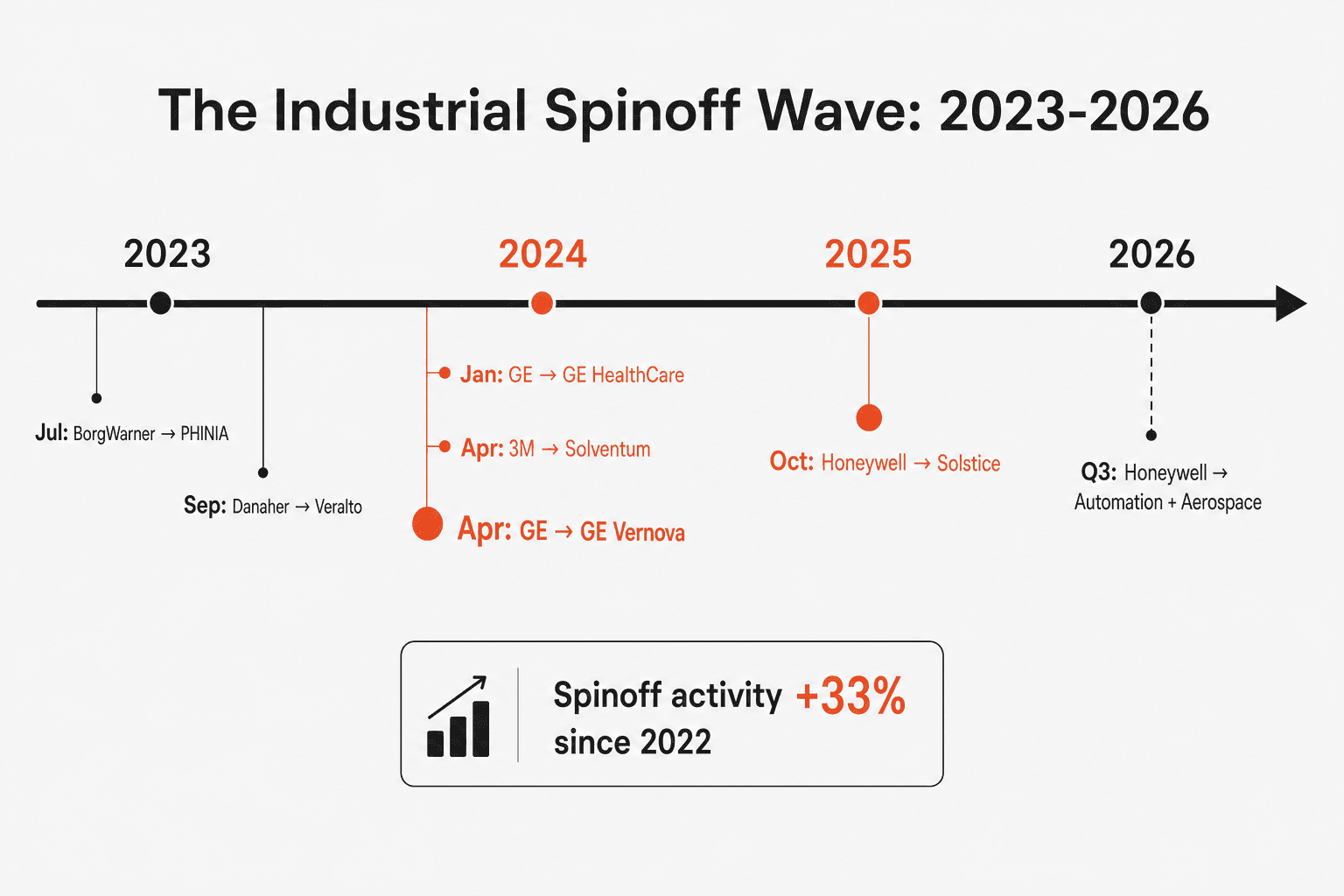

In October 2025, Honeywell completed the spinoff of its Advanced Materials business into a new company called Solstice. Six months earlier, 3M had separated its healthcare unit into Solventum. A year before that, GE finished its three-way split into GE Aerospace, GE Vernova, and GE HealthCare -- a separation that required reviewing 200,000 supplier documents and using AI to parse 7,000 contracts. Danaher spun off Veralto. BorgWarner separated PHINIA. Corporate spinoff activity surged 33% starting in 2022 and hasn't slowed.

Every one of these separations created a procurement organization that woke up one morning with fewer suppliers under contract, less purchasing volume to negotiate with, and an ERP system that used to talk to the parent's but no longer does. The strategic rationale for spinoffs is well understood -- focus, agility, market-specific capital allocation. The procurement implications are far less discussed, and they're where the real operational pain lives.

This post uses the Philips/Signify separation as a primary case study, draws on the recent wave of industrial spinoffs for patterns, and offers practical guidance for procurement leaders navigating the transition from division to standalone company.

The Signify Story: From Philips Division to Standalone Company

The timeline is instructive.

2014: Philips announces it will split into two companies -- one focused on health technology, the other on connected LED lighting.

