The single most important machine in the world economy is also one of the hardest to ship. When ASML sends an extreme-ultraviolet lithography system to a customer, it goes out as roughly 40 freight containers, three cargo planes, and 20 trucks, then gets reassembled in a cleanroom the size of a swimming pool. The machine has about 100,000 parts. ASML does not make most of them. The company describes itself as an "architect and integrator," and says it sources around 80% of its bill of materials from a network of about 5,100 suppliers. On Dwarkesh Patel's podcast in March, Dylan Patel of SemiAnalysis put the human scale of it plainly: ASML has said its supply chain involves "over ten thousand people." He called the result "the world's most complicated machine."

That dispersion is the whole story, and it cuts two ways. It is why no one has been able to copy ASML in forty years of trying, and it is also why ASML can build only about 70 of these machines a year. The same global supply chain that makes the EUV tool possible is the thing that caps how many can exist. And it is the backdrop for the most expensive industrial project on earth right now: China's attempt to rebuild the entire chipmaking-equipment supply chain inside one country, because export controls have left it no other option.

I want to map both chains, because the contrast is more useful than the headline. One is a story about specialization spread across the planet. The other is a story about a single nation trying to internalize all of it at once. Most companies will never operate at this scale, but the tradeoff underneath is the same one any manufacturer faces about its own critical suppliers: do you optimize for the best possible product, or for control of the supply that builds it?

Map A: ASML, or specialization spread across a planet

ASML's supply chain is not a pyramid with ASML on top. It is closer to a constellation of specialists, each of which is the best or only source for one impossibly hard thing, with ASML in the Netherlands integrating them into a working tool. The supplier base breaks down to roughly 1,600 in the Netherlands, 700 elsewhere in Europe, 1,350 in North America, and 1,450 in Asia. The critical few matter far more than the count.

Subsystem | Supplier / site | What it contributes | Why it's a chokepoint |

|---|---|---|---|

Optics | Carl Zeiss SMT -- Oberkochen, Germany | EUV mirrors (not lenses) with 100+ engineered layers, polished to below the thickness of a single atom | ASML's optics have come from Zeiss since the 1980s; ASML took a 24.9% stake in Zeiss SMT in 2016 to lock the relationship in |

Light source | Cymer / ASML -- San Diego, USA | Laser-produced-plasma source: tin droplets hit by laser pulses ~60,000 times a second to emit 13.5 nm light | The light source gated EUV for years; ASML bought Cymer in 2013 to control it |

Drive laser | TRUMPF -- Ditzingen, Germany | The high-power CO2 laser that vaporizes the tin droplets | Co-developed with ASML and Zeiss; no commodity substitute |

Precision stages | ASML and specialist suppliers (Connecticut, per Patel; Europe) | Reticle and wafer stages that move in opposite directions with sub-nanometer overlay | Systems-level precision, not commodity mechanics |

Module supply | VDL and other Dutch high-tech firms | Vacuum vessels and mechatronic modules | A deep, co-developed Dutch supplier base built over decades |

Integration | ASML -- Veldhoven, Netherlands | Architecture, assembly, qualification, teardown, shipment, on-site rebuild | The tacit knowledge of making 100,000 parts work as one machine |

The pattern is the point. Each row is a near-monopoly held by one company in one place, and several of them sit inside ASML through ownership or decades of joint development. Zeiss does not sell its EUV optics to anyone else. Cymer is ASML. The drive laser comes from one firm in one German town. This is what makes the machine impossible to clone on a deadline: the hard part was never a blueprint you could steal. It is twenty-five years of co-developed process knowledge spread across optics, plasma physics, precision motion, metrology, and software, none of which is written down in one place. The EUV source alone has to fire a laser at tin droplets up to 100,000 times a second, in a vacuum, reliably enough to run inside a customer's fab. That is exotic physics and a production tool at the same time.

Why the global chain is also a ceiling

Here is the part worth dwelling on, because it is the one most coverage skips. The same distributed specialization that protects ASML also limits how fast it can grow. ASML shipped 48 EUV systems in 2025. Patel estimates the company can make about 70 a year now, 80 next year, and a little over 100 a year by the end of the decade even with aggressive expansion, at roughly $300 to $400 million per tool. He calls scaling EUV "production hell."

The reason is that you cannot scale an integrator faster than its scarcest supplier. Adding final-assembly capacity in Veldhoven does nothing unless Zeiss's mirror-coating capacity, Cymer's source capacity, TRUMPF's laser output, the stage builders, the supplier quality teams, the field engineers, and the spare-parts pipeline all move together. Each of those is its own artisanal, low-volume operation. As Patel describes the components, "you're not making tens of thousands of these a year, you're making hundreds, you're making thousands," and "any defect in these super thinly deposited stacks will mess it up." A single-source bottleneck is a wonderful thing when it blocks your competitors. It is a painful thing when your customers want another hundred tools and the one company that can polish the mirrors is already running flat out.

That ceiling is becoming everyone's problem. Patel argues that by 2028 or 2029, the binding constraint on AI compute moves down the stack to ASML, because leading-edge wafer output is gated by how many EUV tools exist. I recently wrote about how Google ended up renting its scarcest compute to a competitor; a few layers below that fight, the real scarcity is a few dozen machines a year from one Dutch company that depends on one German optics maker.

Map B: China, or one country trying to internalize all of it

China is attempting the opposite model, not by choice but by denial. Cut off from EUV since 2019 and from advanced deep-ultraviolet tools since 2023, it is building a parallel equipment supply chain inside its own borders, with SMIC and Huawei as the anchor customers and a roster of national champions filling each tool category. The progress is real, and it is wildly uneven.

Tool category | Chinese players | Status | Domestic share |

|---|---|---|---|

Etch | AMEC | Verifying 14 nm etch at SMIC; a 5 nm etch tool in validation at TSMC | Etch + deposition >40% |

Deposition / thermal | Naura | Mass-producing 28 nm tools; its furnaces are >60% of equipment on SMIC's 28 nm lines | (largest domestic maker) |

Thin-film (PECVD) | Piotech | Roughly doubled its share at YMTC's 3D NAND lines | included above |

Clean | ACM Research | Single-wafer cleaning tools at Hua Hong running above 90% utilization | high |

Track, CMP | Kingsemi, Hwatsing | Coat/develop tracks and chemical-mechanical polishing | moderate |

Lithography | SMEE; Yuliangsheng (SiCarrier-linked) | SMEE's 28 nm immersion in verification; SMIC testing a domestic immersion DUV tool, mostly Chinese-made but still using some imported parts | Lithography ~18% |

Metrology, EDA | SiCarrier subsidiaries and others | Domestic EDA and photoresist tools shown at trade shows | Metrology ~25%; EDA ~10% |

