A Leapmotor C10 was driving down a German Autobahn last year when its driver-assistance system braked hard and jerked the car sideways, as if it had been boxed in by a scooter in a Chinese megacity. The man behind the wheel was Martin Resch, who runs Leapmotor’s business in Germany. He emailed the engineers in Hangzhou to flag the problem and walked into a meeting. By the time he came out, a software update had been written, tested, and beamed to the car. The behavior was fixed. At a European carmaker, he told Bloomberg, the same fix would have taken weeks.

Related: the duty-side response to China exposure -- classification, origin, first-sale valuation, drawback, and renegotiation -- is laid out in The Buyer’s Tariff Playbook.

That gets told as a software story. I think it is really a clock story.

The industry calls it China Speed, and it has become the auto industry’s new benchmark. I’d call it something slightly different. The strange thing about Chinese EV makers is not only that they move fast. It is that they seem to operate on a different unit of time, where a sourcing question, a software defect, or a design change carries months less calendar between problem and answer than it does anywhere else. China Time.

The reflex, when people see this, is to explain it with cost. Cheap labor. State subsidies. A government that has put at least $230 billion into the EV sector since 2009, by the Center for Strategic and International Studies’ count. All of that is real, and none of it is the answer. The cost story is the comfortable story, because it lets incumbents believe the gap is a subsidy line they can lobby against rather than a way of working they would have to rebuild from the studs. The harder truth is that China’s decisive advantage is speed, and the famous cost advantage is mostly a consequence of it.

A new car in 24 months

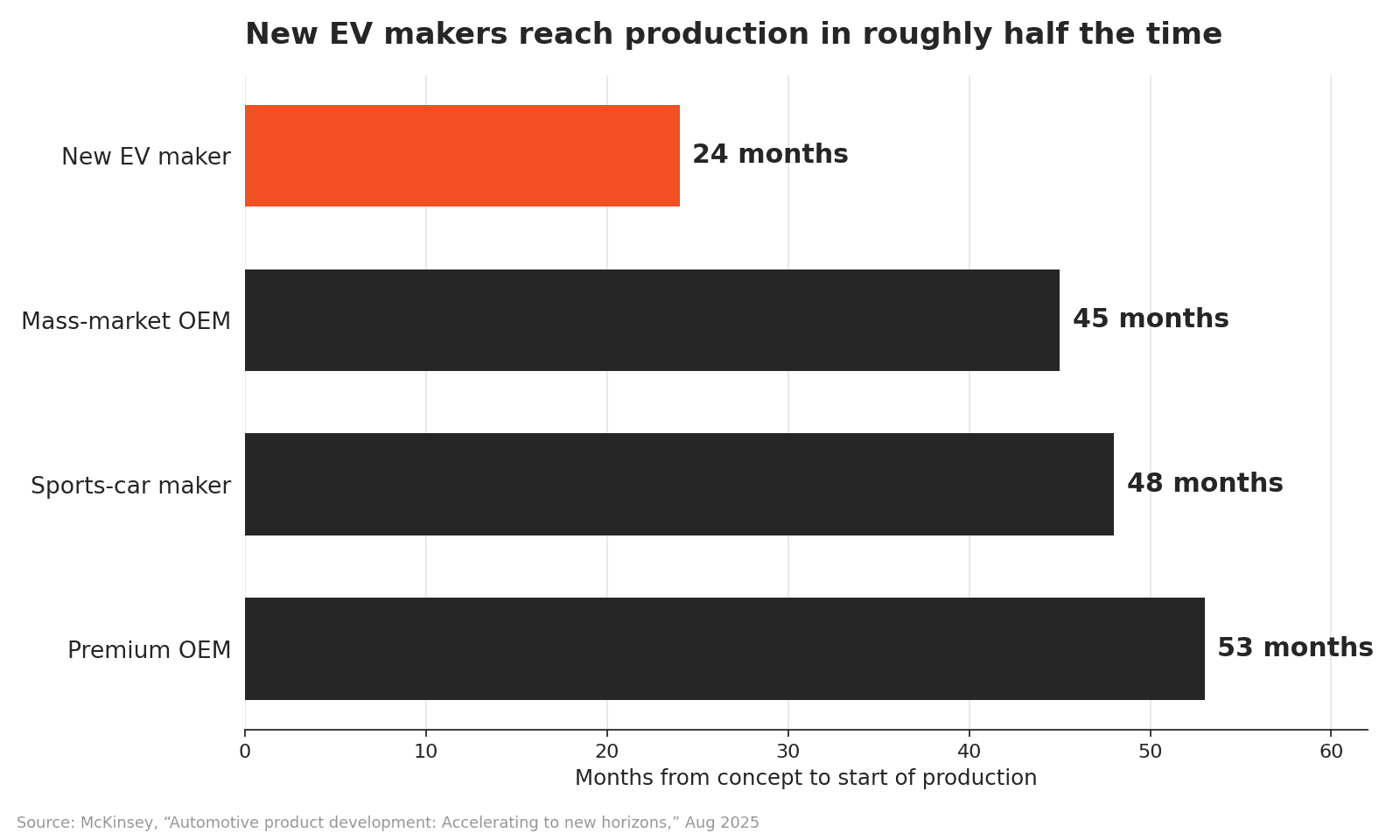

Start with the number that should bother anyone who builds physical products. McKinsey’s operations practice put hard figures on it in August 2025: China’s new EV-focused automakers take a vehicle from concept to start of production in roughly 24 months, including the platform. A mass-market Western OEM takes 45 months. A premium OEM takes 53. The Chinese newcomers run at twice the speed of the rest of the industry, and some programs are now targeting 18 months or less.