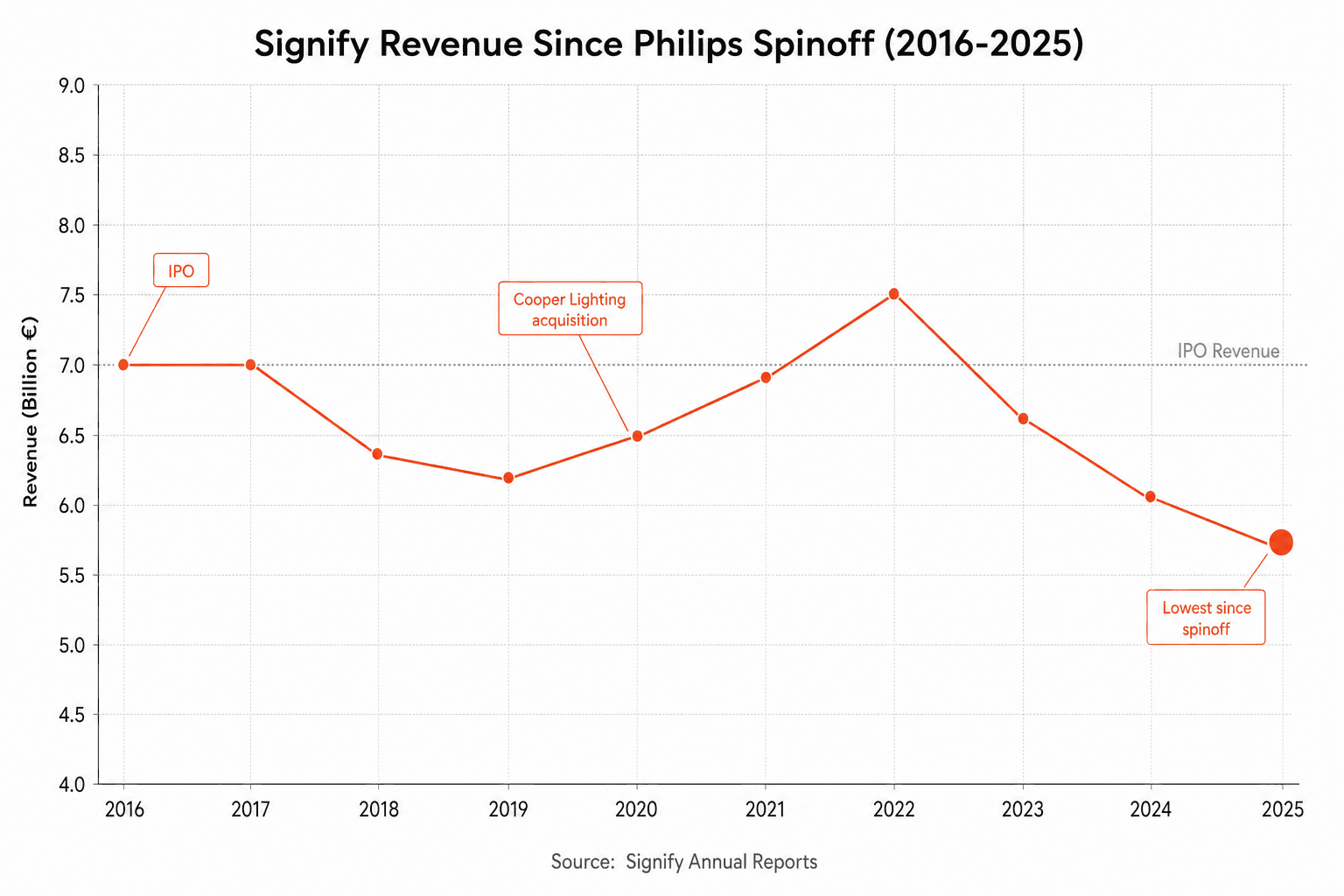

May 2016: Philips Lighting goes public on Euronext Amsterdam with an IPO valued at $3.4 billion. At separation, the business has €7 billion in revenue, 32,000 employees, and operations in more than 70 countries.

May 2018: Philips Lighting rebrands to Signify. The Philips brand continues to appear on products under a licensing agreement.

2020: Signify acquires Cooper Lighting Solutions from Eaton for $1.4 billion, expanding its North American market presence and diversifying its supplier base.

2021: Global supply chain disruptions hit Signify hard. The company reports an estimated €100 million in lost sales over a few months due to inability to source enough components -- particularly semiconductors. Without Philips' diversified supply network to fall back on, Signify struggles to requalify alternate suppliers quickly.

2023-2025: Revenue declines. Signify closes 2025 at €5.77 billion -- its lowest annual revenue since the 2016 spinoff. The company announces 900 additional job cuts. Adjusted EBITA margin falls to 8.9%.

The Signify trajectory isn't a simple decline story -- the company has maintained profitability, invested in connected lighting and IoT, and built a standalone procurement operation that functions independently. But it illustrates the core challenge: a spinoff inherits the parent's cost structure without the parent's scale. Over time, the gap between the two becomes the defining operational problem.

What Went Right

Signify started life as the world's largest lighting company. That initial scale gave it negotiating leverage with suppliers even after leaving Philips. Management ensured continuity by assigning or replicating existing Philips supplier contracts for day-one operations. The procurement team carried forward strategic sourcing practices and supplier collaboration frameworks that Philips had built over the prior decade.

The Cooper Lighting acquisition in 2020 was a smart procurement move -- it broadened the supplier base, added North American manufacturing capacity, and partially offset the volume decline in legacy categories.

What Went Wrong

The 2021 supply chain crisis exposed Signify's vulnerability. Inside Philips, the lighting division could tap the parent's diversified supplier relationships across healthcare, consumer electronics, and industrial equipment. As a standalone company, Signify's procurement team had a narrower supplier network focused exclusively on lighting components. When semiconductor shortages hit, Signify couldn't reroute demand through sister-division supplier relationships the way it could have as a Philips subsidiary.

More fundamentally, Signify's cost base was built for €7 billion in revenue. As revenue declined toward €5.8 billion, fixed procurement overhead -- supplier management staff, quality systems, logistics infrastructure -- became proportionally more expensive. The sourcing bottleneck that large companies can absorb through headcount becomes acute when the organization is leaner.

The Recent Wave: What Other Spinoffs Teach Us

Signify isn't an isolated case. The 2022-2026 wave of industrial spinoffs has generated a dataset of procurement separation experiences.

GE's Three-Way Split (2023-2024)

GE's separation into GE HealthCare (January 2023), GE Vernova (April 2024), and GE Aerospace is the most complex industrial spinoff in recent history. PwC, which advised on the deal, documented the scale of the procurement separation:

200,000+ supplier documents collected and reviewed

7,000 contracts analyzed using AI and analytics tools to identify clauses requiring renegotiation

48 ERP systems separated across the three entities

40,000+ execution actions across workstreams covering regulatory compliance, supplier relationships, IT infrastructure, and financial implications

The GE case demonstrates that procurement separation is fundamentally a data and contract problem. Every supplier agreement needs to be read, categorized, and assigned to the right entity. Every BOM needs to be mapped to the correct procurement organization. Every IT system integration needs to be severed or replicated. At GE's scale, this required AI tooling that most separations don't invest in.

3M / Solventum (April 2024)

3M's separation of its healthcare business into Solventum included an explicit SEC filing disclosure about procurement risk: "As part of 3M, Solventum currently takes advantage of 3M's size and purchasing power in procuring certain goods and services. After the separation, each of 3M and Solventum may be unable to obtain these goods, services and technologies at prices or on terms as favorable as those 3M obtained prior to completion of the separation."

That's the parent company telling shareholders, in a regulatory filing, that the spun-off entity will pay more for the same inputs. It's the clearest articulation of the procurement penalty that spinoffs face.

Solventum's filings also note that functions previously provided by 3M -- accounting, legal, HR, and critically procurement -- would need to be replicated at standalone scale. "Because of Solventum's smaller scale as a standalone company, its cost of performing such functions could be higher than the amounts reflected in Solventum's historical financial statements."

Honeywell / Solstice Advanced Materials (October 2025)

Honeywell's separation is still in progress. Solstice Advanced Materials began trading in October 2025, and the remaining Automation and Aerospace businesses are expected to separate by Q3 2026. This three-way split mirrors GE's playbook but with one important difference: Honeywell has explicitly positioned each entity as a "pure-play" market leader with dedicated go-to-market and supply chain infrastructure from day one.

The procurement challenge for Solstice is particularly acute because specialty chemicals procurement depends heavily on long-term supply agreements and sole-source relationships. When you're Honeywell, you can negotiate raw material contracts across your entire $37 billion portfolio. When you're Solstice, you're a $4 billion specialty chemicals company negotiating alone.

Danaher / Veralto (September 2023) and BorgWarner / PHINIA (July 2023)

Both completed in 2023, these separations followed the same pattern: the parent retained the higher-growth, higher-margin business while spinning off the more mature unit. Veralto (water quality and product identification) separated from Danaher's life sciences focus. PHINIA (fuel systems and aftermarket) separated from BorgWarner's electrification strategy.

In both cases, the spun-off entity faced the classic procurement challenge: the categories they buy are the same, but their leverage is smaller. A fuel systems company negotiating steel contracts carries less weight than a $14 billion powertrain conglomerate.

The Five Procurement Problems Every Spinoff Faces

Across these cases, five challenges emerge consistently.

1. Volume Leverage Evaporates

The most immediate and measurable impact. A procurement organization that negotiated as part of a $30 billion parent is now negotiating as a $5 billion standalone. Supplier pricing is volume-dependent. The same commodity, the same supplier, the same quality spec -- but the price goes up because the volume went down.

This isn't theoretical. 3M explicitly disclosed the risk in Solventum's SEC filing. Signify experienced it as revenue declined below the cost base built at separation. Every spun-off entity in the 2022-2026 wave has faced some version of this math.

2. Transition Services Agreements Create a False Sense of Security

Most spinoffs include a Transition Services Agreement (TSA) -- a temporary arrangement where the parent continues to provide certain services (IT, HR, procurement support) for 12-24 months after separation. TSAs keep the lights on during the transition, but they mask the true standalone cost.

When the TSA expires, the spun-off company must either replicate those services internally or find new providers. Procurement teams that don't begin building independent capabilities during the TSA period -- while they still have the parent's systems and support -- find themselves scrambling when the agreement ends.

3. Supplier Relationships Don't Automatically Transfer

A supplier's relationship is with the buyer they know, not with the corporate entity on the contract. When the parent's procurement VP had a 15-year relationship with a key material supplier, that relationship belonged to a person, not to a legal entity. After a spinoff, the spun-off company may have the contract but not the relationship -- and in procurement, the relationship determines whether you get the call when capacity is tight.

This is where supplier relationship management becomes critical. The spun-off entity needs to invest in rebuilding trust, demonstrating reliability, and proving that it's a customer worth prioritizing -- without the parent's brand behind it.

4. ERP and Data Systems Fracture

GE's separation required splitting 48 ERP systems. That's not a typo. Enterprise procurement systems are deeply integrated with the parent's financial, logistics, and quality infrastructure. Separating them means either:

Replicating the parent's systems at standalone scale (expensive, time-consuming)

Implementing new systems from scratch (risky, even more time-consuming)

Running on temporary workarounds that degrade data quality and spend visibility

The procurement team that can't see its own spend data can't negotiate effectively. The team running on spreadsheet workarounds while the new ERP is being implemented is losing money every day it operates blind.

5. Talent Follows the Glamour

In most spinoffs, the parent retains the business perceived as higher-growth or more strategically exciting. The spun-off entity often gets the "mature" business label. Procurement talent -- especially senior strategic sourcing leaders -- tends to follow the glamour. The spun-off company may retain the operational buyers but lose the strategic thinkers who built the category strategies, the supplier development programs, and the should-cost models that drove savings.

Practical Steps: Maintaining Supplier Credibility Without the Mothership

For procurement leaders navigating a spinoff -- whether you're on the parent side or the separated entity -- here are the moves that matter.

Before Separation (T-minus 12 to 0 Months)

1. Audit every supplier contract for assignment clauses. Many supplier agreements contain change-of-control provisions that allow the supplier to renegotiate or terminate upon a corporate event. Identify these before the separation closes, not after. GE's approach -- AI-assisted review of 7,000 contracts -- is the right model if scale demands it.

2. Build your own supplier scorecards. Don't wait until the TSA expires to understand your supplier performance independently. Start collecting delivery, quality, and responsiveness data in your own systems during the transition period.

3. Identify the 20 suppliers that matter most. In most procurement organizations, 15-20 suppliers account for 60-70% of spend. Have your CPO personally visit these suppliers, explain the separation, and make the case for why the standalone entity is a customer worth investing in. This is relationship work that can't be delegated to the contract.

During Transition (T-0 to T+18 Months)

4. Compete what you couldn't before. Ironically, a spinoff can create procurement opportunities. Categories that were locked into enterprise-wide parent contracts may now be open for competitive bidding. The parent's preferred supplier was preferred for reasons that may not apply to the standalone entity. Run competitive sourcing events on categories that haven't been market-tested in years.

5. Invest in procurement technology early. The TSA provides temporary access to the parent's systems. When that access ends, you need your own. Companies that implement their own sourcing platform during the transition -- rather than after the TSA expires -- avoid the data gap that makes the first standalone year so painful.

This is where a platform like LightSource pays for itself fastest. A spun-off entity that can run structured RFQ events, benchmark pricing against historical data, and maintain supplier performance visibility from day one of independence starts its standalone life with the same operational capability as the parent -- without the parent's headcount or legacy systems.

6. Build consortiums or buying groups. If you've lost volume leverage, find it elsewhere. Industry buying cooperatives, group purchasing organizations, or informal alliances with non-competing companies in adjacent industries can partially restore the negotiating power that the parent's scale provided.

After Independence (T+18 Months and Beyond)

7. Requalify your supply base. The suppliers you inherited from the parent aren't necessarily the right suppliers for the standalone entity. Your volumes are different. Your specifications may be evolving. Your geographic footprint may be shifting. A systematic supplier qualification program -- starting with the top 50 suppliers and working down -- ensures your supply base fits your actual needs, not the parent's.

8. Tell your supplier story. Suppliers assess customer attractiveness based on volume, growth trajectory, payment reliability, and relationship quality. A freshly spun-off company may score lower on volume but can compete on the other three dimensions. Develop a clear narrative for your supply base: where the company is headed, why you're a growth customer (even if smaller), and what makes the relationship valuable beyond purchase orders.

9. Measure the procurement cost of independence. Track the specific cost increases attributable to the separation -- higher unit prices from lost volume, standalone IT costs, incremental headcount. This data is essential for making the business case for procurement investment. If standalone procurement costs $10 million more per year than the allocated cost under the parent, that's the baseline the procurement team needs to offset through savings initiatives.

The Spinoff Scorecard: What Separates Winners from Losers

Factor | Winners | Losers |

|---|---|---|

Contract prep | AI-assisted review before Day 1 (GE model) | Discover assignment clauses after separation |

Supplier relationships | CPO visits top 20 suppliers pre-separation | Assume contracts = relationships |

Technology | Own procurement platform during TSA period | Rely on parent systems until TSA expires |

Talent | Retain strategic sourcing leaders with equity | Let talent follow the "glamour" entity |

Volume strategy | Build buying consortiums; compete locked categories | Accept higher prices as inevitable |

Timeline awareness | 18-month capability buildout plan from Day 1 | React to each challenge as it arises |

Corporate spinoffs are accelerating. Honeywell's three-way split is still in progress. The industrial conglomerate model that defined the 20th century is being systematically dismantled. Every separation creates a procurement organization that must prove it can operate without the infrastructure, volume, and brand recognition of the parent.

The companies that manage this transition well are the ones that treat procurement independence as a strategic capability to be built, not an administrative consequence to be absorbed. They invest in their own systems, their own supplier relationships, and their own data -- before the TSA expires and the parent's support disappears.

The mothership is leaving. The question is whether you've built your own engine.

Sources

Signify Company History and Performance -- Revenue decline to €5.77B in 2025, 900 job cuts, margin erosion since spinoff

Signify Official Rebrand Announcement -- Philips Lighting to Signify rebrand, May 2018

PwC -- GE Split Case Study -- 200,000+ supplier documents, 7,000 contracts, 48 ERPs, 40,000+ execution actions

Honeywell -- Solstice Advanced Materials Spinoff -- Completed October 2025; Automation and Aerospace separation expected Q3 2026

Solventum SEC Filing (Form 10-12B) -- Explicit disclosure of lost purchasing power and standalone cost increases

Signify 2024 Full-Year Results -- €6.1B sales, 9.9% operational profitability, €334M net income

Bundl -- Corporate Spin-Off Examples -- Spinoff activity surged 33% from 2022; market trend analysis

Wikipedia -- List of Largest Corporate Spin-offs -- Historical context for industrial separations

Frequently Asked Questions

Why do corporate spinoffs create procurement problems?

Spinoffs separate a business unit from the parent company's purchasing scale, supplier relationships, IT infrastructure, and procurement talent. A division that negotiated as part of a $30 billion conglomerate must now negotiate as a $5 billion standalone. Supplier pricing is volume-dependent, so the same inputs often cost more post-separation. Transition Services Agreements provide temporary support but mask the true standalone cost until they expire.

How long does it take to build independent procurement after a spinoff?

Most companies need 18-24 months to achieve full procurement independence. The first 12 months are typically covered by a Transition Services Agreement with the parent. The critical window is months 6-18, when the procurement team should be building its own systems, renegotiating supplier contracts, and establishing independent performance tracking -- while still having access to the parent's support.

What happened to Signify after the Philips spinoff?

Signify (formerly Philips Lighting) went public in 2016 with €7 billion in revenue and 32,000 employees. It built independent procurement operations and acquired Cooper Lighting for $1.4 billion in 2020. However, the 2021 supply chain crisis cost an estimated €100 million in lost sales, exposing vulnerability without Philips' diversified supplier network. By 2025, revenue had declined to €5.77 billion and the company announced 900 additional job cuts. Signify remains profitable but operates at a lower scale than its initial separation.

How can a spun-off company maintain supplier credibility without the parent's volume?

Three approaches work: (1) Compete categories that were previously locked into parent-wide contracts -- you may find better pricing than the parent's preferred suppliers offered. (2) Build buying consortiums or group purchasing arrangements with non-competing companies to partially restore volume leverage. (3) Invest in the relationship dimensions that suppliers value beyond volume: payment reliability, growth trajectory, and the quality of the buyer-supplier working relationship.

What is a Transition Services Agreement and why does it matter?

A TSA is a temporary arrangement where the parent company continues providing services (IT, procurement systems, HR) to the spun-off entity for 12-24 months after separation. TSAs are essential for operational continuity but create a false sense of security. Procurement teams that don't build independent capabilities during the TSA period face a cliff when it expires -- sudden loss of system access, spend visibility, and operational support.

Which recent spinoffs offer the best procurement lessons?

GE's three-way split is the gold standard for procurement separation at scale -- 200,000 supplier documents reviewed, AI-assisted contract analysis, and 48 ERP systems separated. 3M/Solventum's SEC filings provide the most transparent disclosure of procurement risk. Signify's decade of post-spinoff experience shows the long-term trajectory. Honeywell's ongoing separation (Solstice completed, Automation and Aerospace in 2026) will provide the next major dataset.

In October 2025, Honeywell completed the spinoff of its Advanced Materials business into a new company called Solstice. Six months earlier, 3M had separated its healthcare unit into Solventum. A year before that, GE finished its three-way split into GE Aerospace, GE Vernova, and GE HealthCare -- a separation that required reviewing 200,000 supplier documents and using AI to parse 7,000 contracts. Danaher spun off Veralto. BorgWarner separated PHINIA. Corporate spinoff activity surged 33% starting in 2022 and hasn't slowed.

Every one of these separations created a procurement organization that woke up one morning with fewer suppliers under contract, less purchasing volume to negotiate with, and an ERP system that used to talk to the parent's but no longer does. The strategic rationale for spinoffs is well understood -- focus, agility, market-specific capital allocation. The procurement implications are far less discussed, and they're where the real operational pain lives.

This post uses the Philips/Signify separation as a primary case study, draws on the recent wave of industrial spinoffs for patterns, and offers practical guidance for procurement leaders navigating the transition from division to standalone company.

The Signify Story: From Philips Division to Standalone Company

The timeline is instructive.

2014: Philips announces it will split into two companies -- one focused on health technology, the other on connected LED lighting.

May 2016: Philips Lighting goes public on Euronext Amsterdam with an IPO valued at $3.4 billion. At separation, the business has €7 billion in revenue, 32,000 employees, and operations in more than 70 countries.

May 2018: Philips Lighting rebrands to Signify. The Philips brand continues to appear on products under a licensing agreement.

2020: Signify acquires Cooper Lighting Solutions from Eaton for $1.4 billion, expanding its North American market presence and diversifying its supplier base.

2021: Global supply chain disruptions hit Signify hard. The company reports an estimated €100 million in lost sales over a few months due to inability to source enough components -- particularly semiconductors. Without Philips' diversified supply network to fall back on, Signify struggles to requalify alternate suppliers quickly.

2023-2025: Revenue declines. Signify closes 2025 at €5.77 billion -- its lowest annual revenue since the 2016 spinoff. The company announces 900 additional job cuts. Adjusted EBITA margin falls to 8.9%.

The Signify trajectory isn't a simple decline story -- the company has maintained profitability, invested in connected lighting and IoT, and built a standalone procurement operation that functions independently. But it illustrates the core challenge: a spinoff inherits the parent's cost structure without the parent's scale. Over time, the gap between the two becomes the defining operational problem.

What Went Right

Signify started life as the world's largest lighting company. That initial scale gave it negotiating leverage with suppliers even after leaving Philips. Management ensured continuity by assigning or replicating existing Philips supplier contracts for day-one operations. The procurement team carried forward strategic sourcing practices and supplier collaboration frameworks that Philips had built over the prior decade.

The Cooper Lighting acquisition in 2020 was a smart procurement move -- it broadened the supplier base, added North American manufacturing capacity, and partially offset the volume decline in legacy categories.

What Went Wrong

The 2021 supply chain crisis exposed Signify's vulnerability. Inside Philips, the lighting division could tap the parent's diversified supplier relationships across healthcare, consumer electronics, and industrial equipment. As a standalone company, Signify's procurement team had a narrower supplier network focused exclusively on lighting components. When semiconductor shortages hit, Signify couldn't reroute demand through sister-division supplier relationships the way it could have as a Philips subsidiary.

More fundamentally, Signify's cost base was built for €7 billion in revenue. As revenue declined toward €5.8 billion, fixed procurement overhead -- supplier management staff, quality systems, logistics infrastructure -- became proportionally more expensive. The sourcing bottleneck that large companies can absorb through headcount becomes acute when the organization is leaner.

The Recent Wave: What Other Spinoffs Teach Us

Signify isn't an isolated case. The 2022-2026 wave of industrial spinoffs has generated a dataset of procurement separation experiences.

GE's Three-Way Split (2023-2024)

GE's separation into GE HealthCare (January 2023), GE Vernova (April 2024), and GE Aerospace is the most complex industrial spinoff in recent history. PwC, which advised on the deal, documented the scale of the procurement separation:

200,000+ supplier documents collected and reviewed

7,000 contracts analyzed using AI and analytics tools to identify clauses requiring renegotiation

48 ERP systems separated across the three entities

40,000+ execution actions across workstreams covering regulatory compliance, supplier relationships, IT infrastructure, and financial implications

The GE case demonstrates that procurement separation is fundamentally a data and contract problem. Every supplier agreement needs to be read, categorized, and assigned to the right entity. Every BOM needs to be mapped to the correct procurement organization. Every IT system integration needs to be severed or replicated. At GE's scale, this required AI tooling that most separations don't invest in.

3M / Solventum (April 2024)

3M's separation of its healthcare business into Solventum included an explicit SEC filing disclosure about procurement risk: "As part of 3M, Solventum currently takes advantage of 3M's size and purchasing power in procuring certain goods and services. After the separation, each of 3M and Solventum may be unable to obtain these goods, services and technologies at prices or on terms as favorable as those 3M obtained prior to completion of the separation."

That's the parent company telling shareholders, in a regulatory filing, that the spun-off entity will pay more for the same inputs. It's the clearest articulation of the procurement penalty that spinoffs face.

Solventum's filings also note that functions previously provided by 3M -- accounting, legal, HR, and critically procurement -- would need to be replicated at standalone scale. "Because of Solventum's smaller scale as a standalone company, its cost of performing such functions could be higher than the amounts reflected in Solventum's historical financial statements."

Honeywell / Solstice Advanced Materials (October 2025)

Honeywell's separation is still in progress. Solstice Advanced Materials began trading in October 2025, and the remaining Automation and Aerospace businesses are expected to separate by Q3 2026. This three-way split mirrors GE's playbook but with one important difference: Honeywell has explicitly positioned each entity as a "pure-play" market leader with dedicated go-to-market and supply chain infrastructure from day one.

The procurement challenge for Solstice is particularly acute because specialty chemicals procurement depends heavily on long-term supply agreements and sole-source relationships. When you're Honeywell, you can negotiate raw material contracts across your entire $37 billion portfolio. When you're Solstice, you're a $4 billion specialty chemicals company negotiating alone.

Danaher / Veralto (September 2023) and BorgWarner / PHINIA (July 2023)

Both completed in 2023, these separations followed the same pattern: the parent retained the higher-growth, higher-margin business while spinning off the more mature unit. Veralto (water quality and product identification) separated from Danaher's life sciences focus. PHINIA (fuel systems and aftermarket) separated from BorgWarner's electrification strategy.

In both cases, the spun-off entity faced the classic procurement challenge: the categories they buy are the same, but their leverage is smaller. A fuel systems company negotiating steel contracts carries less weight than a $14 billion powertrain conglomerate.

The Five Procurement Problems Every Spinoff Faces

Across these cases, five challenges emerge consistently.

1. Volume Leverage Evaporates

The most immediate and measurable impact. A procurement organization that negotiated as part of a $30 billion parent is now negotiating as a $5 billion standalone. Supplier pricing is volume-dependent. The same commodity, the same supplier, the same quality spec -- but the price goes up because the volume went down.

This isn't theoretical. 3M explicitly disclosed the risk in Solventum's SEC filing. Signify experienced it as revenue declined below the cost base built at separation. Every spun-off entity in the 2022-2026 wave has faced some version of this math.

2. Transition Services Agreements Create a False Sense of Security

Most spinoffs include a Transition Services Agreement (TSA) -- a temporary arrangement where the parent continues to provide certain services (IT, HR, procurement support) for 12-24 months after separation. TSAs keep the lights on during the transition, but they mask the true standalone cost.

When the TSA expires, the spun-off company must either replicate those services internally or find new providers. Procurement teams that don't begin building independent capabilities during the TSA period -- while they still have the parent's systems and support -- find themselves scrambling when the agreement ends.

3. Supplier Relationships Don't Automatically Transfer

A supplier's relationship is with the buyer they know, not with the corporate entity on the contract. When the parent's procurement VP had a 15-year relationship with a key material supplier, that relationship belonged to a person, not to a legal entity. After a spinoff, the spun-off company may have the contract but not the relationship -- and in procurement, the relationship determines whether you get the call when capacity is tight.

This is where supplier relationship management becomes critical. The spun-off entity needs to invest in rebuilding trust, demonstrating reliability, and proving that it's a customer worth prioritizing -- without the parent's brand behind it.

4. ERP and Data Systems Fracture

GE's separation required splitting 48 ERP systems. That's not a typo. Enterprise procurement systems are deeply integrated with the parent's financial, logistics, and quality infrastructure. Separating them means either:

Replicating the parent's systems at standalone scale (expensive, time-consuming)

Implementing new systems from scratch (risky, even more time-consuming)

Running on temporary workarounds that degrade data quality and spend visibility

The procurement team that can't see its own spend data can't negotiate effectively. The team running on spreadsheet workarounds while the new ERP is being implemented is losing money every day it operates blind.

5. Talent Follows the Glamour

In most spinoffs, the parent retains the business perceived as higher-growth or more strategically exciting. The spun-off entity often gets the "mature" business label. Procurement talent -- especially senior strategic sourcing leaders -- tends to follow the glamour. The spun-off company may retain the operational buyers but lose the strategic thinkers who built the category strategies, the supplier development programs, and the should-cost models that drove savings.

Practical Steps: Maintaining Supplier Credibility Without the Mothership

For procurement leaders navigating a spinoff -- whether you're on the parent side or the separated entity -- here are the moves that matter.

Before Separation (T-minus 12 to 0 Months)

1. Audit every supplier contract for assignment clauses. Many supplier agreements contain change-of-control provisions that allow the supplier to renegotiate or terminate upon a corporate event. Identify these before the separation closes, not after. GE's approach -- AI-assisted review of 7,000 contracts -- is the right model if scale demands it.

2. Build your own supplier scorecards. Don't wait until the TSA expires to understand your supplier performance independently. Start collecting delivery, quality, and responsiveness data in your own systems during the transition period.

3. Identify the 20 suppliers that matter most. In most procurement organizations, 15-20 suppliers account for 60-70% of spend. Have your CPO personally visit these suppliers, explain the separation, and make the case for why the standalone entity is a customer worth investing in. This is relationship work that can't be delegated to the contract.

During Transition (T-0 to T+18 Months)

4. Compete what you couldn't before. Ironically, a spinoff can create procurement opportunities. Categories that were locked into enterprise-wide parent contracts may now be open for competitive bidding. The parent's preferred supplier was preferred for reasons that may not apply to the standalone entity. Run competitive sourcing events on categories that haven't been market-tested in years.

5. Invest in procurement technology early. The TSA provides temporary access to the parent's systems. When that access ends, you need your own. Companies that implement their own sourcing platform during the transition -- rather than after the TSA expires -- avoid the data gap that makes the first standalone year so painful.

This is where a platform like LightSource pays for itself fastest. A spun-off entity that can run structured RFQ events, benchmark pricing against historical data, and maintain supplier performance visibility from day one of independence starts its standalone life with the same operational capability as the parent -- without the parent's headcount or legacy systems.

6. Build consortiums or buying groups. If you've lost volume leverage, find it elsewhere. Industry buying cooperatives, group purchasing organizations, or informal alliances with non-competing companies in adjacent industries can partially restore the negotiating power that the parent's scale provided.

After Independence (T+18 Months and Beyond)

7. Requalify your supply base. The suppliers you inherited from the parent aren't necessarily the right suppliers for the standalone entity. Your volumes are different. Your specifications may be evolving. Your geographic footprint may be shifting. A systematic supplier qualification program -- starting with the top 50 suppliers and working down -- ensures your supply base fits your actual needs, not the parent's.

8. Tell your supplier story. Suppliers assess customer attractiveness based on volume, growth trajectory, payment reliability, and relationship quality. A freshly spun-off company may score lower on volume but can compete on the other three dimensions. Develop a clear narrative for your supply base: where the company is headed, why you're a growth customer (even if smaller), and what makes the relationship valuable beyond purchase orders.

9. Measure the procurement cost of independence. Track the specific cost increases attributable to the separation -- higher unit prices from lost volume, standalone IT costs, incremental headcount. This data is essential for making the business case for procurement investment. If standalone procurement costs $10 million more per year than the allocated cost under the parent, that's the baseline the procurement team needs to offset through savings initiatives.

The Spinoff Scorecard: What Separates Winners from Losers

Factor | Winners | Losers |

|---|---|---|

Contract prep | AI-assisted review before Day 1 (GE model) | Discover assignment clauses after separation |

Supplier relationships | CPO visits top 20 suppliers pre-separation | Assume contracts = relationships |

Technology | Own procurement platform during TSA period | Rely on parent systems until TSA expires |

Talent | Retain strategic sourcing leaders with equity | Let talent follow the "glamour" entity |

Volume strategy | Build buying consortiums; compete locked categories | Accept higher prices as inevitable |

Timeline awareness | 18-month capability buildout plan from Day 1 | React to each challenge as it arises |

Corporate spinoffs are accelerating. Honeywell's three-way split is still in progress. The industrial conglomerate model that defined the 20th century is being systematically dismantled. Every separation creates a procurement organization that must prove it can operate without the infrastructure, volume, and brand recognition of the parent.

The companies that manage this transition well are the ones that treat procurement independence as a strategic capability to be built, not an administrative consequence to be absorbed. They invest in their own systems, their own supplier relationships, and their own data -- before the TSA expires and the parent's support disappears.

The mothership is leaving. The question is whether you've built your own engine.

Sources

Signify Company History and Performance -- Revenue decline to €5.77B in 2025, 900 job cuts, margin erosion since spinoff

Signify Official Rebrand Announcement -- Philips Lighting to Signify rebrand, May 2018

PwC -- GE Split Case Study -- 200,000+ supplier documents, 7,000 contracts, 48 ERPs, 40,000+ execution actions

Honeywell -- Solstice Advanced Materials Spinoff -- Completed October 2025; Automation and Aerospace separation expected Q3 2026

Solventum SEC Filing (Form 10-12B) -- Explicit disclosure of lost purchasing power and standalone cost increases

Signify 2024 Full-Year Results -- €6.1B sales, 9.9% operational profitability, €334M net income

Bundl -- Corporate Spin-Off Examples -- Spinoff activity surged 33% from 2022; market trend analysis

Wikipedia -- List of Largest Corporate Spin-offs -- Historical context for industrial separations

Frequently Asked Questions

Why do corporate spinoffs create procurement problems?

Spinoffs separate a business unit from the parent company's purchasing scale, supplier relationships, IT infrastructure, and procurement talent. A division that negotiated as part of a $30 billion conglomerate must now negotiate as a $5 billion standalone. Supplier pricing is volume-dependent, so the same inputs often cost more post-separation. Transition Services Agreements provide temporary support but mask the true standalone cost until they expire.

How long does it take to build independent procurement after a spinoff?

Most companies need 18-24 months to achieve full procurement independence. The first 12 months are typically covered by a Transition Services Agreement with the parent. The critical window is months 6-18, when the procurement team should be building its own systems, renegotiating supplier contracts, and establishing independent performance tracking -- while still having access to the parent's support.

What happened to Signify after the Philips spinoff?

Signify (formerly Philips Lighting) went public in 2016 with €7 billion in revenue and 32,000 employees. It built independent procurement operations and acquired Cooper Lighting for $1.4 billion in 2020. However, the 2021 supply chain crisis cost an estimated €100 million in lost sales, exposing vulnerability without Philips' diversified supplier network. By 2025, revenue had declined to €5.77 billion and the company announced 900 additional job cuts. Signify remains profitable but operates at a lower scale than its initial separation.

How can a spun-off company maintain supplier credibility without the parent's volume?

Three approaches work: (1) Compete categories that were previously locked into parent-wide contracts -- you may find better pricing than the parent's preferred suppliers offered. (2) Build buying consortiums or group purchasing arrangements with non-competing companies to partially restore volume leverage. (3) Invest in the relationship dimensions that suppliers value beyond volume: payment reliability, growth trajectory, and the quality of the buyer-supplier working relationship.

What is a Transition Services Agreement and why does it matter?

A TSA is a temporary arrangement where the parent company continues providing services (IT, procurement systems, HR) to the spun-off entity for 12-24 months after separation. TSAs are essential for operational continuity but create a false sense of security. Procurement teams that don't build independent capabilities during the TSA period face a cliff when it expires -- sudden loss of system access, spend visibility, and operational support.

Which recent spinoffs offer the best procurement lessons?

GE's three-way split is the gold standard for procurement separation at scale -- 200,000 supplier documents reviewed, AI-assisted contract analysis, and 48 ERP systems separated. 3M/Solventum's SEC filings provide the most transparent disclosure of procurement risk. Signify's decade of post-spinoff experience shows the long-term trajectory. Honeywell's ongoing separation (Solstice completed, Automation and Aerospace in 2026) will provide the next major dataset.

In October 2025, Honeywell completed the spinoff of its Advanced Materials business into a new company called Solstice. Six months earlier, 3M had separated its healthcare unit into Solventum. A year before that, GE finished its three-way split into GE Aerospace, GE Vernova, and GE HealthCare -- a separation that required reviewing 200,000 supplier documents and using AI to parse 7,000 contracts. Danaher spun off Veralto. BorgWarner separated PHINIA. Corporate spinoff activity surged 33% starting in 2022 and hasn't slowed.

Every one of these separations created a procurement organization that woke up one morning with fewer suppliers under contract, less purchasing volume to negotiate with, and an ERP system that used to talk to the parent's but no longer does. The strategic rationale for spinoffs is well understood -- focus, agility, market-specific capital allocation. The procurement implications are far less discussed, and they're where the real operational pain lives.

This post uses the Philips/Signify separation as a primary case study, draws on the recent wave of industrial spinoffs for patterns, and offers practical guidance for procurement leaders navigating the transition from division to standalone company.

The Signify Story: From Philips Division to Standalone Company

The timeline is instructive.

2014: Philips announces it will split into two companies -- one focused on health technology, the other on connected LED lighting.

May 2016: Philips Lighting goes public on Euronext Amsterdam with an IPO valued at $3.4 billion. At separation, the business has €7 billion in revenue, 32,000 employees, and operations in more than 70 countries.

May 2018: Philips Lighting rebrands to Signify. The Philips brand continues to appear on products under a licensing agreement.

2020: Signify acquires Cooper Lighting Solutions from Eaton for $1.4 billion, expanding its North American market presence and diversifying its supplier base.

2021: Global supply chain disruptions hit Signify hard. The company reports an estimated €100 million in lost sales over a few months due to inability to source enough components -- particularly semiconductors. Without Philips' diversified supply network to fall back on, Signify struggles to requalify alternate suppliers quickly.

2023-2025: Revenue declines. Signify closes 2025 at €5.77 billion -- its lowest annual revenue since the 2016 spinoff. The company announces 900 additional job cuts. Adjusted EBITA margin falls to 8.9%.

The Signify trajectory isn't a simple decline story -- the company has maintained profitability, invested in connected lighting and IoT, and built a standalone procurement operation that functions independently. But it illustrates the core challenge: a spinoff inherits the parent's cost structure without the parent's scale. Over time, the gap between the two becomes the defining operational problem.

What Went Right

Signify started life as the world's largest lighting company. That initial scale gave it negotiating leverage with suppliers even after leaving Philips. Management ensured continuity by assigning or replicating existing Philips supplier contracts for day-one operations. The procurement team carried forward strategic sourcing practices and supplier collaboration frameworks that Philips had built over the prior decade.

The Cooper Lighting acquisition in 2020 was a smart procurement move -- it broadened the supplier base, added North American manufacturing capacity, and partially offset the volume decline in legacy categories.

What Went Wrong

The 2021 supply chain crisis exposed Signify's vulnerability. Inside Philips, the lighting division could tap the parent's diversified supplier relationships across healthcare, consumer electronics, and industrial equipment. As a standalone company, Signify's procurement team had a narrower supplier network focused exclusively on lighting components. When semiconductor shortages hit, Signify couldn't reroute demand through sister-division supplier relationships the way it could have as a Philips subsidiary.

More fundamentally, Signify's cost base was built for €7 billion in revenue. As revenue declined toward €5.8 billion, fixed procurement overhead -- supplier management staff, quality systems, logistics infrastructure -- became proportionally more expensive. The sourcing bottleneck that large companies can absorb through headcount becomes acute when the organization is leaner.

The Recent Wave: What Other Spinoffs Teach Us

Signify isn't an isolated case. The 2022-2026 wave of industrial spinoffs has generated a dataset of procurement separation experiences.

GE's Three-Way Split (2023-2024)

GE's separation into GE HealthCare (January 2023), GE Vernova (April 2024), and GE Aerospace is the most complex industrial spinoff in recent history. PwC, which advised on the deal, documented the scale of the procurement separation:

200,000+ supplier documents collected and reviewed

7,000 contracts analyzed using AI and analytics tools to identify clauses requiring renegotiation

48 ERP systems separated across the three entities

40,000+ execution actions across workstreams covering regulatory compliance, supplier relationships, IT infrastructure, and financial implications

The GE case demonstrates that procurement separation is fundamentally a data and contract problem. Every supplier agreement needs to be read, categorized, and assigned to the right entity. Every BOM needs to be mapped to the correct procurement organization. Every IT system integration needs to be severed or replicated. At GE's scale, this required AI tooling that most separations don't invest in.

3M / Solventum (April 2024)

3M's separation of its healthcare business into Solventum included an explicit SEC filing disclosure about procurement risk: "As part of 3M, Solventum currently takes advantage of 3M's size and purchasing power in procuring certain goods and services. After the separation, each of 3M and Solventum may be unable to obtain these goods, services and technologies at prices or on terms as favorable as those 3M obtained prior to completion of the separation."

That's the parent company telling shareholders, in a regulatory filing, that the spun-off entity will pay more for the same inputs. It's the clearest articulation of the procurement penalty that spinoffs face.

Solventum's filings also note that functions previously provided by 3M -- accounting, legal, HR, and critically procurement -- would need to be replicated at standalone scale. "Because of Solventum's smaller scale as a standalone company, its cost of performing such functions could be higher than the amounts reflected in Solventum's historical financial statements."

Honeywell / Solstice Advanced Materials (October 2025)

Honeywell's separation is still in progress. Solstice Advanced Materials began trading in October 2025, and the remaining Automation and Aerospace businesses are expected to separate by Q3 2026. This three-way split mirrors GE's playbook but with one important difference: Honeywell has explicitly positioned each entity as a "pure-play" market leader with dedicated go-to-market and supply chain infrastructure from day one.

The procurement challenge for Solstice is particularly acute because specialty chemicals procurement depends heavily on long-term supply agreements and sole-source relationships. When you're Honeywell, you can negotiate raw material contracts across your entire $37 billion portfolio. When you're Solstice, you're a $4 billion specialty chemicals company negotiating alone.

Danaher / Veralto (September 2023) and BorgWarner / PHINIA (July 2023)

Both completed in 2023, these separations followed the same pattern: the parent retained the higher-growth, higher-margin business while spinning off the more mature unit. Veralto (water quality and product identification) separated from Danaher's life sciences focus. PHINIA (fuel systems and aftermarket) separated from BorgWarner's electrification strategy.

In both cases, the spun-off entity faced the classic procurement challenge: the categories they buy are the same, but their leverage is smaller. A fuel systems company negotiating steel contracts carries less weight than a $14 billion powertrain conglomerate.

The Five Procurement Problems Every Spinoff Faces

Across these cases, five challenges emerge consistently.

1. Volume Leverage Evaporates

The most immediate and measurable impact. A procurement organization that negotiated as part of a $30 billion parent is now negotiating as a $5 billion standalone. Supplier pricing is volume-dependent. The same commodity, the same supplier, the same quality spec -- but the price goes up because the volume went down.

This isn't theoretical. 3M explicitly disclosed the risk in Solventum's SEC filing. Signify experienced it as revenue declined below the cost base built at separation. Every spun-off entity in the 2022-2026 wave has faced some version of this math.

2. Transition Services Agreements Create a False Sense of Security

Most spinoffs include a Transition Services Agreement (TSA) -- a temporary arrangement where the parent continues to provide certain services (IT, HR, procurement support) for 12-24 months after separation. TSAs keep the lights on during the transition, but they mask the true standalone cost.

When the TSA expires, the spun-off company must either replicate those services internally or find new providers. Procurement teams that don't begin building independent capabilities during the TSA period -- while they still have the parent's systems and support -- find themselves scrambling when the agreement ends.

3. Supplier Relationships Don't Automatically Transfer

A supplier's relationship is with the buyer they know, not with the corporate entity on the contract. When the parent's procurement VP had a 15-year relationship with a key material supplier, that relationship belonged to a person, not to a legal entity. After a spinoff, the spun-off company may have the contract but not the relationship -- and in procurement, the relationship determines whether you get the call when capacity is tight.

This is where supplier relationship management becomes critical. The spun-off entity needs to invest in rebuilding trust, demonstrating reliability, and proving that it's a customer worth prioritizing -- without the parent's brand behind it.

4. ERP and Data Systems Fracture

GE's separation required splitting 48 ERP systems. That's not a typo. Enterprise procurement systems are deeply integrated with the parent's financial, logistics, and quality infrastructure. Separating them means either:

Replicating the parent's systems at standalone scale (expensive, time-consuming)

Implementing new systems from scratch (risky, even more time-consuming)

Running on temporary workarounds that degrade data quality and spend visibility

The procurement team that can't see its own spend data can't negotiate effectively. The team running on spreadsheet workarounds while the new ERP is being implemented is losing money every day it operates blind.

5. Talent Follows the Glamour

In most spinoffs, the parent retains the business perceived as higher-growth or more strategically exciting. The spun-off entity often gets the "mature" business label. Procurement talent -- especially senior strategic sourcing leaders -- tends to follow the glamour. The spun-off company may retain the operational buyers but lose the strategic thinkers who built the category strategies, the supplier development programs, and the should-cost models that drove savings.

Practical Steps: Maintaining Supplier Credibility Without the Mothership

For procurement leaders navigating a spinoff -- whether you're on the parent side or the separated entity -- here are the moves that matter.

Before Separation (T-minus 12 to 0 Months)

1. Audit every supplier contract for assignment clauses. Many supplier agreements contain change-of-control provisions that allow the supplier to renegotiate or terminate upon a corporate event. Identify these before the separation closes, not after. GE's approach -- AI-assisted review of 7,000 contracts -- is the right model if scale demands it.

2. Build your own supplier scorecards. Don't wait until the TSA expires to understand your supplier performance independently. Start collecting delivery, quality, and responsiveness data in your own systems during the transition period.

3. Identify the 20 suppliers that matter most. In most procurement organizations, 15-20 suppliers account for 60-70% of spend. Have your CPO personally visit these suppliers, explain the separation, and make the case for why the standalone entity is a customer worth investing in. This is relationship work that can't be delegated to the contract.

During Transition (T-0 to T+18 Months)

4. Compete what you couldn't before. Ironically, a spinoff can create procurement opportunities. Categories that were locked into enterprise-wide parent contracts may now be open for competitive bidding. The parent's preferred supplier was preferred for reasons that may not apply to the standalone entity. Run competitive sourcing events on categories that haven't been market-tested in years.

5. Invest in procurement technology early. The TSA provides temporary access to the parent's systems. When that access ends, you need your own. Companies that implement their own sourcing platform during the transition -- rather than after the TSA expires -- avoid the data gap that makes the first standalone year so painful.

This is where a platform like LightSource pays for itself fastest. A spun-off entity that can run structured RFQ events, benchmark pricing against historical data, and maintain supplier performance visibility from day one of independence starts its standalone life with the same operational capability as the parent -- without the parent's headcount or legacy systems.

6. Build consortiums or buying groups. If you've lost volume leverage, find it elsewhere. Industry buying cooperatives, group purchasing organizations, or informal alliances with non-competing companies in adjacent industries can partially restore the negotiating power that the parent's scale provided.

After Independence (T+18 Months and Beyond)

7. Requalify your supply base. The suppliers you inherited from the parent aren't necessarily the right suppliers for the standalone entity. Your volumes are different. Your specifications may be evolving. Your geographic footprint may be shifting. A systematic supplier qualification program -- starting with the top 50 suppliers and working down -- ensures your supply base fits your actual needs, not the parent's.

8. Tell your supplier story. Suppliers assess customer attractiveness based on volume, growth trajectory, payment reliability, and relationship quality. A freshly spun-off company may score lower on volume but can compete on the other three dimensions. Develop a clear narrative for your supply base: where the company is headed, why you're a growth customer (even if smaller), and what makes the relationship valuable beyond purchase orders.

9. Measure the procurement cost of independence. Track the specific cost increases attributable to the separation -- higher unit prices from lost volume, standalone IT costs, incremental headcount. This data is essential for making the business case for procurement investment. If standalone procurement costs $10 million more per year than the allocated cost under the parent, that's the baseline the procurement team needs to offset through savings initiatives.

The Spinoff Scorecard: What Separates Winners from Losers

Factor | Winners | Losers |

|---|---|---|

Contract prep | AI-assisted review before Day 1 (GE model) | Discover assignment clauses after separation |

Supplier relationships | CPO visits top 20 suppliers pre-separation | Assume contracts = relationships |

Technology | Own procurement platform during TSA period | Rely on parent systems until TSA expires |

Talent | Retain strategic sourcing leaders with equity | Let talent follow the "glamour" entity |

Volume strategy | Build buying consortiums; compete locked categories | Accept higher prices as inevitable |

Timeline awareness | 18-month capability buildout plan from Day 1 | React to each challenge as it arises |

Corporate spinoffs are accelerating. Honeywell's three-way split is still in progress. The industrial conglomerate model that defined the 20th century is being systematically dismantled. Every separation creates a procurement organization that must prove it can operate without the infrastructure, volume, and brand recognition of the parent.

The companies that manage this transition well are the ones that treat procurement independence as a strategic capability to be built, not an administrative consequence to be absorbed. They invest in their own systems, their own supplier relationships, and their own data -- before the TSA expires and the parent's support disappears.

The mothership is leaving. The question is whether you've built your own engine.

Sources

Signify Company History and Performance -- Revenue decline to €5.77B in 2025, 900 job cuts, margin erosion since spinoff

Signify Official Rebrand Announcement -- Philips Lighting to Signify rebrand, May 2018

PwC -- GE Split Case Study -- 200,000+ supplier documents, 7,000 contracts, 48 ERPs, 40,000+ execution actions

Honeywell -- Solstice Advanced Materials Spinoff -- Completed October 2025; Automation and Aerospace separation expected Q3 2026

Solventum SEC Filing (Form 10-12B) -- Explicit disclosure of lost purchasing power and standalone cost increases

Signify 2024 Full-Year Results -- €6.1B sales, 9.9% operational profitability, €334M net income

Bundl -- Corporate Spin-Off Examples -- Spinoff activity surged 33% from 2022; market trend analysis

Wikipedia -- List of Largest Corporate Spin-offs -- Historical context for industrial separations

Frequently Asked Questions

Why do corporate spinoffs create procurement problems?

Spinoffs separate a business unit from the parent company's purchasing scale, supplier relationships, IT infrastructure, and procurement talent. A division that negotiated as part of a $30 billion conglomerate must now negotiate as a $5 billion standalone. Supplier pricing is volume-dependent, so the same inputs often cost more post-separation. Transition Services Agreements provide temporary support but mask the true standalone cost until they expire.

How long does it take to build independent procurement after a spinoff?

Most companies need 18-24 months to achieve full procurement independence. The first 12 months are typically covered by a Transition Services Agreement with the parent. The critical window is months 6-18, when the procurement team should be building its own systems, renegotiating supplier contracts, and establishing independent performance tracking -- while still having access to the parent's support.

What happened to Signify after the Philips spinoff?

Signify (formerly Philips Lighting) went public in 2016 with €7 billion in revenue and 32,000 employees. It built independent procurement operations and acquired Cooper Lighting for $1.4 billion in 2020. However, the 2021 supply chain crisis cost an estimated €100 million in lost sales, exposing vulnerability without Philips' diversified supplier network. By 2025, revenue had declined to €5.77 billion and the company announced 900 additional job cuts. Signify remains profitable but operates at a lower scale than its initial separation.

How can a spun-off company maintain supplier credibility without the parent's volume?

Three approaches work: (1) Compete categories that were previously locked into parent-wide contracts -- you may find better pricing than the parent's preferred suppliers offered. (2) Build buying consortiums or group purchasing arrangements with non-competing companies to partially restore volume leverage. (3) Invest in the relationship dimensions that suppliers value beyond volume: payment reliability, growth trajectory, and the quality of the buyer-supplier working relationship.

What is a Transition Services Agreement and why does it matter?

A TSA is a temporary arrangement where the parent company continues providing services (IT, procurement systems, HR) to the spun-off entity for 12-24 months after separation. TSAs are essential for operational continuity but create a false sense of security. Procurement teams that don't build independent capabilities during the TSA period face a cliff when it expires -- sudden loss of system access, spend visibility, and operational support.

Which recent spinoffs offer the best procurement lessons?

GE's three-way split is the gold standard for procurement separation at scale -- 200,000 supplier documents reviewed, AI-assisted contract analysis, and 48 ERP systems separated. 3M/Solventum's SEC filings provide the most transparent disclosure of procurement risk. Signify's decade of post-spinoff experience shows the long-term trajectory. Honeywell's ongoing separation (Solstice completed, Automation and Aerospace in 2026) will provide the next major dataset.

Read more

Source Code Episode 9: Source Code: Shashi Mandapaty, Former Chief Procurement Officer at Johnson & Johnson, on Why One Throne Isn't Enough

Source Code Episode 8: Running on Paper: Rick McDonald, Chief Supply Chain Officer at Clorox, on Why Supplier Trust Is the Real Business Continuity Plan

The IEEPA Ruling Wasn't a Win. Here's What Procurement Leaders Are Missing.

Read more

Source Code Episode 9: Source Code: Shashi Mandapaty, Former Chief Procurement Officer at Johnson & Johnson, on Why One Throne Isn't Enough

Source Code Episode 8: Running on Paper: Rick McDonald, Chief Supply Chain Officer at Clorox, on Why Supplier Trust Is the Real Business Continuity Plan

The IEEPA Ruling Wasn't a Win. Here's What Procurement Leaders Are Missing.

Read more

Source Code Episode 9: Source Code: Shashi Mandapaty, Former Chief Procurement Officer at Johnson & Johnson, on Why One Throne Isn't Enough

Source Code Episode 8: Running on Paper: Rick McDonald, Chief Supply Chain Officer at Clorox, on Why Supplier Trust Is the Real Business Continuity Plan

The IEEPA Ruling Wasn't a Win. Here's What Procurement Leaders Are Missing.

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Trusted by:

Trusted by:

Trusted by:

*GARTNER is a registered trademark and service mark of Gartner, Inc. and/or its affiliates in the U.S. and internationally, and COOL VENDORS is a registered trademark of Gartner, Inc. and/or its affiliates and are used herein with permission. All rights reserved. Gartner does not endorse any vendor, product or service depicted in its research publications, and does not advise technology users to select only those vendors with the highest ratings or other designation. Gartner research publications consist of the opinions of Gartner’s research organization and should not be construed as statements of fact. Gartner disclaims all warranties, expressed or implied, with respect to this research, including any warranties of merchantability or fitness for a particular purpose.