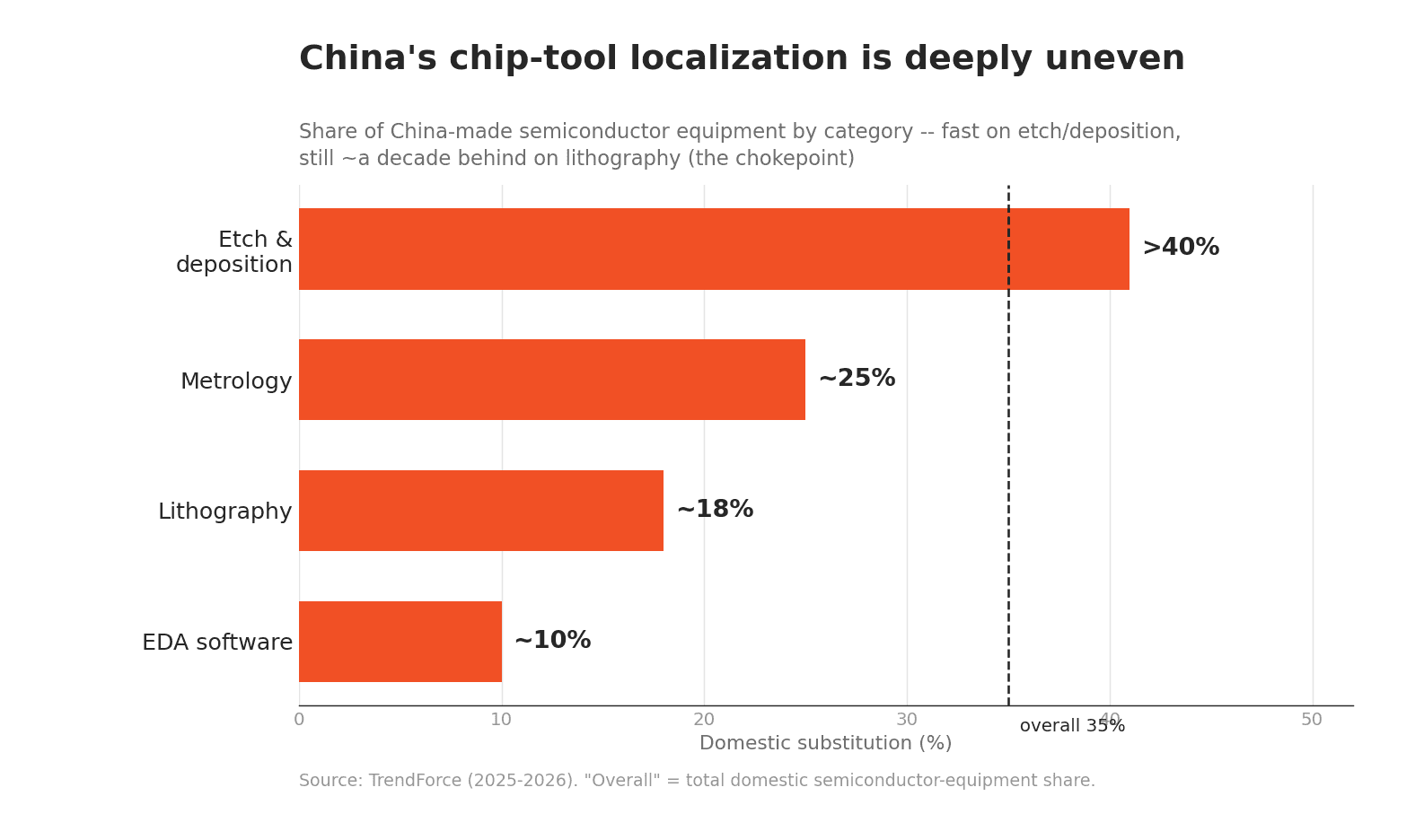

Read the right-hand column and the strategy snaps into focus. China is moving fastest exactly where the manufacturing problem is hard but modular: etch, deposition, thermal, cleaning, polishing. Those require deep process knowledge, but not a Zeiss-class mirror train or an EUV source firing plasma tens of thousands of times a second. Domestic substitution in etch and thin-film deposition is already above 40%, and overall domestic equipment share rose from 25% in 2024 to 35% in 2025. Naura booked more revenue in the first three quarters of 2025 than several times its entire 2020 take.

China remains farthest behind precisely where ASML's moat is deepest. Domestic substitution sits at roughly 18% for lithography, 25% for metrology, and barely above 10% for EDA software. Patel is blunt that the gap is still total at the frontier: "all of China's 7 nm and 14 nm capacity uses ASML DUV tools." A domestic 28 nm-class immersion DUV tool would matter a great deal, and with enough multi-patterning, DUV can be pushed toward more advanced nodes, though that route piles on masks, process steps, cycle time, and yield loss. It can be strategically useful even when it is economically ugly. There are reports of a Chinese EUV prototype assembled from components of older ASML systems, with a government target of chips by 2028 and 2030 seen as more realistic.

The distinction that matters is between a demonstration and a fleet. A tool that prints a wafer in a lab is a milestone. A fleet that holds uptime, overlay, throughput, service, spares, and yield steady across multiple fabs is a different industrial achievement, and it is the one China has not reached at the leading edge. Patel gives China credit and draws the line in the same breath: "I think they'll have working tools. I don't think that they'll be able to manufacture a bunch yet." His estimate is that China might reach about 100 DUV tools a year by 2030, against the hundreds ASML already ships.

The forcing function: export controls

None of China's localization push happens without the export controls that made it necessary, and the controls did something subtler than slow China down. They changed the procurement spec. A Chinese fab no longer just asks which tool performs best; it asks which tool it can still buy, service, and improve if foreign supply gets worse. That turns purchasing into industrial policy.

EUV has been blocked from China since 2019, and ASML says it has never shipped an EUV machine there. In 2023 and 2024 the Dutch and US governments extended controls into advanced immersion DUV, so ASML's most capable NXT:1970i and NXT:1980i tools now require Dutch export licenses. As of June 2026, a bipartisan US bill would go further and effectively ban all ASML DUV shipments to China, a category that is roughly a fifth of ASML's expected 2026 revenue.

The effect on ASML is that its largest growth market is turning into a political liability. China was about 29% of ASML's 2025 sales by one count and a third by another, and the company expects that to fall toward 20% in 2026. The effect on China is the multi-hundred-billion-yuan scramble now underway: Beijing has reportedly required new fab capacity to use more than 50% domestic equipment and discussed subsidies as large as 500 billion yuan. Controls did not slow China's equipment industry. They created its domestic market overnight.

Two philosophies of supply chain

Strip away the geopolitics and what is left are two genuinely different answers to the same question: do you optimize your supply chain for capability or for control?