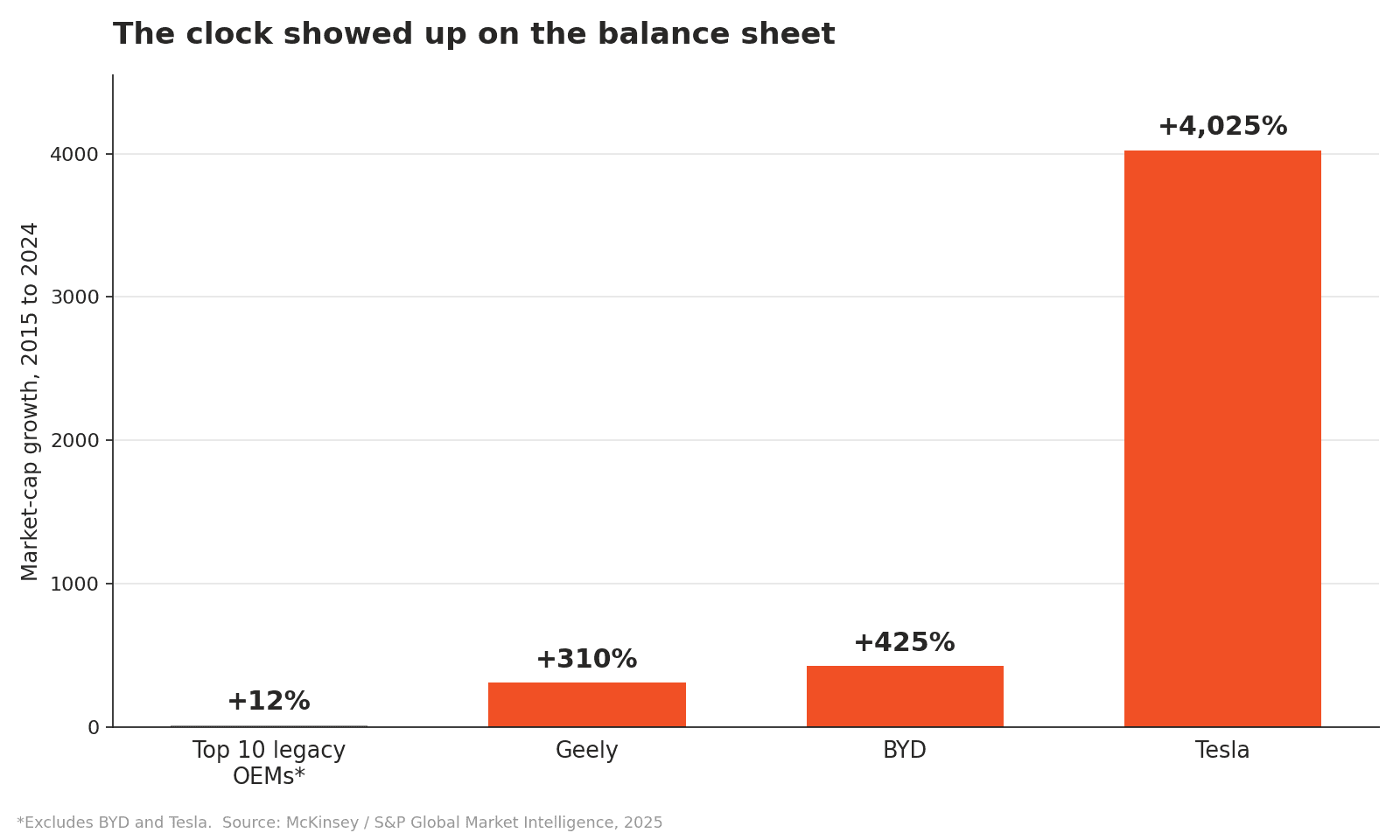

Twice the speed is not an efficiency gain. It is a different category of company. If you launch a genuinely new product every two years while your competitor launches every four to five, you get two cracks at the market for each of theirs. You fold in a new battery chemistry, a new chip, a new driver-assistance stack a full generation ahead. The compounding shows up where it counts: from 2015 to 2024, the combined market value of the ten largest legacy automakers, excluding BYD and Tesla, grew 12 percent. Geely grew 310 percent. BYD grew 425 percent. Tesla grew more than 4,000 percent. The clock showed up on the balance sheet.

This is a familiar shape, for what it’s worth. Japan did it to Detroit in the 1970s with lean production. The new wave is faster and software-shaped, but the lesson is the one the industry keeps relearning: the company that compresses the development loop wins, and everyone else spends a decade explaining why it shouldn’t have counted.

New EV makers reach start of production in roughly 24 months, against 45 to 53 for legacy OEMs. Source: McKinsey, August 2025.

Cost is the output, not the input

Here is the part that gets the story backwards. In 2024, the American benchmarking firm Caresoft Global tore down a BYD Seagull, the roughly $11,500 city car that has become the symbol of Chinese cost dominance. They expected to find the seams: the cut corners, the cheap substitutions, the evidence that this was a subsidized loss-leader held together with thin plastic. That is not what they found. They found a car that, in their words, did not come across cheap. They found that almost nothing on it was outsourced. The body panels, the light clusters, the motors, the batteries, and the power electronics were largely made by BYD itself. The low price wasn’t corner-cutting. It was engineering.

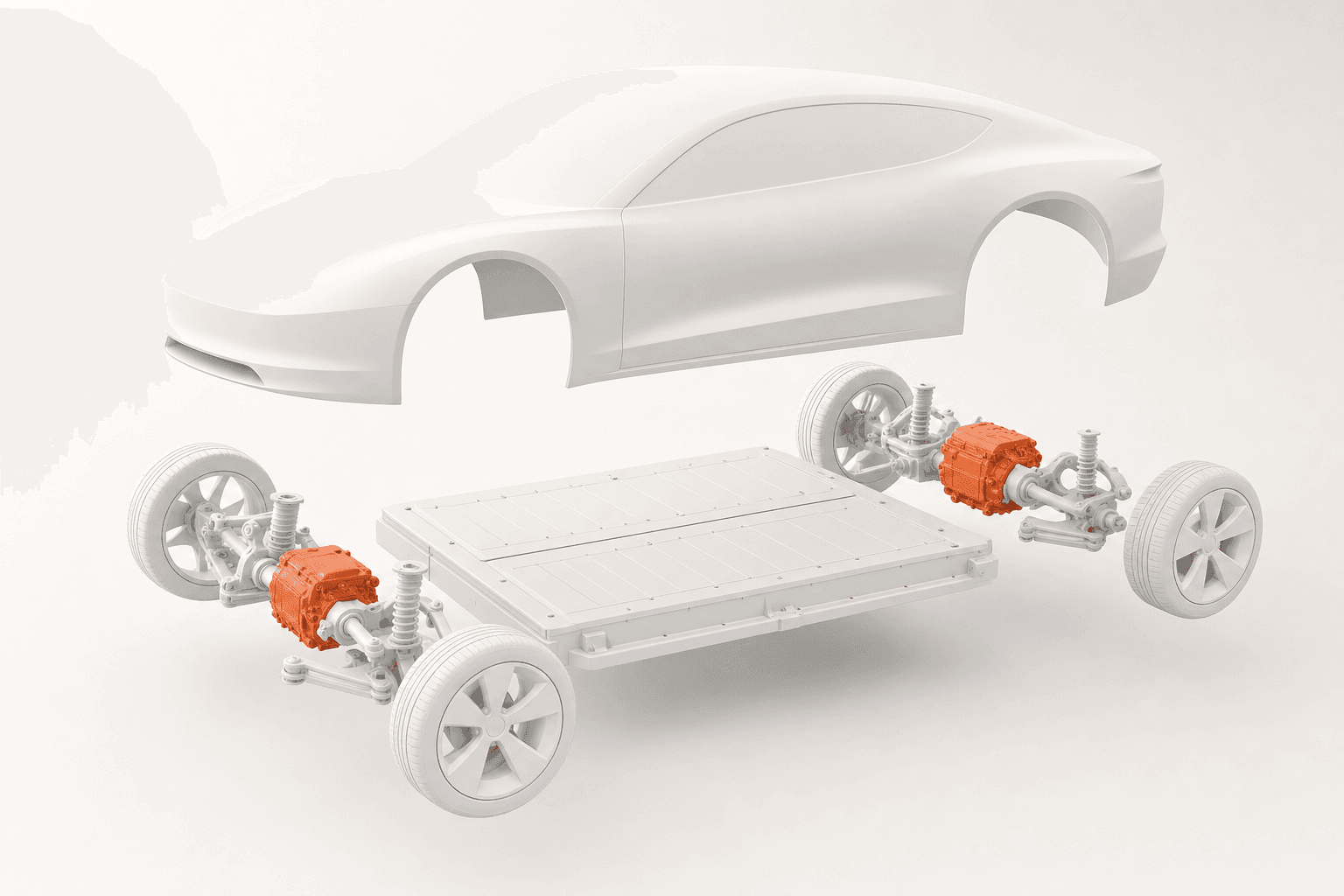

That distinction is the whole argument. Cheapness is an input you choose. Low cost can be something a system produces. BYD’s roughly $2,000-per-vehicle battery cost advantage, which UBS analysts have documented, doesn’t come from cheap labor. It comes from making its own cells at enormous scale, from a Blade battery design that removes parts, and from developing the battery and the car as one thing instead of buying the first and bolting it into the second. Xiaomi’s SU7 uses a single aluminum gigacasting in place of 72 stamped-and-welded parts, eliminating roughly 840 weld points and halving that section’s production time. None of that is a labor-rate story. It is a design-and-integration story, and the integration was only possible because one team controlled the whole stack and moved fast enough to co-optimize it.

Speed is the cause, and lower cost is the effect. A faster loop means real-world feedback arrives sooner, the expensive mistakes get caught earlier, and each generation lands cheaper than the last. The price you see at the dealership was created years before, in a development process that let the company try more designs and find out faster which cost-downs were real. That is why squeezing your own suppliers on piece price has done so little to close the gap. You can’t buy the output without rebuilding the process that produces it.

How the clock actually got compressed

So how is the loop compressed? Not with one trick. With a stack of them, each shaving weeks or months off a process the West runs end to end. McKinsey’s teardown of the development process is the clearest I’ve seen, and it matches what I watched firsthand in the EV and autonomy world, from Tesla to Waymo. The levers:

Lever | Time saved (concept-to-SOP) | What it actually is |

|---|---|---|

Smart, virtual testing | 9-11 months | 65% of testing in simulation vs 40-50% elsewhere; physical prototypes roughly halved |

Decoupling software from hardware | 3-10 months | Centralized electronics plus full over-the-air updates, so the car ships before every feature is final |

Vertical integration | 3-4 months | In-house batteries, motors, e-axles, with no quote-and-negotiate cycle to wait on |

Optimized tooling | 1-4 months | Soft polymer molds for test parts; tooling starts before the design is frozen |

Portfolio and parts reuse | 1-3 months | Fewer trims, modular platforms, parts carried over from prior models |

Execution rigor | 1-3 months | Four or five executives in stand-ups several times a week, deciding on the spot |

The biggest item on that list is not a factory or a subsidy. It is the willingness to overlap stages the West runs in sequence. John Paul MacDuffie, who studies Chinese production methods at Wharton, put it plainly to Bloomberg: “Much of the speed comes from companies beginning production before validation is complete, and compressing development stages so they overlap rather than waiting for the previous phase to finish.” Western development is a relay race, where each runner waits for the baton. China runs it as a scrum. That is a dangerous sentence, and it is also the sentence that explains most of the speed.

Three things keep that from collapsing into chaos. The first is software: Chinese EV makers, like Tesla, build on centralized electronic architectures and ship full over-the-air updates, so the car doesn’t have to be finished at launch. It has to be good enough to homologate, and the rest arrives later, the way your phone does. The Leapmotor fix on the Autobahn was that principle working as designed. The second is geography, which I’ll come back to. The third is vertical integration, which sounds like a cost play but is really a speed play: when you own the battery and the motor and the control unit, you don’t spend four months sending specs over a wall to a supplier and waiting to learn what’s hard to make.

That last point is where the quietest part of the lesson lives. McKinsey’s description of how the fast OEMs source is worth reading slowly: their procurement teams review early-stage designs “to let engineering know if any requirements will be difficult to source.” In a normal stage-gate program, engineering hands a finished design to procurement, and the buyer is then measured on price even though most of the cost and much of the schedule risk is already locked into the drawing. China Time moves the buyer, the supplier, and the manufacturing engineer to the front of the process, where changing a decision is still cheap. This is early supplier involvement run as a daily habit rather than a workshop slide.

Even component reuse, the least glamorous lever, is really about time. Automotive Manufacturing Solutions reports that BYD and Zeekr use AI to search twenty years of internal design libraries and reuse a part rather than draw a new one. A carried-over bracket, connector, or software module skips its sourcing, testing, tooling, and qualification work entirely. For anyone running new product introduction, reuse isn’t conservatism. It is schedule control.

The West built the clock that now beats it

The uncomfortable part of the China Speed story is that the West did not simply miss a shift. In several cases it built the conditions for its own competitor. Tesla’s Shanghai factory opened in 2019 and pulled design, manufacturing, and suppliers into tight physical proximity. In the Yangtze River Delta around Shanghai, an EV maker can now source nearly every component within a 200-mile radius. A prototype part that takes two days instead of two weeks changes the design conversation. A supplier engineer who can be on your factory floor tomorrow changes the tooling conversation. Tesla helped seed that supplier cluster, and the cluster now lets dozens of Chinese companies move at speeds Tesla itself has to respect.

The same reversal is running through intellectual property and platform strategy. WIPO data cited by Bloomberg shows China generated more than 343,000 patents in future land-transport technology between 2000 and 2023, about five times Germany’s total. Western automakers once used Chinese joint ventures to reach the market while guarding their know-how. Now the traffic moves the other way: Stellantis is weighing Leapmotor’s platforms for Fiat, Opel, and Peugeot; Volkswagen is building on Xpeng’s; Audi is developing on SAIC’s; Mercedes has held talks with Geely. Renault developed its new Twingo at a Shanghai research center and will source 40 percent of its parts, by value, from the mainland. Nissan is putting about $1.4 billion into building EVs in China for export. Even the suppliers are switching clocks. Bosch engineers in Suzhou redesigned an EV electrical connector in six months, about half the time a German team would need, while Bosch sheds thousands of jobs in Baden-Württemberg, where Carl Benz invented the automobile.

Kai Gramke of the consultancy EconSight put the new arrangement bluntly to Bloomberg: “In the past, China has bought European designed cars or US designed cars. In the future, we might be buying Chinese designed cars with all the Chinese specifics.” That is the fear European executives keep circling, the one they call their Nokia moment. Not that one Chinese car is cheaper. That the development clock moved, and they were standing on the wrong side of it.

From 2015 to 2024, the market value of the fastest companies pulled away from the field. Source: McKinsey / S&P Global Market Intelligence.

The bill comes due

It would be dishonest to make speed sound free. The same model that beams a fix to a car on the Autobahn also shipped the bug that needed fixing. China’s good-enough-at-launch culture has a growing file of cautionary tales. A fatal crash of a Xiaomi SU7 in late 2025 drew scrutiny to flush, retractable door handles after reports that rescuers couldn’t open them; this February, China’s regulators banned hidden door handles on new vehicles outright and will require mechanical releases by 2027, a world first. A Geely Lynk & Co Z20 turned its own headlights off at night because of a software glitch and crashed into a median. J.D. Power’s China dependability study has now worsened two years running, with the agency warning that shortened development cycles and cost pressure are becoming a systemic risk to quality. “Move fast and break things” is a fine motto for a web app. It reads differently at highway speed.

The economics carry their own warning, and this is the part most outside observers miss. The ferocious internal competition that produces China Time also produces a price war that erased an estimated 471 billion yuan, around $69 billion, in industry revenue between 2023 and 2025, by analyst Li Yanwei’s reckoning. Chinese plants can build 55.5 million vehicles a year against domestic demand near 23 million, so the industry runs at roughly half utilization and exports the difference. BYD posted its first annual profit decline since the pandemic. Beijing banned below-cost selling in February, and the discounting continued anyway. Several hundred EV startups have already died or been absorbed. Look closely and the overcapacity is not just a side effect; it functions like a brutal funding mechanism for learning. It pays for more experiments than a healthy industry would tolerate, and the bill arrives through bankrupt suppliers, failed startups, thin margins, and political pressure to dump cars abroad. The model is real. Whether every company running it survives is a different question.

And it does not transplant cleanly. Built in Europe or North America, a Chinese EV loses the supplier cluster, meets labor rules that forbid the hours, and runs into a liability regime that takes a dim view of shipping before validation is done. The Stellantis-Leapmotor plant coming to Spain in 2027 will be the real test of how much of China Time is a method and how much is just China.

What this means if you make anything

The auto industry is only the first test case, because cars are where the money and the cameras are. The pattern, a competitor who treats development time as the primary variable and lets cost fall out of it, is coming for consumer electronics, industrial equipment, aerospace, and anything assembled from a bill of materials. A tariff buys time against it without closing the gap. The actual defense is the unglamorous work of compressing your own loop, and the place to start is the questions your program asks.

The old question | The China Time question |

|---|---|

How do we reduce piece price after design release? | How do we get sourcing feedback while the design is still fluid? |

Which supplier can meet the spec? | Which supplier can help change the spec before it gets expensive? |

How do we finish all validation before SOP? | Which risks must close before SOP, and which can be fixed safely after? |

Make or buy, based on unit cost? | Which components control the program clock enough to justify building them? |

How do we manage the BOM? | Which parts can we reuse instead of redesign? |

How do we run the steering committee? | Who can decide today, without waiting for the monthly review? |

None of those right-hand questions require a 200-mile supplier cluster outside the door. They require engineering, procurement, and suppliers to be working off the same picture while the design is still moving, so cost and sourcing feedback reaches the drawing before it hardens. That connective tissue is the part of China Time that travels, and for most companies it now has to come from software instead of geography. It is the problem we work on at LightSource: an AI-native direct-materials sourcing system that puts engineering, procurement, and suppliers in one place so the buyer is in the room while the design still bends. Our customers are challenger manufacturers trying to win on speed against larger incumbents, which is to say they are trying to run on China Time without the cluster, the subsidies, or the 996.

The thing worth sitting with is that none of the levers on McKinsey’s list are secret, and most of them are not even Chinese. Concurrent engineering was named in Detroit. Over-the-air updates were Tesla’s. Early supplier involvement has been in procurement textbooks for thirty years. What China did was run all of them at once, with conviction, and let the clock be the boss. Time became the thing they optimized, and cost, market share, and the technical lead followed it out the door. The rest of the industry can keep arguing about whether that should have counted, or it can start its own clock.

Sources

China Is Ripping Up the Rulebook for the Global Auto Industry -- Bloomberg, March 2026. The Leapmotor Autobahn anecdote, the MacDuffie and Gramke quotes, the $230B subsidy figure, UBS battery and market-share estimates, Bosch Suzhou, and the door-handle and dependability concerns.

Automotive product development: Accelerating to new horizons -- McKinsey & Company, August 2025. The 24-vs-45-53 month development timelines, the time-saving levers, the early-procurement practice, and the market-cap comparison.

American Test Of The $11,500 BYD Seagull: ‘This Doesn’t Come Across Cheap’ -- InsideEVs, on the Caresoft Global teardown and BYD’s vertical integration.

‘China speed’ isn’t a cut-and-paste model -- Automotive World, with Arthur D. Little’s Niklas Brundin on what does and doesn’t transfer.

China Speed reshapes global vehicle manufacturing -- Automotive Manufacturing Solutions, on gigacasting, in-house ratios, and AI-driven parts reuse.

China to ban hidden car door handles on all EVs over crash safety concerns -- The Guardian, February 2026.

China’s EV price war rages on as BYD sets record discounts -- Automotive World, on the price war, overcapacity, and profitability pressure.

Frequently Asked Questions

What is “China Speed”?

China Speed is the term auto executives use for the pace at which Chinese automakers develop and update vehicles: roughly 18 to 24 months from concept to production, versus 45 to 53 months at Western OEMs, according to McKinsey. It also describes a software-style approach in which cars ship “good enough” and improve through over-the-air updates after the sale. The deeper point is that speed, not low cost, is the core advantage, and the cost advantage is largely a byproduct of the fast, vertically integrated development model.

How is “China Time” different from “China Speed”?

China Speed is the industry phrase for how fast Chinese automakers launch vehicles. China Time is a more specific way to think about it: the advantage is shorter loops between engineering, sourcing, testing, tooling, supplier feedback, and software fixes, so there is less calendar between a problem and its answer at every step.

Why isn’t cost China’s main advantage in EVs?

Cost is real but downstream. When Caresoft tore down the $11,500 BYD Seagull expecting cheap shortcuts, it found near-total vertical integration and genuine engineering instead. BYD’s roughly $2,000 battery cost edge comes from owning and scaling its own cell production, not from cheap labor. A faster development loop lowers the cost of learning and compounds over generations, so low cost is the result of speed and integration rather than the starting point.

How do Chinese automakers develop cars so fast?

They overlap development stages instead of running them in sequence, do about 65 percent of testing in simulation, decouple software from hardware so the car can ship before every feature is final, integrate vertically to skip supplier negotiation delays, cluster their supply chains within a few hours’ drive, and run lean teams that decide on the spot. McKinsey attributes specific time savings to each lever, the largest being 9 to 11 months from virtual testing. Procurement also reviews designs early, so sourcing problems surface while the design is still cheap to change.

What are the risks of the “ship-then-fix” model?

Shipping before validation is complete can put safety defects on the road. A fatal Xiaomi SU7 crash led China to ban hidden door handles, a Lynk & Co model crashed after a headlight software glitch, and J.D. Power’s China dependability scores have fallen two years running. There is also an economic risk: a domestic price war erased roughly $69 billion in industry revenue from 2023 to 2025, and Chinese plants run at about half capacity.

Can Western manufacturers copy China Speed?

Partly. Arthur D. Little argues the scale, demographics, and policy environment are specific to China, but the organizing principles travel: flatter structures, faster cycles, customer co-creation, selective vertical integration, and putting procurement inside engineering from day one. The levers themselves, from concurrent engineering to over-the-air updates to early supplier involvement, are well known and mostly not Chinese in origin. The hard part is running all of them at once and treating development time as the primary thing to optimize.

A Leapmotor C10 was driving down a German Autobahn last year when its driver-assistance system braked hard and jerked the car sideways, as if it had been boxed in by a scooter in a Chinese megacity. The man behind the wheel was Martin Resch, who runs Leapmotor’s business in Germany. He emailed the engineers in Hangzhou to flag the problem and walked into a meeting. By the time he came out, a software update had been written, tested, and beamed to the car. The behavior was fixed. At a European carmaker, he told Bloomberg, the same fix would have taken weeks.

Related: the duty-side response to China exposure -- classification, origin, first-sale valuation, drawback, and renegotiation -- is laid out in The Buyer’s Tariff Playbook.

That gets told as a software story. I think it is really a clock story.

The industry calls it China Speed, and it has become the auto industry’s new benchmark. I’d call it something slightly different. The strange thing about Chinese EV makers is not only that they move fast. It is that they seem to operate on a different unit of time, where a sourcing question, a software defect, or a design change carries months less calendar between problem and answer than it does anywhere else. China Time.

The reflex, when people see this, is to explain it with cost. Cheap labor. State subsidies. A government that has put at least $230 billion into the EV sector since 2009, by the Center for Strategic and International Studies’ count. All of that is real, and none of it is the answer. The cost story is the comfortable story, because it lets incumbents believe the gap is a subsidy line they can lobby against rather than a way of working they would have to rebuild from the studs. The harder truth is that China’s decisive advantage is speed, and the famous cost advantage is mostly a consequence of it.

A new car in 24 months

Start with the number that should bother anyone who builds physical products. McKinsey’s operations practice put hard figures on it in August 2025: China’s new EV-focused automakers take a vehicle from concept to start of production in roughly 24 months, including the platform. A mass-market Western OEM takes 45 months. A premium OEM takes 53. The Chinese newcomers run at twice the speed of the rest of the industry, and some programs are now targeting 18 months or less.

Twice the speed is not an efficiency gain. It is a different category of company. If you launch a genuinely new product every two years while your competitor launches every four to five, you get two cracks at the market for each of theirs. You fold in a new battery chemistry, a new chip, a new driver-assistance stack a full generation ahead. The compounding shows up where it counts: from 2015 to 2024, the combined market value of the ten largest legacy automakers, excluding BYD and Tesla, grew 12 percent. Geely grew 310 percent. BYD grew 425 percent. Tesla grew more than 4,000 percent. The clock showed up on the balance sheet.

This is a familiar shape, for what it’s worth. Japan did it to Detroit in the 1970s with lean production. The new wave is faster and software-shaped, but the lesson is the one the industry keeps relearning: the company that compresses the development loop wins, and everyone else spends a decade explaining why it shouldn’t have counted.

New EV makers reach start of production in roughly 24 months, against 45 to 53 for legacy OEMs. Source: McKinsey, August 2025.

Cost is the output, not the input

Here is the part that gets the story backwards. In 2024, the American benchmarking firm Caresoft Global tore down a BYD Seagull, the roughly $11,500 city car that has become the symbol of Chinese cost dominance. They expected to find the seams: the cut corners, the cheap substitutions, the evidence that this was a subsidized loss-leader held together with thin plastic. That is not what they found. They found a car that, in their words, did not come across cheap. They found that almost nothing on it was outsourced. The body panels, the light clusters, the motors, the batteries, and the power electronics were largely made by BYD itself. The low price wasn’t corner-cutting. It was engineering.

That distinction is the whole argument. Cheapness is an input you choose. Low cost can be something a system produces. BYD’s roughly $2,000-per-vehicle battery cost advantage, which UBS analysts have documented, doesn’t come from cheap labor. It comes from making its own cells at enormous scale, from a Blade battery design that removes parts, and from developing the battery and the car as one thing instead of buying the first and bolting it into the second. Xiaomi’s SU7 uses a single aluminum gigacasting in place of 72 stamped-and-welded parts, eliminating roughly 840 weld points and halving that section’s production time. None of that is a labor-rate story. It is a design-and-integration story, and the integration was only possible because one team controlled the whole stack and moved fast enough to co-optimize it.

Speed is the cause, and lower cost is the effect. A faster loop means real-world feedback arrives sooner, the expensive mistakes get caught earlier, and each generation lands cheaper than the last. The price you see at the dealership was created years before, in a development process that let the company try more designs and find out faster which cost-downs were real. That is why squeezing your own suppliers on piece price has done so little to close the gap. You can’t buy the output without rebuilding the process that produces it.

How the clock actually got compressed

So how is the loop compressed? Not with one trick. With a stack of them, each shaving weeks or months off a process the West runs end to end. McKinsey’s teardown of the development process is the clearest I’ve seen, and it matches what I watched firsthand in the EV and autonomy world, from Tesla to Waymo. The levers:

Lever | Time saved (concept-to-SOP) | What it actually is |

|---|---|---|

Smart, virtual testing | 9-11 months | 65% of testing in simulation vs 40-50% elsewhere; physical prototypes roughly halved |

Decoupling software from hardware | 3-10 months | Centralized electronics plus full over-the-air updates, so the car ships before every feature is final |

Vertical integration | 3-4 months | In-house batteries, motors, e-axles, with no quote-and-negotiate cycle to wait on |

Optimized tooling | 1-4 months | Soft polymer molds for test parts; tooling starts before the design is frozen |

Portfolio and parts reuse | 1-3 months | Fewer trims, modular platforms, parts carried over from prior models |

Execution rigor | 1-3 months | Four or five executives in stand-ups several times a week, deciding on the spot |

The biggest item on that list is not a factory or a subsidy. It is the willingness to overlap stages the West runs in sequence. John Paul MacDuffie, who studies Chinese production methods at Wharton, put it plainly to Bloomberg: “Much of the speed comes from companies beginning production before validation is complete, and compressing development stages so they overlap rather than waiting for the previous phase to finish.” Western development is a relay race, where each runner waits for the baton. China runs it as a scrum. That is a dangerous sentence, and it is also the sentence that explains most of the speed.

Three things keep that from collapsing into chaos. The first is software: Chinese EV makers, like Tesla, build on centralized electronic architectures and ship full over-the-air updates, so the car doesn’t have to be finished at launch. It has to be good enough to homologate, and the rest arrives later, the way your phone does. The Leapmotor fix on the Autobahn was that principle working as designed. The second is geography, which I’ll come back to. The third is vertical integration, which sounds like a cost play but is really a speed play: when you own the battery and the motor and the control unit, you don’t spend four months sending specs over a wall to a supplier and waiting to learn what’s hard to make.

That last point is where the quietest part of the lesson lives. McKinsey’s description of how the fast OEMs source is worth reading slowly: their procurement teams review early-stage designs “to let engineering know if any requirements will be difficult to source.” In a normal stage-gate program, engineering hands a finished design to procurement, and the buyer is then measured on price even though most of the cost and much of the schedule risk is already locked into the drawing. China Time moves the buyer, the supplier, and the manufacturing engineer to the front of the process, where changing a decision is still cheap. This is early supplier involvement run as a daily habit rather than a workshop slide.

Even component reuse, the least glamorous lever, is really about time. Automotive Manufacturing Solutions reports that BYD and Zeekr use AI to search twenty years of internal design libraries and reuse a part rather than draw a new one. A carried-over bracket, connector, or software module skips its sourcing, testing, tooling, and qualification work entirely. For anyone running new product introduction, reuse isn’t conservatism. It is schedule control.

The West built the clock that now beats it

The uncomfortable part of the China Speed story is that the West did not simply miss a shift. In several cases it built the conditions for its own competitor. Tesla’s Shanghai factory opened in 2019 and pulled design, manufacturing, and suppliers into tight physical proximity. In the Yangtze River Delta around Shanghai, an EV maker can now source nearly every component within a 200-mile radius. A prototype part that takes two days instead of two weeks changes the design conversation. A supplier engineer who can be on your factory floor tomorrow changes the tooling conversation. Tesla helped seed that supplier cluster, and the cluster now lets dozens of Chinese companies move at speeds Tesla itself has to respect.

The same reversal is running through intellectual property and platform strategy. WIPO data cited by Bloomberg shows China generated more than 343,000 patents in future land-transport technology between 2000 and 2023, about five times Germany’s total. Western automakers once used Chinese joint ventures to reach the market while guarding their know-how. Now the traffic moves the other way: Stellantis is weighing Leapmotor’s platforms for Fiat, Opel, and Peugeot; Volkswagen is building on Xpeng’s; Audi is developing on SAIC’s; Mercedes has held talks with Geely. Renault developed its new Twingo at a Shanghai research center and will source 40 percent of its parts, by value, from the mainland. Nissan is putting about $1.4 billion into building EVs in China for export. Even the suppliers are switching clocks. Bosch engineers in Suzhou redesigned an EV electrical connector in six months, about half the time a German team would need, while Bosch sheds thousands of jobs in Baden-Württemberg, where Carl Benz invented the automobile.

Kai Gramke of the consultancy EconSight put the new arrangement bluntly to Bloomberg: “In the past, China has bought European designed cars or US designed cars. In the future, we might be buying Chinese designed cars with all the Chinese specifics.” That is the fear European executives keep circling, the one they call their Nokia moment. Not that one Chinese car is cheaper. That the development clock moved, and they were standing on the wrong side of it.

From 2015 to 2024, the market value of the fastest companies pulled away from the field. Source: McKinsey / S&P Global Market Intelligence.

The bill comes due

It would be dishonest to make speed sound free. The same model that beams a fix to a car on the Autobahn also shipped the bug that needed fixing. China’s good-enough-at-launch culture has a growing file of cautionary tales. A fatal crash of a Xiaomi SU7 in late 2025 drew scrutiny to flush, retractable door handles after reports that rescuers couldn’t open them; this February, China’s regulators banned hidden door handles on new vehicles outright and will require mechanical releases by 2027, a world first. A Geely Lynk & Co Z20 turned its own headlights off at night because of a software glitch and crashed into a median. J.D. Power’s China dependability study has now worsened two years running, with the agency warning that shortened development cycles and cost pressure are becoming a systemic risk to quality. “Move fast and break things” is a fine motto for a web app. It reads differently at highway speed.

The economics carry their own warning, and this is the part most outside observers miss. The ferocious internal competition that produces China Time also produces a price war that erased an estimated 471 billion yuan, around $69 billion, in industry revenue between 2023 and 2025, by analyst Li Yanwei’s reckoning. Chinese plants can build 55.5 million vehicles a year against domestic demand near 23 million, so the industry runs at roughly half utilization and exports the difference. BYD posted its first annual profit decline since the pandemic. Beijing banned below-cost selling in February, and the discounting continued anyway. Several hundred EV startups have already died or been absorbed. Look closely and the overcapacity is not just a side effect; it functions like a brutal funding mechanism for learning. It pays for more experiments than a healthy industry would tolerate, and the bill arrives through bankrupt suppliers, failed startups, thin margins, and political pressure to dump cars abroad. The model is real. Whether every company running it survives is a different question.

And it does not transplant cleanly. Built in Europe or North America, a Chinese EV loses the supplier cluster, meets labor rules that forbid the hours, and runs into a liability regime that takes a dim view of shipping before validation is done. The Stellantis-Leapmotor plant coming to Spain in 2027 will be the real test of how much of China Time is a method and how much is just China.

What this means if you make anything

The auto industry is only the first test case, because cars are where the money and the cameras are. The pattern, a competitor who treats development time as the primary variable and lets cost fall out of it, is coming for consumer electronics, industrial equipment, aerospace, and anything assembled from a bill of materials. A tariff buys time against it without closing the gap. The actual defense is the unglamorous work of compressing your own loop, and the place to start is the questions your program asks.

The old question | The China Time question |

|---|---|

How do we reduce piece price after design release? | How do we get sourcing feedback while the design is still fluid? |

Which supplier can meet the spec? | Which supplier can help change the spec before it gets expensive? |

How do we finish all validation before SOP? | Which risks must close before SOP, and which can be fixed safely after? |

Make or buy, based on unit cost? | Which components control the program clock enough to justify building them? |

How do we manage the BOM? | Which parts can we reuse instead of redesign? |

How do we run the steering committee? | Who can decide today, without waiting for the monthly review? |

None of those right-hand questions require a 200-mile supplier cluster outside the door. They require engineering, procurement, and suppliers to be working off the same picture while the design is still moving, so cost and sourcing feedback reaches the drawing before it hardens. That connective tissue is the part of China Time that travels, and for most companies it now has to come from software instead of geography. It is the problem we work on at LightSource: an AI-native direct-materials sourcing system that puts engineering, procurement, and suppliers in one place so the buyer is in the room while the design still bends. Our customers are challenger manufacturers trying to win on speed against larger incumbents, which is to say they are trying to run on China Time without the cluster, the subsidies, or the 996.

The thing worth sitting with is that none of the levers on McKinsey’s list are secret, and most of them are not even Chinese. Concurrent engineering was named in Detroit. Over-the-air updates were Tesla’s. Early supplier involvement has been in procurement textbooks for thirty years. What China did was run all of them at once, with conviction, and let the clock be the boss. Time became the thing they optimized, and cost, market share, and the technical lead followed it out the door. The rest of the industry can keep arguing about whether that should have counted, or it can start its own clock.

Sources

China Is Ripping Up the Rulebook for the Global Auto Industry -- Bloomberg, March 2026. The Leapmotor Autobahn anecdote, the MacDuffie and Gramke quotes, the $230B subsidy figure, UBS battery and market-share estimates, Bosch Suzhou, and the door-handle and dependability concerns.

Automotive product development: Accelerating to new horizons -- McKinsey & Company, August 2025. The 24-vs-45-53 month development timelines, the time-saving levers, the early-procurement practice, and the market-cap comparison.

American Test Of The $11,500 BYD Seagull: ‘This Doesn’t Come Across Cheap’ -- InsideEVs, on the Caresoft Global teardown and BYD’s vertical integration.

‘China speed’ isn’t a cut-and-paste model -- Automotive World, with Arthur D. Little’s Niklas Brundin on what does and doesn’t transfer.

China Speed reshapes global vehicle manufacturing -- Automotive Manufacturing Solutions, on gigacasting, in-house ratios, and AI-driven parts reuse.

China to ban hidden car door handles on all EVs over crash safety concerns -- The Guardian, February 2026.

China’s EV price war rages on as BYD sets record discounts -- Automotive World, on the price war, overcapacity, and profitability pressure.

Frequently Asked Questions

What is “China Speed”?

China Speed is the term auto executives use for the pace at which Chinese automakers develop and update vehicles: roughly 18 to 24 months from concept to production, versus 45 to 53 months at Western OEMs, according to McKinsey. It also describes a software-style approach in which cars ship “good enough” and improve through over-the-air updates after the sale. The deeper point is that speed, not low cost, is the core advantage, and the cost advantage is largely a byproduct of the fast, vertically integrated development model.

How is “China Time” different from “China Speed”?

China Speed is the industry phrase for how fast Chinese automakers launch vehicles. China Time is a more specific way to think about it: the advantage is shorter loops between engineering, sourcing, testing, tooling, supplier feedback, and software fixes, so there is less calendar between a problem and its answer at every step.

Why isn’t cost China’s main advantage in EVs?

Cost is real but downstream. When Caresoft tore down the $11,500 BYD Seagull expecting cheap shortcuts, it found near-total vertical integration and genuine engineering instead. BYD’s roughly $2,000 battery cost edge comes from owning and scaling its own cell production, not from cheap labor. A faster development loop lowers the cost of learning and compounds over generations, so low cost is the result of speed and integration rather than the starting point.

How do Chinese automakers develop cars so fast?

They overlap development stages instead of running them in sequence, do about 65 percent of testing in simulation, decouple software from hardware so the car can ship before every feature is final, integrate vertically to skip supplier negotiation delays, cluster their supply chains within a few hours’ drive, and run lean teams that decide on the spot. McKinsey attributes specific time savings to each lever, the largest being 9 to 11 months from virtual testing. Procurement also reviews designs early, so sourcing problems surface while the design is still cheap to change.

What are the risks of the “ship-then-fix” model?

Shipping before validation is complete can put safety defects on the road. A fatal Xiaomi SU7 crash led China to ban hidden door handles, a Lynk & Co model crashed after a headlight software glitch, and J.D. Power’s China dependability scores have fallen two years running. There is also an economic risk: a domestic price war erased roughly $69 billion in industry revenue from 2023 to 2025, and Chinese plants run at about half capacity.

Can Western manufacturers copy China Speed?

Partly. Arthur D. Little argues the scale, demographics, and policy environment are specific to China, but the organizing principles travel: flatter structures, faster cycles, customer co-creation, selective vertical integration, and putting procurement inside engineering from day one. The levers themselves, from concurrent engineering to over-the-air updates to early supplier involvement, are well known and mostly not Chinese in origin. The hard part is running all of them at once and treating development time as the primary thing to optimize.

A Leapmotor C10 was driving down a German Autobahn last year when its driver-assistance system braked hard and jerked the car sideways, as if it had been boxed in by a scooter in a Chinese megacity. The man behind the wheel was Martin Resch, who runs Leapmotor’s business in Germany. He emailed the engineers in Hangzhou to flag the problem and walked into a meeting. By the time he came out, a software update had been written, tested, and beamed to the car. The behavior was fixed. At a European carmaker, he told Bloomberg, the same fix would have taken weeks.

Related: the duty-side response to China exposure -- classification, origin, first-sale valuation, drawback, and renegotiation -- is laid out in The Buyer’s Tariff Playbook.

That gets told as a software story. I think it is really a clock story.

The industry calls it China Speed, and it has become the auto industry’s new benchmark. I’d call it something slightly different. The strange thing about Chinese EV makers is not only that they move fast. It is that they seem to operate on a different unit of time, where a sourcing question, a software defect, or a design change carries months less calendar between problem and answer than it does anywhere else. China Time.

The reflex, when people see this, is to explain it with cost. Cheap labor. State subsidies. A government that has put at least $230 billion into the EV sector since 2009, by the Center for Strategic and International Studies’ count. All of that is real, and none of it is the answer. The cost story is the comfortable story, because it lets incumbents believe the gap is a subsidy line they can lobby against rather than a way of working they would have to rebuild from the studs. The harder truth is that China’s decisive advantage is speed, and the famous cost advantage is mostly a consequence of it.

A new car in 24 months

Start with the number that should bother anyone who builds physical products. McKinsey’s operations practice put hard figures on it in August 2025: China’s new EV-focused automakers take a vehicle from concept to start of production in roughly 24 months, including the platform. A mass-market Western OEM takes 45 months. A premium OEM takes 53. The Chinese newcomers run at twice the speed of the rest of the industry, and some programs are now targeting 18 months or less.

Twice the speed is not an efficiency gain. It is a different category of company. If you launch a genuinely new product every two years while your competitor launches every four to five, you get two cracks at the market for each of theirs. You fold in a new battery chemistry, a new chip, a new driver-assistance stack a full generation ahead. The compounding shows up where it counts: from 2015 to 2024, the combined market value of the ten largest legacy automakers, excluding BYD and Tesla, grew 12 percent. Geely grew 310 percent. BYD grew 425 percent. Tesla grew more than 4,000 percent. The clock showed up on the balance sheet.

This is a familiar shape, for what it’s worth. Japan did it to Detroit in the 1970s with lean production. The new wave is faster and software-shaped, but the lesson is the one the industry keeps relearning: the company that compresses the development loop wins, and everyone else spends a decade explaining why it shouldn’t have counted.

New EV makers reach start of production in roughly 24 months, against 45 to 53 for legacy OEMs. Source: McKinsey, August 2025.

Cost is the output, not the input

Here is the part that gets the story backwards. In 2024, the American benchmarking firm Caresoft Global tore down a BYD Seagull, the roughly $11,500 city car that has become the symbol of Chinese cost dominance. They expected to find the seams: the cut corners, the cheap substitutions, the evidence that this was a subsidized loss-leader held together with thin plastic. That is not what they found. They found a car that, in their words, did not come across cheap. They found that almost nothing on it was outsourced. The body panels, the light clusters, the motors, the batteries, and the power electronics were largely made by BYD itself. The low price wasn’t corner-cutting. It was engineering.

That distinction is the whole argument. Cheapness is an input you choose. Low cost can be something a system produces. BYD’s roughly $2,000-per-vehicle battery cost advantage, which UBS analysts have documented, doesn’t come from cheap labor. It comes from making its own cells at enormous scale, from a Blade battery design that removes parts, and from developing the battery and the car as one thing instead of buying the first and bolting it into the second. Xiaomi’s SU7 uses a single aluminum gigacasting in place of 72 stamped-and-welded parts, eliminating roughly 840 weld points and halving that section’s production time. None of that is a labor-rate story. It is a design-and-integration story, and the integration was only possible because one team controlled the whole stack and moved fast enough to co-optimize it.

Speed is the cause, and lower cost is the effect. A faster loop means real-world feedback arrives sooner, the expensive mistakes get caught earlier, and each generation lands cheaper than the last. The price you see at the dealership was created years before, in a development process that let the company try more designs and find out faster which cost-downs were real. That is why squeezing your own suppliers on piece price has done so little to close the gap. You can’t buy the output without rebuilding the process that produces it.

How the clock actually got compressed

So how is the loop compressed? Not with one trick. With a stack of them, each shaving weeks or months off a process the West runs end to end. McKinsey’s teardown of the development process is the clearest I’ve seen, and it matches what I watched firsthand in the EV and autonomy world, from Tesla to Waymo. The levers:

Lever | Time saved (concept-to-SOP) | What it actually is |

|---|---|---|

Smart, virtual testing | 9-11 months | 65% of testing in simulation vs 40-50% elsewhere; physical prototypes roughly halved |

Decoupling software from hardware | 3-10 months | Centralized electronics plus full over-the-air updates, so the car ships before every feature is final |

Vertical integration | 3-4 months | In-house batteries, motors, e-axles, with no quote-and-negotiate cycle to wait on |

Optimized tooling | 1-4 months | Soft polymer molds for test parts; tooling starts before the design is frozen |

Portfolio and parts reuse | 1-3 months | Fewer trims, modular platforms, parts carried over from prior models |

Execution rigor | 1-3 months | Four or five executives in stand-ups several times a week, deciding on the spot |

The biggest item on that list is not a factory or a subsidy. It is the willingness to overlap stages the West runs in sequence. John Paul MacDuffie, who studies Chinese production methods at Wharton, put it plainly to Bloomberg: “Much of the speed comes from companies beginning production before validation is complete, and compressing development stages so they overlap rather than waiting for the previous phase to finish.” Western development is a relay race, where each runner waits for the baton. China runs it as a scrum. That is a dangerous sentence, and it is also the sentence that explains most of the speed.

Three things keep that from collapsing into chaos. The first is software: Chinese EV makers, like Tesla, build on centralized electronic architectures and ship full over-the-air updates, so the car doesn’t have to be finished at launch. It has to be good enough to homologate, and the rest arrives later, the way your phone does. The Leapmotor fix on the Autobahn was that principle working as designed. The second is geography, which I’ll come back to. The third is vertical integration, which sounds like a cost play but is really a speed play: when you own the battery and the motor and the control unit, you don’t spend four months sending specs over a wall to a supplier and waiting to learn what’s hard to make.

That last point is where the quietest part of the lesson lives. McKinsey’s description of how the fast OEMs source is worth reading slowly: their procurement teams review early-stage designs “to let engineering know if any requirements will be difficult to source.” In a normal stage-gate program, engineering hands a finished design to procurement, and the buyer is then measured on price even though most of the cost and much of the schedule risk is already locked into the drawing. China Time moves the buyer, the supplier, and the manufacturing engineer to the front of the process, where changing a decision is still cheap. This is early supplier involvement run as a daily habit rather than a workshop slide.

Even component reuse, the least glamorous lever, is really about time. Automotive Manufacturing Solutions reports that BYD and Zeekr use AI to search twenty years of internal design libraries and reuse a part rather than draw a new one. A carried-over bracket, connector, or software module skips its sourcing, testing, tooling, and qualification work entirely. For anyone running new product introduction, reuse isn’t conservatism. It is schedule control.

The West built the clock that now beats it

The uncomfortable part of the China Speed story is that the West did not simply miss a shift. In several cases it built the conditions for its own competitor. Tesla’s Shanghai factory opened in 2019 and pulled design, manufacturing, and suppliers into tight physical proximity. In the Yangtze River Delta around Shanghai, an EV maker can now source nearly every component within a 200-mile radius. A prototype part that takes two days instead of two weeks changes the design conversation. A supplier engineer who can be on your factory floor tomorrow changes the tooling conversation. Tesla helped seed that supplier cluster, and the cluster now lets dozens of Chinese companies move at speeds Tesla itself has to respect.

The same reversal is running through intellectual property and platform strategy. WIPO data cited by Bloomberg shows China generated more than 343,000 patents in future land-transport technology between 2000 and 2023, about five times Germany’s total. Western automakers once used Chinese joint ventures to reach the market while guarding their know-how. Now the traffic moves the other way: Stellantis is weighing Leapmotor’s platforms for Fiat, Opel, and Peugeot; Volkswagen is building on Xpeng’s; Audi is developing on SAIC’s; Mercedes has held talks with Geely. Renault developed its new Twingo at a Shanghai research center and will source 40 percent of its parts, by value, from the mainland. Nissan is putting about $1.4 billion into building EVs in China for export. Even the suppliers are switching clocks. Bosch engineers in Suzhou redesigned an EV electrical connector in six months, about half the time a German team would need, while Bosch sheds thousands of jobs in Baden-Württemberg, where Carl Benz invented the automobile.

Kai Gramke of the consultancy EconSight put the new arrangement bluntly to Bloomberg: “In the past, China has bought European designed cars or US designed cars. In the future, we might be buying Chinese designed cars with all the Chinese specifics.” That is the fear European executives keep circling, the one they call their Nokia moment. Not that one Chinese car is cheaper. That the development clock moved, and they were standing on the wrong side of it.

From 2015 to 2024, the market value of the fastest companies pulled away from the field. Source: McKinsey / S&P Global Market Intelligence.

The bill comes due

It would be dishonest to make speed sound free. The same model that beams a fix to a car on the Autobahn also shipped the bug that needed fixing. China’s good-enough-at-launch culture has a growing file of cautionary tales. A fatal crash of a Xiaomi SU7 in late 2025 drew scrutiny to flush, retractable door handles after reports that rescuers couldn’t open them; this February, China’s regulators banned hidden door handles on new vehicles outright and will require mechanical releases by 2027, a world first. A Geely Lynk & Co Z20 turned its own headlights off at night because of a software glitch and crashed into a median. J.D. Power’s China dependability study has now worsened two years running, with the agency warning that shortened development cycles and cost pressure are becoming a systemic risk to quality. “Move fast and break things” is a fine motto for a web app. It reads differently at highway speed.

The economics carry their own warning, and this is the part most outside observers miss. The ferocious internal competition that produces China Time also produces a price war that erased an estimated 471 billion yuan, around $69 billion, in industry revenue between 2023 and 2025, by analyst Li Yanwei’s reckoning. Chinese plants can build 55.5 million vehicles a year against domestic demand near 23 million, so the industry runs at roughly half utilization and exports the difference. BYD posted its first annual profit decline since the pandemic. Beijing banned below-cost selling in February, and the discounting continued anyway. Several hundred EV startups have already died or been absorbed. Look closely and the overcapacity is not just a side effect; it functions like a brutal funding mechanism for learning. It pays for more experiments than a healthy industry would tolerate, and the bill arrives through bankrupt suppliers, failed startups, thin margins, and political pressure to dump cars abroad. The model is real. Whether every company running it survives is a different question.

And it does not transplant cleanly. Built in Europe or North America, a Chinese EV loses the supplier cluster, meets labor rules that forbid the hours, and runs into a liability regime that takes a dim view of shipping before validation is done. The Stellantis-Leapmotor plant coming to Spain in 2027 will be the real test of how much of China Time is a method and how much is just China.

What this means if you make anything

The auto industry is only the first test case, because cars are where the money and the cameras are. The pattern, a competitor who treats development time as the primary variable and lets cost fall out of it, is coming for consumer electronics, industrial equipment, aerospace, and anything assembled from a bill of materials. A tariff buys time against it without closing the gap. The actual defense is the unglamorous work of compressing your own loop, and the place to start is the questions your program asks.

The old question | The China Time question |

|---|---|

How do we reduce piece price after design release? | How do we get sourcing feedback while the design is still fluid? |

Which supplier can meet the spec? | Which supplier can help change the spec before it gets expensive? |

How do we finish all validation before SOP? | Which risks must close before SOP, and which can be fixed safely after? |

Make or buy, based on unit cost? | Which components control the program clock enough to justify building them? |

How do we manage the BOM? | Which parts can we reuse instead of redesign? |

How do we run the steering committee? | Who can decide today, without waiting for the monthly review? |

None of those right-hand questions require a 200-mile supplier cluster outside the door. They require engineering, procurement, and suppliers to be working off the same picture while the design is still moving, so cost and sourcing feedback reaches the drawing before it hardens. That connective tissue is the part of China Time that travels, and for most companies it now has to come from software instead of geography. It is the problem we work on at LightSource: an AI-native direct-materials sourcing system that puts engineering, procurement, and suppliers in one place so the buyer is in the room while the design still bends. Our customers are challenger manufacturers trying to win on speed against larger incumbents, which is to say they are trying to run on China Time without the cluster, the subsidies, or the 996.

The thing worth sitting with is that none of the levers on McKinsey’s list are secret, and most of them are not even Chinese. Concurrent engineering was named in Detroit. Over-the-air updates were Tesla’s. Early supplier involvement has been in procurement textbooks for thirty years. What China did was run all of them at once, with conviction, and let the clock be the boss. Time became the thing they optimized, and cost, market share, and the technical lead followed it out the door. The rest of the industry can keep arguing about whether that should have counted, or it can start its own clock.

Sources

China Is Ripping Up the Rulebook for the Global Auto Industry -- Bloomberg, March 2026. The Leapmotor Autobahn anecdote, the MacDuffie and Gramke quotes, the $230B subsidy figure, UBS battery and market-share estimates, Bosch Suzhou, and the door-handle and dependability concerns.

Automotive product development: Accelerating to new horizons -- McKinsey & Company, August 2025. The 24-vs-45-53 month development timelines, the time-saving levers, the early-procurement practice, and the market-cap comparison.

American Test Of The $11,500 BYD Seagull: ‘This Doesn’t Come Across Cheap’ -- InsideEVs, on the Caresoft Global teardown and BYD’s vertical integration.

‘China speed’ isn’t a cut-and-paste model -- Automotive World, with Arthur D. Little’s Niklas Brundin on what does and doesn’t transfer.

China Speed reshapes global vehicle manufacturing -- Automotive Manufacturing Solutions, on gigacasting, in-house ratios, and AI-driven parts reuse.

China to ban hidden car door handles on all EVs over crash safety concerns -- The Guardian, February 2026.

China’s EV price war rages on as BYD sets record discounts -- Automotive World, on the price war, overcapacity, and profitability pressure.

Frequently Asked Questions

What is “China Speed”?

China Speed is the term auto executives use for the pace at which Chinese automakers develop and update vehicles: roughly 18 to 24 months from concept to production, versus 45 to 53 months at Western OEMs, according to McKinsey. It also describes a software-style approach in which cars ship “good enough” and improve through over-the-air updates after the sale. The deeper point is that speed, not low cost, is the core advantage, and the cost advantage is largely a byproduct of the fast, vertically integrated development model.

How is “China Time” different from “China Speed”?

China Speed is the industry phrase for how fast Chinese automakers launch vehicles. China Time is a more specific way to think about it: the advantage is shorter loops between engineering, sourcing, testing, tooling, supplier feedback, and software fixes, so there is less calendar between a problem and its answer at every step.

Why isn’t cost China’s main advantage in EVs?

Cost is real but downstream. When Caresoft tore down the $11,500 BYD Seagull expecting cheap shortcuts, it found near-total vertical integration and genuine engineering instead. BYD’s roughly $2,000 battery cost edge comes from owning and scaling its own cell production, not from cheap labor. A faster development loop lowers the cost of learning and compounds over generations, so low cost is the result of speed and integration rather than the starting point.

How do Chinese automakers develop cars so fast?

They overlap development stages instead of running them in sequence, do about 65 percent of testing in simulation, decouple software from hardware so the car can ship before every feature is final, integrate vertically to skip supplier negotiation delays, cluster their supply chains within a few hours’ drive, and run lean teams that decide on the spot. McKinsey attributes specific time savings to each lever, the largest being 9 to 11 months from virtual testing. Procurement also reviews designs early, so sourcing problems surface while the design is still cheap to change.

What are the risks of the “ship-then-fix” model?

Shipping before validation is complete can put safety defects on the road. A fatal Xiaomi SU7 crash led China to ban hidden door handles, a Lynk & Co model crashed after a headlight software glitch, and J.D. Power’s China dependability scores have fallen two years running. There is also an economic risk: a domestic price war erased roughly $69 billion in industry revenue from 2023 to 2025, and Chinese plants run at about half capacity.

Can Western manufacturers copy China Speed?

Partly. Arthur D. Little argues the scale, demographics, and policy environment are specific to China, but the organizing principles travel: flatter structures, faster cycles, customer co-creation, selective vertical integration, and putting procurement inside engineering from day one. The levers themselves, from concurrent engineering to over-the-air updates to early supplier involvement, are well known and mostly not Chinese in origin. The hard part is running all of them at once and treating development time as the primary thing to optimize.

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Trusted by:

Trusted by:

Trusted by: