focused on supplier engagement, accessibility, and implementing a two-way supplier scorecard for transparency. Dr. Angela Johnson specifically credited Door with getting out into the supply base and driving her purchasing team to do the same -- behaviors that map directly to Communication and Consistency in the Six Cs framework.

Does the WRI score correlate with OEM financial performance?

Twenty-six years of WRI data demonstrates a correlation between supplier relations scores and OEM operating performance. OEMs with stronger partnerships tend to receive competitive pricing, greater supplier investment in innovation, reduced operating costs, and faster time to market. The relationship is not strictly causal -- many factors contribute to profitability -- but the directional correlation has been consistent across the study's history.

What is the risk of poor supplier relations if suppliers still accept contracts?

The real cost of weak OEM-supplier relations is not supplier refusal -- it's diminished discretionary effort. Suppliers who lack trust in an OEM still take the business but may assign less experienced teams, withhold their best innovations, add risk premiums to pricing, and reduce voluntary support during launch crises. These effects don't show up in the WRI score but eventually appear in launch timing, quality, and total cost.

Read more

Source Code Episode 9: Source Code: Shashi Mandapaty, Former Chief Procurement Officer at Johnson & Johnson, on Why One Throne Isn't Enough

Source Code Episode 8: Running on Paper: Rick McDonald, Chief Supply Chain Officer at Clorox, on Why Supplier Trust Is the Real Business Continuity Plan

The IEEPA Ruling Wasn't a Win. Here's What Procurement Leaders Are Missing.

Read more

Source Code Episode 9: Source Code: Shashi Mandapaty, Former Chief Procurement Officer at Johnson & Johnson, on Why One Throne Isn't Enough

Source Code Episode 8: Running on Paper: Rick McDonald, Chief Supply Chain Officer at Clorox, on Why Supplier Trust Is the Real Business Continuity Plan

The IEEPA Ruling Wasn't a Win. Here's What Procurement Leaders Are Missing.

Read more

Source Code Episode 9: Source Code: Shashi Mandapaty, Former Chief Procurement Officer at Johnson & Johnson, on Why One Throne Isn't Enough

Source Code Episode 8: Running on Paper: Rick McDonald, Chief Supply Chain Officer at Clorox, on Why Supplier Trust Is the Real Business Continuity Plan

The IEEPA Ruling Wasn't a Win. Here's What Procurement Leaders Are Missing.

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Trusted by:

Trusted by:

Trusted by:

*GARTNER is a registered trademark and service mark of Gartner, Inc. and/or its affiliates in the U.S. and internationally, and COOL VENDORS is a registered trademark of Gartner, Inc. and/or its affiliates and are used herein with permission. All rights reserved. Gartner does not endorse any vendor, product or service depicted in its research publications, and does not advise technology users to select only those vendors with the highest ratings or other designation. Gartner research publications consist of the opinions of Gartner’s research organization and should not be construed as statements of fact. Gartner disclaims all warranties, expressed or implied, with respect to this research, including any warranties of merchantability or fitness for a particular purpose.