Dimension | ASML model | China's domestic model |

|---|---|---|

Optimizing for | Maximum capability | Control under denial |

Structure | Specialized global suppliers, one integrator | State-backed localization across every tool category |

Core strength | Decades of tacit, co-developed knowledge | Fast demand pull from domestic fabs plus policy money |

Core weakness | Volume ceiling; political exposure across borders | Lower maturity in lithography, optics, metrology, EDA |

Hardest wall | Scaling artisanal suppliers without losing quality | Moving from working prototypes to production fleets |

ASML chose capability. By going to the single best supplier for every subsystem, wherever on earth it sits, it built a machine no one else can make. The cost is a chain that is volume-limited by its most artisanal link and politically exposed at every border it crosses. China is being forced to choose control. By rebuilding every tool category at home, it is trading the frontier for sovereignty, accepting tools a node or two behind in exchange for a chain no foreign government can switch off. Neither is wrong. They are different bets about which risk is more dangerous: not having the best tool, or not controlling the tool you have.

What is striking is that the deepest part of ASML's moat is the part China cannot buy its way around. You can fund an etch champion and reach 40% domestic share in a few years, because etch, while brutally hard, is a problem money and talent can attack in parallel. You cannot fund your way to a Zeiss, because the knowledge of how to polish a mirror to below an atom's thickness lives in a few hundred people and a few decades of failures, and it does not transfer on a five-year plan. My colleague Andy Hunt has written about why dual sourcing alone won't save your supply chain when every supposed alternative converges on the same sub-tier. ASML is the extreme version of that problem: at the very bottom of the world's most important supply chain sits one optics company with no real second source anywhere on the planet.

What this means for the rest of us

Most manufacturers are not building EUV machines, but almost every hardware company has its own version of the Zeiss problem: a single supplier, often several tiers down, that no one mapped until it became a crisis. A program can look comfortably dual-sourced at the tier-one level while both of those suppliers quietly depend on the same sub-tier coating, magnet, resin, or test socket. That is the trap multi-sourcing is supposed to prevent and often doesn't.

The lesson from ASML is not "go global" or "localize." It is that you cannot make either choice well if you cannot see your own supply chain to its roots, and the same make-versus-buy decision China is being forced to make at national scale shows up on every serious BOM. ASML knows its 5,100 suppliers and its critical chokepoints in granular detail; that visibility is part of why it can manage the risk at all. Most companies discover their tier-three dependency the week it stops shipping.

This is the gap LightSource is built to close for the companies we work with. The same speed-and-localization pressures playing out in semiconductors are reshaping ordinary automotive and electronics bills of materials too, and the compressed development cycles we examined in China Time only raise the stakes. A challenger manufacturer competing on speed cannot afford to learn where its single-source and long-lead exposures are only when one of them breaks. Connecting engineering, procurement, and suppliers in one system means a sole-source risk or a geographic concentration surfaces on the BOM while there is still time to qualify a second source or redesign around it. The operating question is the same whether you are ASML or a robotics startup: which supplier dependency will decide your ramp before the launch team even notices it is there?

China will likely close most of the mature-node equipment gap this decade, and may build DUV tools at real scale by 2030. The harder question is whether forced verticalization can ever reach the frontier that emergent global specialization built, or whether the optics wall holds for another decade. Either way, the contest is no longer just about who designs the best machine. It is about which kind of supply chain proves more durable: the one optimized to build the best possible tool, or the one optimized to never be cut off. We are about to find out which bet was right.

Sources

ASML 2025 Annual Report -- 5,100 suppliers and regional split, ~80% of BOM from suppliers, 2025 shipments (48 EUV, 279 DUV), €32.7B net sales.

ASML -- How we innovate -- ASML as "architect and integrator," supplier network, VDL example.

ASML -- Busting ASML myths -- ~100,000 parts; EUV ships as 40 containers, 3 cargo planes, 20 trucks.

ASML -- Lenses and mirrors -- Zeiss optics, EUV mirrors with 100+ layers polished below an atom's thickness.

ASML + Zeiss partnership (2016) -- ASML's 24.9% stake in Carl Zeiss SMT.

ASML -- Cymer -- San Diego light source; 2013 acquisition.

TRUMPF -- EUV lithography -- CO2 drive laser co-developed with ASML and Zeiss.

Dwarkesh Patel -- Dylan Patel -- "world's most complicated machine," "over ten thousand people," artisanal production, ~70-80 EUV/year, China DUV/EUV outlook.

TrendForce -- China domestic chip-equipment adoption hits 35% -- 25%->35% share; substitution by category (etch/deposition >40%, lithography 18%, metrology 25%); Naura, AMEC, Piotech, ACM.

TrendForce -- China chip-tool push, 70% target by 2027 -- SMEE 28 nm immersion in verification; EUV prototype reporting.

Tom's Hardware -- China's first domestic immersion DUV tool tested at SMIC -- domestic DUV, mostly Chinese-made, some imported parts.

ASML -- Dutch export license requirement (2024) -- NXT:1970i/1980i need Dutch licenses.

TechCrunch -- US bill targeting ASML DUV to China (June 2026) -- proposed DUV ban; DUV ~one-fifth of 2026 ASML revenue.

Caixin -- ASML expects China revenue to fall in 2026 -- China exposure falling toward ~20%.

Frequently Asked Questions

How many suppliers does ASML have, and why does it matter?

ASML reports about 5,100 suppliers, split roughly 1,600 in the Netherlands, 700 elsewhere in Europe, 1,350 in North America, and 1,450 in Asia, and it sources around 80% of an EUV machine's bill of materials from them. It matters because ASML is an integrator, not a vertically integrated manufacturer: its advantage is the global network of single-source specialists it has co-developed over decades, which is exactly what makes the machine impossible to copy quickly.

Why can ASML only build about 70 EUV machines a year?

Each machine has roughly 100,000 parts and depends on artisanal, single-source components like Carl Zeiss's EUV optics, which are polished to below the thickness of an atom. ASML can only scale as fast as its slowest critical supplier, because adding assembly capacity does nothing unless mirror, light-source, laser, and stage capacity all grow together. Dylan Patel estimates output at about 70 to 80 a year now, rising past 100 only by the end of the decade.

How close is China to replicating ASML's lithography machines?

China is closing the gap fast on etch, deposition, cleaning, and other non-lithography tools, where domestic substitution is above 40%, but it remains roughly a decade behind on lithography, where substitution is about 18% and there is no domestic EUV in volume production. SMEE's 28 nm immersion tool is in verification and a domestic DUV tool is being tested at SMIC, but as of 2026 all of China's 7 nm and 14 nm capacity still runs on ASML's deep-ultraviolet machines.

What are the export controls on ASML, and how is China responding?

EUV machines have been blocked from China since 2019, and advanced DUV tools since 2023-2024; a 2026 US bill proposes banning all ASML DUV shipments to China. In response, Beijing has reportedly mandated more than 50% domestic equipment for new fab capacity and discussed subsidies up to 500 billion yuan, which has turned export controls into the catalyst for China's domestic equipment industry.

What can an ordinary manufacturer learn from the ASML vs. China comparison?

The core lesson is that a supply chain optimized for the best possible product (ASML's global specialists) and one optimized for control (China's domestic chain) carry opposite risks: volume limits and political exposure versus being a step behind the frontier. Most companies have a hidden single-source dependency several tiers down, so the practical takeaway is to map your supply chain to its roots and decide, deliberately, whether to live with a chokepoint or invest in a real second source.

The single most important machine in the world economy is also one of the hardest to ship. When ASML sends an extreme-ultraviolet lithography system to a customer, it goes out as roughly 40 freight containers, three cargo planes, and 20 trucks, then gets reassembled in a cleanroom the size of a swimming pool. The machine has about 100,000 parts. ASML does not make most of them. The company describes itself as an "architect and integrator," and says it sources around 80% of its bill of materials from a network of about 5,100 suppliers. On Dwarkesh Patel's podcast in March, Dylan Patel of SemiAnalysis put the human scale of it plainly: ASML has said its supply chain involves "over ten thousand people." He called the result "the world's most complicated machine."

That dispersion is the whole story, and it cuts two ways. It is why no one has been able to copy ASML in forty years of trying, and it is also why ASML can build only about 70 of these machines a year. The same global supply chain that makes the EUV tool possible is the thing that caps how many can exist. And it is the backdrop for the most expensive industrial project on earth right now: China's attempt to rebuild the entire chipmaking-equipment supply chain inside one country, because export controls have left it no other option.

I want to map both chains, because the contrast is more useful than the headline. One is a story about specialization spread across the planet. The other is a story about a single nation trying to internalize all of it at once. Most companies will never operate at this scale, but the tradeoff underneath is the same one any manufacturer faces about its own critical suppliers: do you optimize for the best possible product, or for control of the supply that builds it?

Map A: ASML, or specialization spread across a planet

ASML's supply chain is not a pyramid with ASML on top. It is closer to a constellation of specialists, each of which is the best or only source for one impossibly hard thing, with ASML in the Netherlands integrating them into a working tool. The supplier base breaks down to roughly 1,600 in the Netherlands, 700 elsewhere in Europe, 1,350 in North America, and 1,450 in Asia. The critical few matter far more than the count.

Subsystem | Supplier / site | What it contributes | Why it's a chokepoint |

|---|---|---|---|

Optics | Carl Zeiss SMT -- Oberkochen, Germany | EUV mirrors (not lenses) with 100+ engineered layers, polished to below the thickness of a single atom | ASML's optics have come from Zeiss since the 1980s; ASML took a 24.9% stake in Zeiss SMT in 2016 to lock the relationship in |

Light source | Cymer / ASML -- San Diego, USA | Laser-produced-plasma source: tin droplets hit by laser pulses ~60,000 times a second to emit 13.5 nm light | The light source gated EUV for years; ASML bought Cymer in 2013 to control it |

Drive laser | TRUMPF -- Ditzingen, Germany | The high-power CO2 laser that vaporizes the tin droplets | Co-developed with ASML and Zeiss; no commodity substitute |

Precision stages | ASML and specialist suppliers (Connecticut, per Patel; Europe) | Reticle and wafer stages that move in opposite directions with sub-nanometer overlay | Systems-level precision, not commodity mechanics |

Module supply | VDL and other Dutch high-tech firms | Vacuum vessels and mechatronic modules | A deep, co-developed Dutch supplier base built over decades |

Integration | ASML -- Veldhoven, Netherlands | Architecture, assembly, qualification, teardown, shipment, on-site rebuild | The tacit knowledge of making 100,000 parts work as one machine |

The pattern is the point. Each row is a near-monopoly held by one company in one place, and several of them sit inside ASML through ownership or decades of joint development. Zeiss does not sell its EUV optics to anyone else. Cymer is ASML. The drive laser comes from one firm in one German town. This is what makes the machine impossible to clone on a deadline: the hard part was never a blueprint you could steal. It is twenty-five years of co-developed process knowledge spread across optics, plasma physics, precision motion, metrology, and software, none of which is written down in one place. The EUV source alone has to fire a laser at tin droplets up to 100,000 times a second, in a vacuum, reliably enough to run inside a customer's fab. That is exotic physics and a production tool at the same time.

Why the global chain is also a ceiling

Here is the part worth dwelling on, because it is the one most coverage skips. The same distributed specialization that protects ASML also limits how fast it can grow. ASML shipped 48 EUV systems in 2025. Patel estimates the company can make about 70 a year now, 80 next year, and a little over 100 a year by the end of the decade even with aggressive expansion, at roughly $300 to $400 million per tool. He calls scaling EUV "production hell."

The reason is that you cannot scale an integrator faster than its scarcest supplier. Adding final-assembly capacity in Veldhoven does nothing unless Zeiss's mirror-coating capacity, Cymer's source capacity, TRUMPF's laser output, the stage builders, the supplier quality teams, the field engineers, and the spare-parts pipeline all move together. Each of those is its own artisanal, low-volume operation. As Patel describes the components, "you're not making tens of thousands of these a year, you're making hundreds, you're making thousands," and "any defect in these super thinly deposited stacks will mess it up." A single-source bottleneck is a wonderful thing when it blocks your competitors. It is a painful thing when your customers want another hundred tools and the one company that can polish the mirrors is already running flat out.

That ceiling is becoming everyone's problem. Patel argues that by 2028 or 2029, the binding constraint on AI compute moves down the stack to ASML, because leading-edge wafer output is gated by how many EUV tools exist. I recently wrote about how Google ended up renting its scarcest compute to a competitor; a few layers below that fight, the real scarcity is a few dozen machines a year from one Dutch company that depends on one German optics maker.

Map B: China, or one country trying to internalize all of it

China is attempting the opposite model, not by choice but by denial. Cut off from EUV since 2019 and from advanced deep-ultraviolet tools since 2023, it is building a parallel equipment supply chain inside its own borders, with SMIC and Huawei as the anchor customers and a roster of national champions filling each tool category. The progress is real, and it is wildly uneven.

Tool category | Chinese players | Status | Domestic share |

|---|---|---|---|

Etch | AMEC | Verifying 14 nm etch at SMIC; a 5 nm etch tool in validation at TSMC | Etch + deposition >40% |

Deposition / thermal | Naura | Mass-producing 28 nm tools; its furnaces are >60% of equipment on SMIC's 28 nm lines | (largest domestic maker) |

Thin-film (PECVD) | Piotech | Roughly doubled its share at YMTC's 3D NAND lines | included above |

Clean | ACM Research | Single-wafer cleaning tools at Hua Hong running above 90% utilization | high |

Track, CMP | Kingsemi, Hwatsing | Coat/develop tracks and chemical-mechanical polishing | moderate |

Lithography | SMEE; Yuliangsheng (SiCarrier-linked) | SMEE's 28 nm immersion in verification; SMIC testing a domestic immersion DUV tool, mostly Chinese-made but still using some imported parts | Lithography ~18% |

Metrology, EDA | SiCarrier subsidiaries and others | Domestic EDA and photoresist tools shown at trade shows | Metrology ~25%; EDA ~10% |

Read the right-hand column and the strategy snaps into focus. China is moving fastest exactly where the manufacturing problem is hard but modular: etch, deposition, thermal, cleaning, polishing. Those require deep process knowledge, but not a Zeiss-class mirror train or an EUV source firing plasma tens of thousands of times a second. Domestic substitution in etch and thin-film deposition is already above 40%, and overall domestic equipment share rose from 25% in 2024 to 35% in 2025. Naura booked more revenue in the first three quarters of 2025 than several times its entire 2020 take.

China remains farthest behind precisely where ASML's moat is deepest. Domestic substitution sits at roughly 18% for lithography, 25% for metrology, and barely above 10% for EDA software. Patel is blunt that the gap is still total at the frontier: "all of China's 7 nm and 14 nm capacity uses ASML DUV tools." A domestic 28 nm-class immersion DUV tool would matter a great deal, and with enough multi-patterning, DUV can be pushed toward more advanced nodes, though that route piles on masks, process steps, cycle time, and yield loss. It can be strategically useful even when it is economically ugly. There are reports of a Chinese EUV prototype assembled from components of older ASML systems, with a government target of chips by 2028 and 2030 seen as more realistic.

The distinction that matters is between a demonstration and a fleet. A tool that prints a wafer in a lab is a milestone. A fleet that holds uptime, overlay, throughput, service, spares, and yield steady across multiple fabs is a different industrial achievement, and it is the one China has not reached at the leading edge. Patel gives China credit and draws the line in the same breath: "I think they'll have working tools. I don't think that they'll be able to manufacture a bunch yet." His estimate is that China might reach about 100 DUV tools a year by 2030, against the hundreds ASML already ships.

The forcing function: export controls

None of China's localization push happens without the export controls that made it necessary, and the controls did something subtler than slow China down. They changed the procurement spec. A Chinese fab no longer just asks which tool performs best; it asks which tool it can still buy, service, and improve if foreign supply gets worse. That turns purchasing into industrial policy.

EUV has been blocked from China since 2019, and ASML says it has never shipped an EUV machine there. In 2023 and 2024 the Dutch and US governments extended controls into advanced immersion DUV, so ASML's most capable NXT:1970i and NXT:1980i tools now require Dutch export licenses. As of June 2026, a bipartisan US bill would go further and effectively ban all ASML DUV shipments to China, a category that is roughly a fifth of ASML's expected 2026 revenue.

The effect on ASML is that its largest growth market is turning into a political liability. China was about 29% of ASML's 2025 sales by one count and a third by another, and the company expects that to fall toward 20% in 2026. The effect on China is the multi-hundred-billion-yuan scramble now underway: Beijing has reportedly required new fab capacity to use more than 50% domestic equipment and discussed subsidies as large as 500 billion yuan. Controls did not slow China's equipment industry. They created its domestic market overnight.

Two philosophies of supply chain

Strip away the geopolitics and what is left are two genuinely different answers to the same question: do you optimize your supply chain for capability or for control?

Dimension | ASML model | China's domestic model |

|---|---|---|

Optimizing for | Maximum capability | Control under denial |

Structure | Specialized global suppliers, one integrator | State-backed localization across every tool category |

Core strength | Decades of tacit, co-developed knowledge | Fast demand pull from domestic fabs plus policy money |

Core weakness | Volume ceiling; political exposure across borders | Lower maturity in lithography, optics, metrology, EDA |

Hardest wall | Scaling artisanal suppliers without losing quality | Moving from working prototypes to production fleets |

ASML chose capability. By going to the single best supplier for every subsystem, wherever on earth it sits, it built a machine no one else can make. The cost is a chain that is volume-limited by its most artisanal link and politically exposed at every border it crosses. China is being forced to choose control. By rebuilding every tool category at home, it is trading the frontier for sovereignty, accepting tools a node or two behind in exchange for a chain no foreign government can switch off. Neither is wrong. They are different bets about which risk is more dangerous: not having the best tool, or not controlling the tool you have.

What is striking is that the deepest part of ASML's moat is the part China cannot buy its way around. You can fund an etch champion and reach 40% domestic share in a few years, because etch, while brutally hard, is a problem money and talent can attack in parallel. You cannot fund your way to a Zeiss, because the knowledge of how to polish a mirror to below an atom's thickness lives in a few hundred people and a few decades of failures, and it does not transfer on a five-year plan. My colleague Andy Hunt has written about why dual sourcing alone won't save your supply chain when every supposed alternative converges on the same sub-tier. ASML is the extreme version of that problem: at the very bottom of the world's most important supply chain sits one optics company with no real second source anywhere on the planet.

What this means for the rest of us

Most manufacturers are not building EUV machines, but almost every hardware company has its own version of the Zeiss problem: a single supplier, often several tiers down, that no one mapped until it became a crisis. A program can look comfortably dual-sourced at the tier-one level while both of those suppliers quietly depend on the same sub-tier coating, magnet, resin, or test socket. That is the trap multi-sourcing is supposed to prevent and often doesn't.

The lesson from ASML is not "go global" or "localize." It is that you cannot make either choice well if you cannot see your own supply chain to its roots, and the same make-versus-buy decision China is being forced to make at national scale shows up on every serious BOM. ASML knows its 5,100 suppliers and its critical chokepoints in granular detail; that visibility is part of why it can manage the risk at all. Most companies discover their tier-three dependency the week it stops shipping.

This is the gap LightSource is built to close for the companies we work with. The same speed-and-localization pressures playing out in semiconductors are reshaping ordinary automotive and electronics bills of materials too, and the compressed development cycles we examined in China Time only raise the stakes. A challenger manufacturer competing on speed cannot afford to learn where its single-source and long-lead exposures are only when one of them breaks. Connecting engineering, procurement, and suppliers in one system means a sole-source risk or a geographic concentration surfaces on the BOM while there is still time to qualify a second source or redesign around it. The operating question is the same whether you are ASML or a robotics startup: which supplier dependency will decide your ramp before the launch team even notices it is there?

China will likely close most of the mature-node equipment gap this decade, and may build DUV tools at real scale by 2030. The harder question is whether forced verticalization can ever reach the frontier that emergent global specialization built, or whether the optics wall holds for another decade. Either way, the contest is no longer just about who designs the best machine. It is about which kind of supply chain proves more durable: the one optimized to build the best possible tool, or the one optimized to never be cut off. We are about to find out which bet was right.

Sources

ASML 2025 Annual Report -- 5,100 suppliers and regional split, ~80% of BOM from suppliers, 2025 shipments (48 EUV, 279 DUV), €32.7B net sales.

ASML -- How we innovate -- ASML as "architect and integrator," supplier network, VDL example.

ASML -- Busting ASML myths -- ~100,000 parts; EUV ships as 40 containers, 3 cargo planes, 20 trucks.

ASML -- Lenses and mirrors -- Zeiss optics, EUV mirrors with 100+ layers polished below an atom's thickness.

ASML + Zeiss partnership (2016) -- ASML's 24.9% stake in Carl Zeiss SMT.

ASML -- Cymer -- San Diego light source; 2013 acquisition.

TRUMPF -- EUV lithography -- CO2 drive laser co-developed with ASML and Zeiss.

Dwarkesh Patel -- Dylan Patel -- "world's most complicated machine," "over ten thousand people," artisanal production, ~70-80 EUV/year, China DUV/EUV outlook.

TrendForce -- China domestic chip-equipment adoption hits 35% -- 25%->35% share; substitution by category (etch/deposition >40%, lithography 18%, metrology 25%); Naura, AMEC, Piotech, ACM.

TrendForce -- China chip-tool push, 70% target by 2027 -- SMEE 28 nm immersion in verification; EUV prototype reporting.

Tom's Hardware -- China's first domestic immersion DUV tool tested at SMIC -- domestic DUV, mostly Chinese-made, some imported parts.

ASML -- Dutch export license requirement (2024) -- NXT:1970i/1980i need Dutch licenses.

TechCrunch -- US bill targeting ASML DUV to China (June 2026) -- proposed DUV ban; DUV ~one-fifth of 2026 ASML revenue.

Caixin -- ASML expects China revenue to fall in 2026 -- China exposure falling toward ~20%.

Frequently Asked Questions

How many suppliers does ASML have, and why does it matter?

ASML reports about 5,100 suppliers, split roughly 1,600 in the Netherlands, 700 elsewhere in Europe, 1,350 in North America, and 1,450 in Asia, and it sources around 80% of an EUV machine's bill of materials from them. It matters because ASML is an integrator, not a vertically integrated manufacturer: its advantage is the global network of single-source specialists it has co-developed over decades, which is exactly what makes the machine impossible to copy quickly.

Why can ASML only build about 70 EUV machines a year?

Each machine has roughly 100,000 parts and depends on artisanal, single-source components like Carl Zeiss's EUV optics, which are polished to below the thickness of an atom. ASML can only scale as fast as its slowest critical supplier, because adding assembly capacity does nothing unless mirror, light-source, laser, and stage capacity all grow together. Dylan Patel estimates output at about 70 to 80 a year now, rising past 100 only by the end of the decade.

How close is China to replicating ASML's lithography machines?

China is closing the gap fast on etch, deposition, cleaning, and other non-lithography tools, where domestic substitution is above 40%, but it remains roughly a decade behind on lithography, where substitution is about 18% and there is no domestic EUV in volume production. SMEE's 28 nm immersion tool is in verification and a domestic DUV tool is being tested at SMIC, but as of 2026 all of China's 7 nm and 14 nm capacity still runs on ASML's deep-ultraviolet machines.

What are the export controls on ASML, and how is China responding?

EUV machines have been blocked from China since 2019, and advanced DUV tools since 2023-2024; a 2026 US bill proposes banning all ASML DUV shipments to China. In response, Beijing has reportedly mandated more than 50% domestic equipment for new fab capacity and discussed subsidies up to 500 billion yuan, which has turned export controls into the catalyst for China's domestic equipment industry.

What can an ordinary manufacturer learn from the ASML vs. China comparison?

The core lesson is that a supply chain optimized for the best possible product (ASML's global specialists) and one optimized for control (China's domestic chain) carry opposite risks: volume limits and political exposure versus being a step behind the frontier. Most companies have a hidden single-source dependency several tiers down, so the practical takeaway is to map your supply chain to its roots and decide, deliberately, whether to live with a chokepoint or invest in a real second source.

The single most important machine in the world economy is also one of the hardest to ship. When ASML sends an extreme-ultraviolet lithography system to a customer, it goes out as roughly 40 freight containers, three cargo planes, and 20 trucks, then gets reassembled in a cleanroom the size of a swimming pool. The machine has about 100,000 parts. ASML does not make most of them. The company describes itself as an "architect and integrator," and says it sources around 80% of its bill of materials from a network of about 5,100 suppliers. On Dwarkesh Patel's podcast in March, Dylan Patel of SemiAnalysis put the human scale of it plainly: ASML has said its supply chain involves "over ten thousand people." He called the result "the world's most complicated machine."

That dispersion is the whole story, and it cuts two ways. It is why no one has been able to copy ASML in forty years of trying, and it is also why ASML can build only about 70 of these machines a year. The same global supply chain that makes the EUV tool possible is the thing that caps how many can exist. And it is the backdrop for the most expensive industrial project on earth right now: China's attempt to rebuild the entire chipmaking-equipment supply chain inside one country, because export controls have left it no other option.

I want to map both chains, because the contrast is more useful than the headline. One is a story about specialization spread across the planet. The other is a story about a single nation trying to internalize all of it at once. Most companies will never operate at this scale, but the tradeoff underneath is the same one any manufacturer faces about its own critical suppliers: do you optimize for the best possible product, or for control of the supply that builds it?

Map A: ASML, or specialization spread across a planet

ASML's supply chain is not a pyramid with ASML on top. It is closer to a constellation of specialists, each of which is the best or only source for one impossibly hard thing, with ASML in the Netherlands integrating them into a working tool. The supplier base breaks down to roughly 1,600 in the Netherlands, 700 elsewhere in Europe, 1,350 in North America, and 1,450 in Asia. The critical few matter far more than the count.

Subsystem | Supplier / site | What it contributes | Why it's a chokepoint |

|---|---|---|---|

Optics | Carl Zeiss SMT -- Oberkochen, Germany | EUV mirrors (not lenses) with 100+ engineered layers, polished to below the thickness of a single atom | ASML's optics have come from Zeiss since the 1980s; ASML took a 24.9% stake in Zeiss SMT in 2016 to lock the relationship in |

Light source | Cymer / ASML -- San Diego, USA | Laser-produced-plasma source: tin droplets hit by laser pulses ~60,000 times a second to emit 13.5 nm light | The light source gated EUV for years; ASML bought Cymer in 2013 to control it |

Drive laser | TRUMPF -- Ditzingen, Germany | The high-power CO2 laser that vaporizes the tin droplets | Co-developed with ASML and Zeiss; no commodity substitute |

Precision stages | ASML and specialist suppliers (Connecticut, per Patel; Europe) | Reticle and wafer stages that move in opposite directions with sub-nanometer overlay | Systems-level precision, not commodity mechanics |

Module supply | VDL and other Dutch high-tech firms | Vacuum vessels and mechatronic modules | A deep, co-developed Dutch supplier base built over decades |

Integration | ASML -- Veldhoven, Netherlands | Architecture, assembly, qualification, teardown, shipment, on-site rebuild | The tacit knowledge of making 100,000 parts work as one machine |

The pattern is the point. Each row is a near-monopoly held by one company in one place, and several of them sit inside ASML through ownership or decades of joint development. Zeiss does not sell its EUV optics to anyone else. Cymer is ASML. The drive laser comes from one firm in one German town. This is what makes the machine impossible to clone on a deadline: the hard part was never a blueprint you could steal. It is twenty-five years of co-developed process knowledge spread across optics, plasma physics, precision motion, metrology, and software, none of which is written down in one place. The EUV source alone has to fire a laser at tin droplets up to 100,000 times a second, in a vacuum, reliably enough to run inside a customer's fab. That is exotic physics and a production tool at the same time.

Why the global chain is also a ceiling

Here is the part worth dwelling on, because it is the one most coverage skips. The same distributed specialization that protects ASML also limits how fast it can grow. ASML shipped 48 EUV systems in 2025. Patel estimates the company can make about 70 a year now, 80 next year, and a little over 100 a year by the end of the decade even with aggressive expansion, at roughly $300 to $400 million per tool. He calls scaling EUV "production hell."

The reason is that you cannot scale an integrator faster than its scarcest supplier. Adding final-assembly capacity in Veldhoven does nothing unless Zeiss's mirror-coating capacity, Cymer's source capacity, TRUMPF's laser output, the stage builders, the supplier quality teams, the field engineers, and the spare-parts pipeline all move together. Each of those is its own artisanal, low-volume operation. As Patel describes the components, "you're not making tens of thousands of these a year, you're making hundreds, you're making thousands," and "any defect in these super thinly deposited stacks will mess it up." A single-source bottleneck is a wonderful thing when it blocks your competitors. It is a painful thing when your customers want another hundred tools and the one company that can polish the mirrors is already running flat out.

That ceiling is becoming everyone's problem. Patel argues that by 2028 or 2029, the binding constraint on AI compute moves down the stack to ASML, because leading-edge wafer output is gated by how many EUV tools exist. I recently wrote about how Google ended up renting its scarcest compute to a competitor; a few layers below that fight, the real scarcity is a few dozen machines a year from one Dutch company that depends on one German optics maker.

Map B: China, or one country trying to internalize all of it

China is attempting the opposite model, not by choice but by denial. Cut off from EUV since 2019 and from advanced deep-ultraviolet tools since 2023, it is building a parallel equipment supply chain inside its own borders, with SMIC and Huawei as the anchor customers and a roster of national champions filling each tool category. The progress is real, and it is wildly uneven.

Tool category | Chinese players | Status | Domestic share |

|---|---|---|---|

Etch | AMEC | Verifying 14 nm etch at SMIC; a 5 nm etch tool in validation at TSMC | Etch + deposition >40% |

Deposition / thermal | Naura | Mass-producing 28 nm tools; its furnaces are >60% of equipment on SMIC's 28 nm lines | (largest domestic maker) |

Thin-film (PECVD) | Piotech | Roughly doubled its share at YMTC's 3D NAND lines | included above |

Clean | ACM Research | Single-wafer cleaning tools at Hua Hong running above 90% utilization | high |

Track, CMP | Kingsemi, Hwatsing | Coat/develop tracks and chemical-mechanical polishing | moderate |

Lithography | SMEE; Yuliangsheng (SiCarrier-linked) | SMEE's 28 nm immersion in verification; SMIC testing a domestic immersion DUV tool, mostly Chinese-made but still using some imported parts | Lithography ~18% |

Metrology, EDA | SiCarrier subsidiaries and others | Domestic EDA and photoresist tools shown at trade shows | Metrology ~25%; EDA ~10% |

Read the right-hand column and the strategy snaps into focus. China is moving fastest exactly where the manufacturing problem is hard but modular: etch, deposition, thermal, cleaning, polishing. Those require deep process knowledge, but not a Zeiss-class mirror train or an EUV source firing plasma tens of thousands of times a second. Domestic substitution in etch and thin-film deposition is already above 40%, and overall domestic equipment share rose from 25% in 2024 to 35% in 2025. Naura booked more revenue in the first three quarters of 2025 than several times its entire 2020 take.

China remains farthest behind precisely where ASML's moat is deepest. Domestic substitution sits at roughly 18% for lithography, 25% for metrology, and barely above 10% for EDA software. Patel is blunt that the gap is still total at the frontier: "all of China's 7 nm and 14 nm capacity uses ASML DUV tools." A domestic 28 nm-class immersion DUV tool would matter a great deal, and with enough multi-patterning, DUV can be pushed toward more advanced nodes, though that route piles on masks, process steps, cycle time, and yield loss. It can be strategically useful even when it is economically ugly. There are reports of a Chinese EUV prototype assembled from components of older ASML systems, with a government target of chips by 2028 and 2030 seen as more realistic.

The distinction that matters is between a demonstration and a fleet. A tool that prints a wafer in a lab is a milestone. A fleet that holds uptime, overlay, throughput, service, spares, and yield steady across multiple fabs is a different industrial achievement, and it is the one China has not reached at the leading edge. Patel gives China credit and draws the line in the same breath: "I think they'll have working tools. I don't think that they'll be able to manufacture a bunch yet." His estimate is that China might reach about 100 DUV tools a year by 2030, against the hundreds ASML already ships.

The forcing function: export controls

None of China's localization push happens without the export controls that made it necessary, and the controls did something subtler than slow China down. They changed the procurement spec. A Chinese fab no longer just asks which tool performs best; it asks which tool it can still buy, service, and improve if foreign supply gets worse. That turns purchasing into industrial policy.

EUV has been blocked from China since 2019, and ASML says it has never shipped an EUV machine there. In 2023 and 2024 the Dutch and US governments extended controls into advanced immersion DUV, so ASML's most capable NXT:1970i and NXT:1980i tools now require Dutch export licenses. As of June 2026, a bipartisan US bill would go further and effectively ban all ASML DUV shipments to China, a category that is roughly a fifth of ASML's expected 2026 revenue.

The effect on ASML is that its largest growth market is turning into a political liability. China was about 29% of ASML's 2025 sales by one count and a third by another, and the company expects that to fall toward 20% in 2026. The effect on China is the multi-hundred-billion-yuan scramble now underway: Beijing has reportedly required new fab capacity to use more than 50% domestic equipment and discussed subsidies as large as 500 billion yuan. Controls did not slow China's equipment industry. They created its domestic market overnight.

Two philosophies of supply chain

Strip away the geopolitics and what is left are two genuinely different answers to the same question: do you optimize your supply chain for capability or for control?

Dimension | ASML model | China's domestic model |

|---|---|---|

Optimizing for | Maximum capability | Control under denial |

Structure | Specialized global suppliers, one integrator | State-backed localization across every tool category |

Core strength | Decades of tacit, co-developed knowledge | Fast demand pull from domestic fabs plus policy money |

Core weakness | Volume ceiling; political exposure across borders | Lower maturity in lithography, optics, metrology, EDA |

Hardest wall | Scaling artisanal suppliers without losing quality | Moving from working prototypes to production fleets |

ASML chose capability. By going to the single best supplier for every subsystem, wherever on earth it sits, it built a machine no one else can make. The cost is a chain that is volume-limited by its most artisanal link and politically exposed at every border it crosses. China is being forced to choose control. By rebuilding every tool category at home, it is trading the frontier for sovereignty, accepting tools a node or two behind in exchange for a chain no foreign government can switch off. Neither is wrong. They are different bets about which risk is more dangerous: not having the best tool, or not controlling the tool you have.

What is striking is that the deepest part of ASML's moat is the part China cannot buy its way around. You can fund an etch champion and reach 40% domestic share in a few years, because etch, while brutally hard, is a problem money and talent can attack in parallel. You cannot fund your way to a Zeiss, because the knowledge of how to polish a mirror to below an atom's thickness lives in a few hundred people and a few decades of failures, and it does not transfer on a five-year plan. My colleague Andy Hunt has written about why dual sourcing alone won't save your supply chain when every supposed alternative converges on the same sub-tier. ASML is the extreme version of that problem: at the very bottom of the world's most important supply chain sits one optics company with no real second source anywhere on the planet.

What this means for the rest of us

Most manufacturers are not building EUV machines, but almost every hardware company has its own version of the Zeiss problem: a single supplier, often several tiers down, that no one mapped until it became a crisis. A program can look comfortably dual-sourced at the tier-one level while both of those suppliers quietly depend on the same sub-tier coating, magnet, resin, or test socket. That is the trap multi-sourcing is supposed to prevent and often doesn't.

The lesson from ASML is not "go global" or "localize." It is that you cannot make either choice well if you cannot see your own supply chain to its roots, and the same make-versus-buy decision China is being forced to make at national scale shows up on every serious BOM. ASML knows its 5,100 suppliers and its critical chokepoints in granular detail; that visibility is part of why it can manage the risk at all. Most companies discover their tier-three dependency the week it stops shipping.

This is the gap LightSource is built to close for the companies we work with. The same speed-and-localization pressures playing out in semiconductors are reshaping ordinary automotive and electronics bills of materials too, and the compressed development cycles we examined in China Time only raise the stakes. A challenger manufacturer competing on speed cannot afford to learn where its single-source and long-lead exposures are only when one of them breaks. Connecting engineering, procurement, and suppliers in one system means a sole-source risk or a geographic concentration surfaces on the BOM while there is still time to qualify a second source or redesign around it. The operating question is the same whether you are ASML or a robotics startup: which supplier dependency will decide your ramp before the launch team even notices it is there?

China will likely close most of the mature-node equipment gap this decade, and may build DUV tools at real scale by 2030. The harder question is whether forced verticalization can ever reach the frontier that emergent global specialization built, or whether the optics wall holds for another decade. Either way, the contest is no longer just about who designs the best machine. It is about which kind of supply chain proves more durable: the one optimized to build the best possible tool, or the one optimized to never be cut off. We are about to find out which bet was right.

Sources

ASML 2025 Annual Report -- 5,100 suppliers and regional split, ~80% of BOM from suppliers, 2025 shipments (48 EUV, 279 DUV), €32.7B net sales.

ASML -- How we innovate -- ASML as "architect and integrator," supplier network, VDL example.

ASML -- Busting ASML myths -- ~100,000 parts; EUV ships as 40 containers, 3 cargo planes, 20 trucks.

ASML -- Lenses and mirrors -- Zeiss optics, EUV mirrors with 100+ layers polished below an atom's thickness.

ASML + Zeiss partnership (2016) -- ASML's 24.9% stake in Carl Zeiss SMT.

ASML -- Cymer -- San Diego light source; 2013 acquisition.

TRUMPF -- EUV lithography -- CO2 drive laser co-developed with ASML and Zeiss.

Dwarkesh Patel -- Dylan Patel -- "world's most complicated machine," "over ten thousand people," artisanal production, ~70-80 EUV/year, China DUV/EUV outlook.

TrendForce -- China domestic chip-equipment adoption hits 35% -- 25%->35% share; substitution by category (etch/deposition >40%, lithography 18%, metrology 25%); Naura, AMEC, Piotech, ACM.

TrendForce -- China chip-tool push, 70% target by 2027 -- SMEE 28 nm immersion in verification; EUV prototype reporting.

Tom's Hardware -- China's first domestic immersion DUV tool tested at SMIC -- domestic DUV, mostly Chinese-made, some imported parts.

ASML -- Dutch export license requirement (2024) -- NXT:1970i/1980i need Dutch licenses.

TechCrunch -- US bill targeting ASML DUV to China (June 2026) -- proposed DUV ban; DUV ~one-fifth of 2026 ASML revenue.

Caixin -- ASML expects China revenue to fall in 2026 -- China exposure falling toward ~20%.

Frequently Asked Questions

How many suppliers does ASML have, and why does it matter?

ASML reports about 5,100 suppliers, split roughly 1,600 in the Netherlands, 700 elsewhere in Europe, 1,350 in North America, and 1,450 in Asia, and it sources around 80% of an EUV machine's bill of materials from them. It matters because ASML is an integrator, not a vertically integrated manufacturer: its advantage is the global network of single-source specialists it has co-developed over decades, which is exactly what makes the machine impossible to copy quickly.

Why can ASML only build about 70 EUV machines a year?

Each machine has roughly 100,000 parts and depends on artisanal, single-source components like Carl Zeiss's EUV optics, which are polished to below the thickness of an atom. ASML can only scale as fast as its slowest critical supplier, because adding assembly capacity does nothing unless mirror, light-source, laser, and stage capacity all grow together. Dylan Patel estimates output at about 70 to 80 a year now, rising past 100 only by the end of the decade.

How close is China to replicating ASML's lithography machines?

China is closing the gap fast on etch, deposition, cleaning, and other non-lithography tools, where domestic substitution is above 40%, but it remains roughly a decade behind on lithography, where substitution is about 18% and there is no domestic EUV in volume production. SMEE's 28 nm immersion tool is in verification and a domestic DUV tool is being tested at SMIC, but as of 2026 all of China's 7 nm and 14 nm capacity still runs on ASML's deep-ultraviolet machines.

What are the export controls on ASML, and how is China responding?

EUV machines have been blocked from China since 2019, and advanced DUV tools since 2023-2024; a 2026 US bill proposes banning all ASML DUV shipments to China. In response, Beijing has reportedly mandated more than 50% domestic equipment for new fab capacity and discussed subsidies up to 500 billion yuan, which has turned export controls into the catalyst for China's domestic equipment industry.

What can an ordinary manufacturer learn from the ASML vs. China comparison?

The core lesson is that a supply chain optimized for the best possible product (ASML's global specialists) and one optimized for control (China's domestic chain) carry opposite risks: volume limits and political exposure versus being a step behind the frontier. Most companies have a hidden single-source dependency several tiers down, so the practical takeaway is to map your supply chain to its roots and decide, deliberately, whether to live with a chokepoint or invest in a real second source.

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Trusted by:

Trusted by:

Trusted by: