Every Tier 1 supplier I talk to has the same line item on their 2026 strategic plan: dual-source critical components. After the semiconductor crisis, the Renesas fire, the Ukraine wire harness shutdown, and now the Jubail petrochemical attack, the logic feels obvious. Two sources are better than one. Spread the risk. Multi-sourcing as insurance policy.

The problem is that dual sourcing -- the way most Tier 1s are implementing it -- solves the wrong layer of the problem.

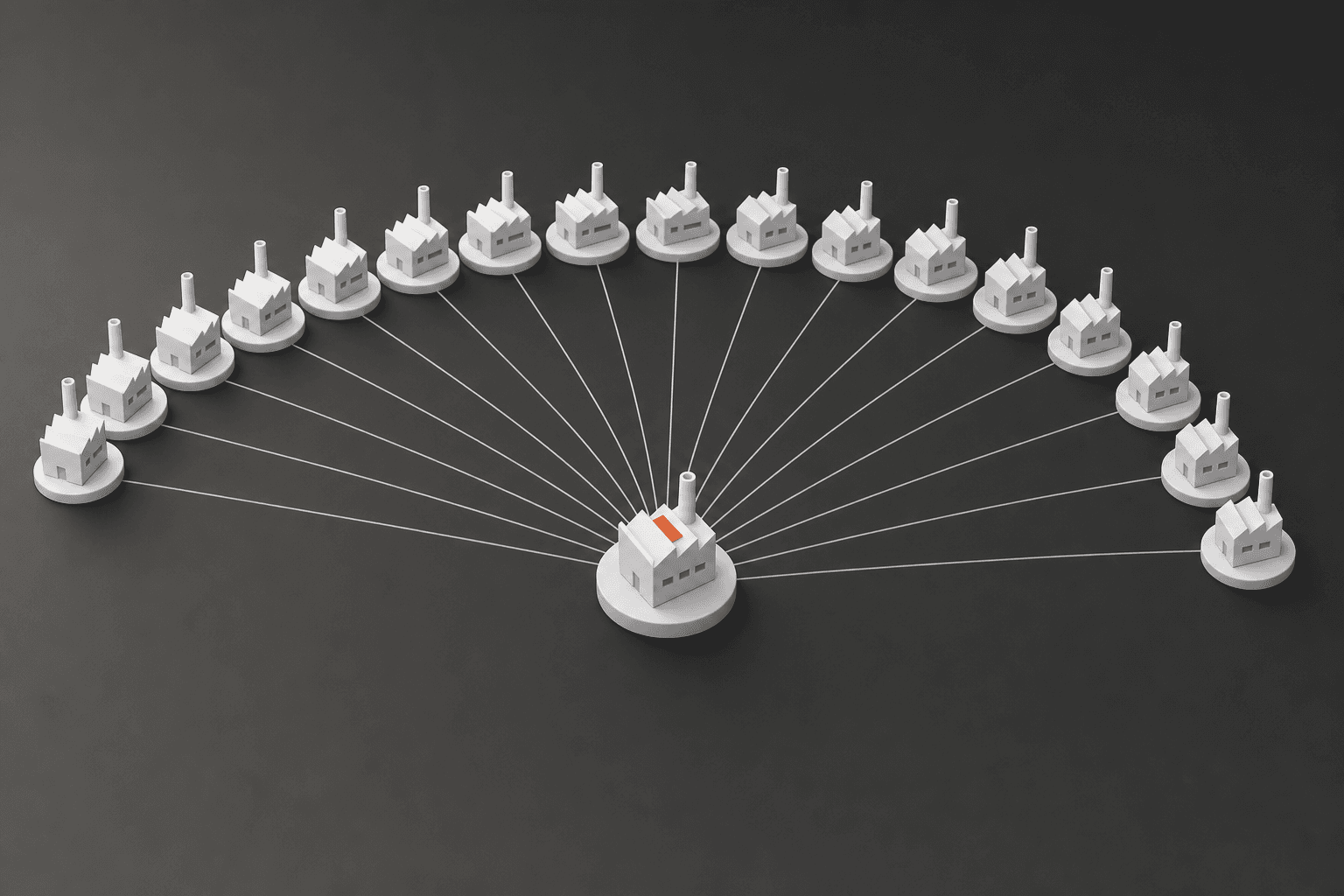

Let's say you're a mid-size Tier 1 building seat electronics assemblies. You have two contract manufacturers. One in Malaysia, one in Mexico. The second source costs more, but procurement did the right thing: kept it warm with 25% of the volume, ran PPAP, duplicated tooling. Then a resin plant three tiers upstream goes down. Both of your suppliers call within 48 hours. Different EMS sites, different freight lanes, different account managers -- but both of them buy PCB laminates from the same material supplier, who buys PPE resin from the same Saudi petrochemical complex.

On paper, you had two sources. In the real network, you had one choke point.

The 2026 tariff environment is making this convergence worse, not better. With U.S. average tariffs at their highest level since the 1930s and sub-tier suppliers consolidating under margin pressure, the industry is concentrating its upstream dependencies at the exact moment when diversification matters most.

What Dual Sourcing Actually Costs

The economics of dual sourcing aren't complicated. They're just unfriendly to a Tier 1 running on mid-single-digit margins.

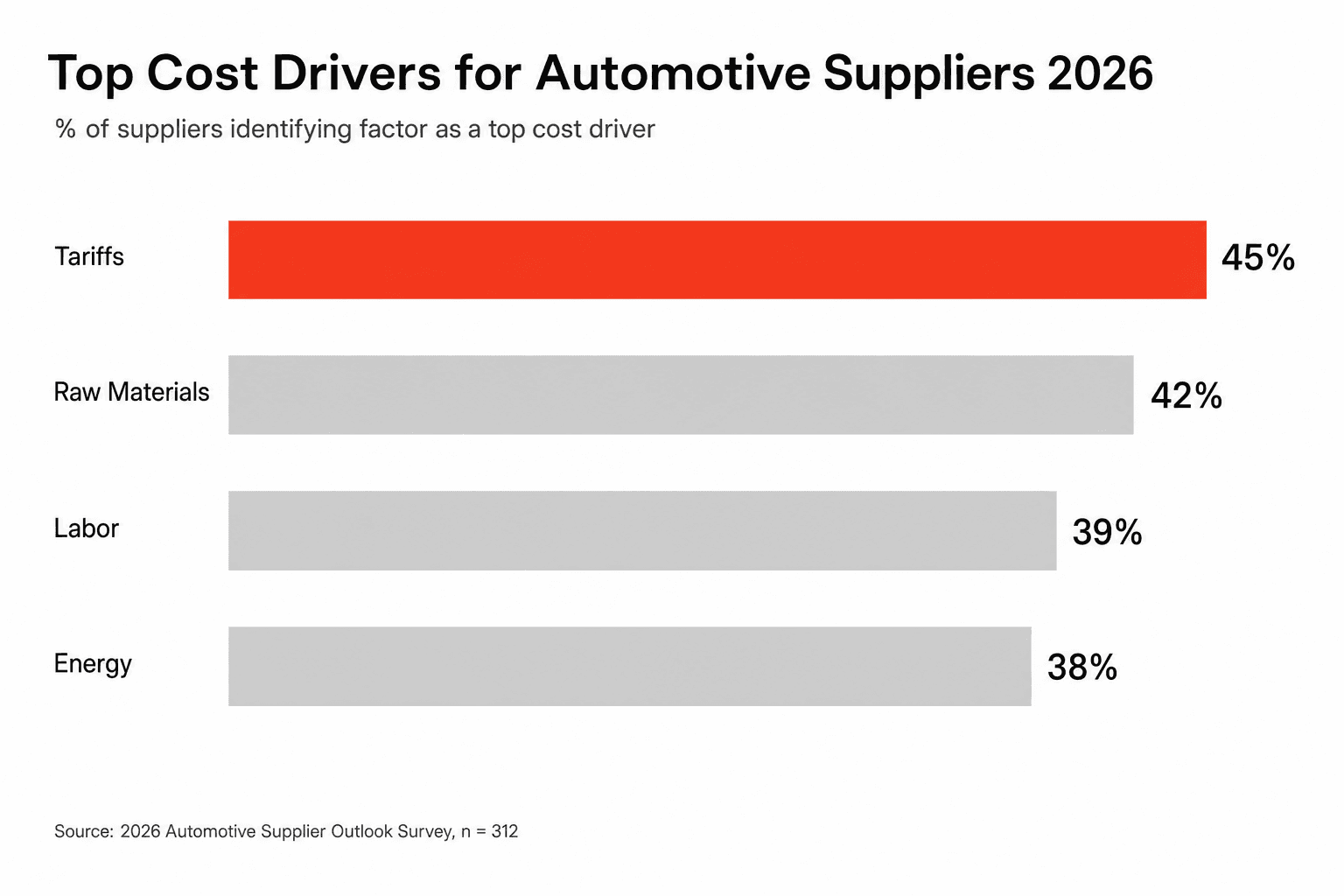

BCG's 2026 Global Automotive Supplier Study puts the average Tier 1 EBIT margin at 5.7%. OEMs are simultaneously pushing price-downs -- not just annually anymore, but quarterly in some programs. Tariffs have displaced raw materials as the number-one cost driver, cited by 45% of supplier executives in the most recent Automotive Logistics survey versus 42% for raw materials. Against that backdrop, every dollar spent on resilience competes with every other use of capital. The total cost of ownership calculation now includes risk.

A secondary source typically charges a 10-20% premium over your primary supplier. That's structural, not exploitative -- a supplier receiving 25% of your demand can't match the unit cost of one receiving 75%. One European electronics supplier documented the math after shifting to a 75/25 split: the backup vendor charged roughly 15% more per PCB. The annual cost increase was meaningful -- but less than the EUR 1.8 million in lost margin from an 8-week outage the previous year. The extra sourcing costs amortized in three years.

The harder constraint is CapEx. Dual sourcing commodity stampings or injection-molded parts is manageable. Dual sourcing a specialty die-cast housing, a custom ASIC, or a high-pressure fuel rail with $2-5 million in dedicated tooling? The economics often break. When tooling costs are that high, splitting volume may be economically impossible at current margins.

The practical consensus among Tier 1 procurement teams in 2026 is a 70/30 or 80/20 volume split, with a minimum of 20-30% allocated to the secondary source. Anything less is theater. A supplier receiving 2% of your demand won't prioritize you in a crisis -- they'll serve their 30% customers first. It's not on the approved vendor list if it can't actually show up.

The counterargument to "dual source everything" is strongest here: most Tier 1s can't afford it across the full BOM, and they shouldn't try. A seat frame bracket, a decorative plastic trim, and a safety-critical ECU don't deserve the same treatment. The sourcing strategy has to start with revenue-at-risk and lead time to recover, not just annual spend. A $6 sensor with a 9-month qualification path carries more risk than a $300 assembly with five qualified suppliers.

If your should-cost model doesn't include a resilience premium -- treating the 10-20% backup source cost as insurance against multi-million-dollar shutdowns -- your landed cost calculations are incomplete. And in 2026, landed cost that doesn't factor in tariff scenarios, HTS classification, and duty drawback eligibility isn't landed cost. It's a guess.

The Convergence Illusion

Here's the part that should keep you up at night. Even the components you've successfully dual-sourced may not actually be diversified.

A McKinsey study found that in a typical automotive supply chain, a single Tier 2 supplier serves an average of 14 different Tier 1 suppliers to the same OEM. Fourteen. When that shared Tier 2 goes down, your OEM customer doesn't lose one supply path -- they lose fourteen simultaneously. Your "backup" Tier 1 supplier was buying from the same upstream node you were.

The Deloitte CPO Survey puts the visibility problem in stark terms: only 15% of chief procurement officers have visibility beyond their Tier 1 suppliers. The other 85% are working from an incomplete map. They know who they buy from. They don't know who their suppliers buy from. And they definitely don't know where those supply chains converge three tiers deep.

This isn't abstract. Consider four convergence failures from the last 14 years, each one following the same pattern:

Evonik PA12 shortage, 2012. An explosion at Evonik's chemical plant in Marl, Germany disrupted production of cyclododecatriene -- a precursor for PA12 nylon used in automotive fuel lines, brake lines, and under-hood applications. The incident forced OEMs and Tier 1s into industry-wide scrambles for substitute materials. The constraint wasn't a Tier 1 assembly plant. It was a chemical input several steps upstream that most procurement teams had never mapped.

Renesas fire, March 2021. Renesas Electronics supplies roughly 30% of the global automotive microcontroller market. A fire at their Naka fab destroyed 23 manufacturing machines -- about 4% of the plant's equipment. Recovery took more than three months. Toyota, Nissan, Honda, and virtually every major OEM cut production. The total industry cost: an estimated $210 billion in lost automotive revenue and 12 million vehicles removed from global production in 2021-2022. Every Tier 1 ECU supplier, regardless of whether they had "dual sourced" their module production, traced back to the same handful of fabs.

Ukrainian neon, 2022. Two companies -- Ingas in Mariupol and Cryoin in Odesa -- produced 45-54% of the world's semiconductor-grade neon, a gas required for the laser lithography that makes every advanced chip. When Russia's invasion shut both facilities, neon prices quadrupled within weeks. Most Tier 1 buyers weren't sourcing neon -- they were sourcing ECUs, sensors, and power modules. But the chip fabs behind those components all depended on the same gas supply. The connection between "neon from a steel mill in Mariupol" and "my seat module supplier can't deliver" was invisible to most BOM cost management systems until it was too late.

Jubail petrochemical attack, April 2026. A missile strike hit the SABIC complex in Jubail, Saudi Arabia -- which produces approximately 70% of the world's high-purity PPE resin, a critical substrate for PCB laminates. Production halted. Within days, electronics and automotive suppliers globally faced severe PCB material shortages. This was a Tier 3 or Tier 4 input that most procurement teams had never mapped. The downstream effects are still rippling through global supply chains as of this writing.

The pattern is consistent: disruption doesn't hit where you're looking. It hits two or three tiers below your line of sight, at a convergence point you didn't know existed.

A useful test -- call it the "same phone call" test -- is simple: if Supplier A and Supplier B would both call the same sub-tier during a crisis, you do not have independent recovery paths. For each critical part, ask four questions:

Do our two suppliers share the same parent company, financial sponsor, or major sub-tier?

Do they depend on the same manufacturing site, even through different invoicing entities?

Do they rely on the same constrained input -- resin, gas, wafer capacity, specialty steel, plating chemistry?

Would a substitution still require months of requalification regardless of source count?

If any answer is yes, you may still want both suppliers. But you shouldn't call it a fully resilient design.

The Tariff Accelerant

The 2026 tariff environment isn't just adding cost. It's actively concentrating sub-tier supply chains.

The numbers are stark. BCG reports U.S. average trade-weighted tariffs at roughly 16% -- the highest since the Smoot-Hawley era of the 1930s. Effective tariffs on Chinese imports average 48%. Section 232 duties impose 25% on imported vehicles and auto parts. The combined impact: an estimated $85 billion in additional annual costs across the industry.

For Tier 1 suppliers, these tariffs create a three-way squeeze. First, direct cost increases on imported components. Second, OEM pressure to absorb those increases. Third -- and this is the one that gets less attention -- the downstream effects on your sub-tier suppliers.

Smaller Tier 2 and Tier 3 suppliers don't have the balance sheets to absorb a 25% tariff spike. Many can't invest in the compliance systems required for HTS classification and tariff drawback programs. The result is consolidation. Global automotive supplier M&A hit $35 billion in the first nine months of 2025, with average deal values doubling to $1.2 billion versus 2023. Liquidity pressure is pushing smaller sub-tier suppliers toward restructuring or acquisition.

Every acquisition that removes a sub-tier supplier from the market increases concentration risk. If your two "diversified" sources for a machined housing both relied on the same small Tier 3 heat-treatment shop, and that shop gets acquired by a larger player who rationalizes capacity -- your diversification just evaporated.

The automation gap compounds the problem. OEMs and Tier 1s invest adequately in robotics at rates of 51-62%. At Tier 2, that drops to 31%. At Tier 3, it's 23%. The suppliers most vulnerable to tariff-driven cost pressure are also the least equipped to adapt.

And there's a new bottleneck emerging from outside automotive entirely: DRAM. AI data center demand is pulling enormous memory capacity into servers. Vehicles are adding more memory content through ADAS, infotainment, and connected features. Even a Tier 1 with strong MCU supplier relationships may face allocation on memory because the shortage is driven by a different end market. The auto industry sometimes assumes its importance gives it priority. At data center margins, that assumption doesn't hold.

The USMCA Wild Card

Layered on top of the tariff environment is the USMCA six-year review, due by mid-2026. The agreement enables $1.6 trillion in annual North American trilateral trade -- including the deeply integrated automotive supply chain where parts cross the U.S., Mexico, and Canada borders multiple times before final assembly.

The U.S. administration has signaled it will seek tighter rules, potentially higher regional value content thresholds beyond the current 75% for vehicles, and has floated the possibility of replacing the trilateral agreement with bilateral deals. Canada's trade minister Dominic LeBlanc warned that the review uncertainty alone is causing a "break in investment decisions" -- net business investment in Canada is down as companies hesitate to build capacity without knowing the future tariff landscape.

For a Tier 1 trying to nearshore supply into Mexico to dodge Section 232 tariffs, the USMCA review injects a second layer of uncertainty. You're moving supply chains to qualify for trade rules that might change within 18 months. And despite tariff pressure, only about 36% of companies are actively reshoring production to the U.S. The majority are nearshoring selectively, going further offshore, or simply waiting.

The critical nuance: "local" is not the same as "resilient." A local supplier can still be financially weak. A regional source can still depend on a single imported material. A tariff-friendly supplier can still create a new concentration risk if every Tier 1 in the region is onboarding them simultaneously.

What Real Resilience Requires

Dual sourcing is a necessary component of resilience. It's not sufficient. The Tier 1s that are genuinely resilient -- not just checking a box for OEM compliance -- share five characteristics:

1. They map constraints, not just suppliers. For each critical component, they identify the true constraint layer: manufacturing site, parent company, critical sub-tier, raw material input, semiconductor fab, tooling location, qualification path, and tariff exposure. The point isn't to map the entire world. It's to find the few places where apparent options collapse into one dependency. Supplier performance management that stops at OTIF and PPM is looking at history. Constraint mapping tells you what happens when a hidden node fails tomorrow.

2. They prioritize by line-stopper risk, not annual spend. A $2 connector with no substitute and a 9-month requalification path carries more risk than a $300 assembly with five qualified sources. The first cut should be: which parts stop customer production? Overlay revenue-at-risk, customer penalty exposure, and time-to-recover before overlay spend.

3. They use engineering as a sourcing lever. Pre-qualifying pin-compatible MCUs, maintaining approved alternate resins, documenting firmware impacts before a crisis -- these engineering decisions determine whether procurement has options later. This isn't procurement telling engineering how to design. It's bringing supply reality into design reviews early enough to matter.

4. They monitor sub-tier financial health. The next disruption may not be a fire or a missile. It may be a Tier 3 supplier quietly going bankrupt because they can't absorb the tariff increase. Monitoring credit ratings, payment patterns, and revenue concentration at Tier 2 and Tier 3 gives lead time to qualify alternatives before the failure reaches your line.

5. They model scenarios, not just suppliers. What happens if a key resin is allocated at 50% for six weeks? What if Section 232 duties hit this assembly and the customer refuses a price adjustment? What if USMCA rules of origin change for this program? The Tier 1s with real resilience can answer these questions before the scenario becomes reality -- because they've connected RFQs, BOMs, supplier data, cost breakdowns, and tariff exposure in one system rather than six spreadsheets.

LightSource works with manufacturers building exactly this kind of connected view -- linking engineering specs, procurement decisions, supplier quotes, and cost data so teams can see how sourcing choices affect both cost and supply exposure at the part and program level. The practical value isn't a dashboard. It's being able to compare sourcing options against tariff scenarios and concentration risk before a decision hardens.

The Hard Math

The average Tier 1 automotive supplier in 2026 is caught between competing demands. OEMs want dual sourcing. Margins can't fund it everywhere. Tariffs are rising. Sub-tier suppliers are consolidating. The USMCA review might rewrite North American trade rules. And the next chip bottleneck may come from AI data center demand, not automotive.

There's no version of this where resilience is free. The question is whether you spend the money on the right risks. Dual sourcing your commodity parts is table stakes. The harder, more valuable work is mapping sub-tier convergence points, monitoring the financial health of concentrated suppliers you can't easily replace, using engineering to pre-qualify alternate materials and components, and building cost models that treat tariff volatility and disruption probability as inputs rather than surprises.

The 2026 Working Relations Index showed OEM-supplier relationships improving for the first time in 26 years. That matters -- because the Tier 1s that can have honest conversations with their OEM customers about the cost of resilience will be better positioned than those that absorb it silently. But the relationships that matter most for resilience aren't between OEMs and Tier 1s. They're between Tier 1s and the Tier 2s and Tier 3s that the industry still can't see.

Sources

BCG 2026 Global Automotive Supplier Study -- supplier margin data (5.7% EBIT), tariff impact analysis, U.S. average tariff at 16%

KPMG: Beyond Tier 1 -- A New Playbook for Multi-Tier Supplier Risk -- sub-tier visibility framework, risk categories, seat manufacturer example

Moody's: Hidden Semiconductor Risks in Automotive Supply Chains -- Tier 2/3 concentration data, $210B lost revenue estimate, 12M vehicles removed from production

Automotive Logistics: Supply Chains Redesigned Amid Disruptions -- tariffs as #1 cost driver (45%), reshoring data (36% active), automation gap by tier

AP News: USMCA 2026 Review -- Canadian trade minister on investment uncertainty, $1.6T trilateral trade

AP News: U.S.-China Tariff Levels -- effective tariffs on Chinese imports at 48%, China's share of U.S. trade from 13% to 6%

Tom's Hardware: Jubail PCB Resin Attack -- SABIC complex producing 70% of global PPE resin

Reuters/Investing.com: Ukraine Neon Disruption -- 45-54% of semiconductor-grade neon, 4x price spike

Kloepfel Consulting: Single vs. Multiple Sourcing 2026 -- dual sourcing cost premiums (15% example), volume split best practices, 3-year amortization

PwC: Section 232 Auto Tariffs -- tariff compliance framework, supplier offset mechanisms

Embedded Computing: Renesas Fire Analysis -- 30% automotive MCU market share, 3-month recovery, production cuts at Toyota/Nissan

Frequently Asked Questions

What is sub-tier convergence in automotive supply chains?

Sub-tier convergence happens when multiple direct suppliers depend on the same upstream supplier, facility, material, or process. A Tier 1 may have two qualified suppliers on paper, but both may rely on the same semiconductor fab, resin plant, specialty gas source, or tooling provider. McKinsey found that a single Tier 2 supplier serves an average of 14 different Tier 1s to the same OEM -- meaning a failure at that convergence point cascades across the entire supply network simultaneously.

Why isn't dual sourcing enough to protect against supply chain disruptions?

Dual sourcing reduces risk at the direct supplier level but doesn't guarantee independence deeper in the network. The Renesas fire, Ukrainian neon disruption, and Jubail petrochemical attack all followed the same pattern: Tier 1s with dual-sourced assemblies discovered both sources depended on the same upstream node. Dual sourcing works best when combined with sub-tier visibility, constraint mapping, and engineering strategies that pre-qualify alternative materials and components.

How much does dual sourcing typically cost a Tier 1 automotive supplier?

The backup source typically charges a 10-20% premium due to lower volume allocation. Most Tier 1s use a 70/30 or 80/20 split, with the secondary source needing at least 20-30% of total volume to remain commercially viable. Additional costs include duplicate tooling (which can range from hundreds of thousands to millions for specialty parts), quality management overhead, and PPAP validation. For highly specialized components with expensive dedicated tooling, dual sourcing may be economically impossible at current Tier 1 margins of ~5.7% EBIT.

How are 2026 tariffs affecting Tier 1 supplier sourcing strategies?

U.S. import tariffs average 16% -- the highest since the 1930s -- with 48% on Chinese goods and 25% Section 232 duties on auto parts. The combined industry impact is estimated at $85 billion annually. Tariffs have become the number-one cost driver, cited by 45% of supplier executives. Many Tier 1s are nearshoring to Mexico, but the 2026 USMCA review creates uncertainty about whether those investments will continue to qualify for duty-free treatment. Tariffs are also accelerating sub-tier consolidation as smaller Tier 2/3 suppliers can't absorb the cost increases.

What should a Tier 1 supplier do first to improve real supply chain resilience?

Start by identifying line-stopper parts -- the components that stop customer production regardless of cost, not just the highest-spend items. Then map the true upstream constraints: sub-tier suppliers, manufacturing sites, raw material inputs, semiconductor fabs, and qualification paths. Apply the "same phone call" test: if both of your suppliers would call the same sub-tier during a crisis, you don't have independent recovery paths. From there, prioritize engineering pre-qualification of alternatives, sub-tier financial health monitoring, and scenario modeling that connects tariff exposure to sourcing decisions.

Every Tier 1 supplier I talk to has the same line item on their 2026 strategic plan: dual-source critical components. After the semiconductor crisis, the Renesas fire, the Ukraine wire harness shutdown, and now the Jubail petrochemical attack, the logic feels obvious. Two sources are better than one. Spread the risk. Multi-sourcing as insurance policy.

The problem is that dual sourcing -- the way most Tier 1s are implementing it -- solves the wrong layer of the problem.

Let's say you're a mid-size Tier 1 building seat electronics assemblies. You have two contract manufacturers. One in Malaysia, one in Mexico. The second source costs more, but procurement did the right thing: kept it warm with 25% of the volume, ran PPAP, duplicated tooling. Then a resin plant three tiers upstream goes down. Both of your suppliers call within 48 hours. Different EMS sites, different freight lanes, different account managers -- but both of them buy PCB laminates from the same material supplier, who buys PPE resin from the same Saudi petrochemical complex.

On paper, you had two sources. In the real network, you had one choke point.

The 2026 tariff environment is making this convergence worse, not better. With U.S. average tariffs at their highest level since the 1930s and sub-tier suppliers consolidating under margin pressure, the industry is concentrating its upstream dependencies at the exact moment when diversification matters most.

What Dual Sourcing Actually Costs

The economics of dual sourcing aren't complicated. They're just unfriendly to a Tier 1 running on mid-single-digit margins.

BCG's 2026 Global Automotive Supplier Study puts the average Tier 1 EBIT margin at 5.7%. OEMs are simultaneously pushing price-downs -- not just annually anymore, but quarterly in some programs. Tariffs have displaced raw materials as the number-one cost driver, cited by 45% of supplier executives in the most recent Automotive Logistics survey versus 42% for raw materials. Against that backdrop, every dollar spent on resilience competes with every other use of capital. The total cost of ownership calculation now includes risk.

A secondary source typically charges a 10-20% premium over your primary supplier. That's structural, not exploitative -- a supplier receiving 25% of your demand can't match the unit cost of one receiving 75%. One European electronics supplier documented the math after shifting to a 75/25 split: the backup vendor charged roughly 15% more per PCB. The annual cost increase was meaningful -- but less than the EUR 1.8 million in lost margin from an 8-week outage the previous year. The extra sourcing costs amortized in three years.

The harder constraint is CapEx. Dual sourcing commodity stampings or injection-molded parts is manageable. Dual sourcing a specialty die-cast housing, a custom ASIC, or a high-pressure fuel rail with $2-5 million in dedicated tooling? The economics often break. When tooling costs are that high, splitting volume may be economically impossible at current margins.

The practical consensus among Tier 1 procurement teams in 2026 is a 70/30 or 80/20 volume split, with a minimum of 20-30% allocated to the secondary source. Anything less is theater. A supplier receiving 2% of your demand won't prioritize you in a crisis -- they'll serve their 30% customers first. It's not on the approved vendor list if it can't actually show up.

The counterargument to "dual source everything" is strongest here: most Tier 1s can't afford it across the full BOM, and they shouldn't try. A seat frame bracket, a decorative plastic trim, and a safety-critical ECU don't deserve the same treatment. The sourcing strategy has to start with revenue-at-risk and lead time to recover, not just annual spend. A $6 sensor with a 9-month qualification path carries more risk than a $300 assembly with five qualified suppliers.

If your should-cost model doesn't include a resilience premium -- treating the 10-20% backup source cost as insurance against multi-million-dollar shutdowns -- your landed cost calculations are incomplete. And in 2026, landed cost that doesn't factor in tariff scenarios, HTS classification, and duty drawback eligibility isn't landed cost. It's a guess.

The Convergence Illusion

Here's the part that should keep you up at night. Even the components you've successfully dual-sourced may not actually be diversified.

A McKinsey study found that in a typical automotive supply chain, a single Tier 2 supplier serves an average of 14 different Tier 1 suppliers to the same OEM. Fourteen. When that shared Tier 2 goes down, your OEM customer doesn't lose one supply path -- they lose fourteen simultaneously. Your "backup" Tier 1 supplier was buying from the same upstream node you were.

The Deloitte CPO Survey puts the visibility problem in stark terms: only 15% of chief procurement officers have visibility beyond their Tier 1 suppliers. The other 85% are working from an incomplete map. They know who they buy from. They don't know who their suppliers buy from. And they definitely don't know where those supply chains converge three tiers deep.

This isn't abstract. Consider four convergence failures from the last 14 years, each one following the same pattern:

Evonik PA12 shortage, 2012. An explosion at Evonik's chemical plant in Marl, Germany disrupted production of cyclododecatriene -- a precursor for PA12 nylon used in automotive fuel lines, brake lines, and under-hood applications. The incident forced OEMs and Tier 1s into industry-wide scrambles for substitute materials. The constraint wasn't a Tier 1 assembly plant. It was a chemical input several steps upstream that most procurement teams had never mapped.

Renesas fire, March 2021. Renesas Electronics supplies roughly 30% of the global automotive microcontroller market. A fire at their Naka fab destroyed 23 manufacturing machines -- about 4% of the plant's equipment. Recovery took more than three months. Toyota, Nissan, Honda, and virtually every major OEM cut production. The total industry cost: an estimated $210 billion in lost automotive revenue and 12 million vehicles removed from global production in 2021-2022. Every Tier 1 ECU supplier, regardless of whether they had "dual sourced" their module production, traced back to the same handful of fabs.

Ukrainian neon, 2022. Two companies -- Ingas in Mariupol and Cryoin in Odesa -- produced 45-54% of the world's semiconductor-grade neon, a gas required for the laser lithography that makes every advanced chip. When Russia's invasion shut both facilities, neon prices quadrupled within weeks. Most Tier 1 buyers weren't sourcing neon -- they were sourcing ECUs, sensors, and power modules. But the chip fabs behind those components all depended on the same gas supply. The connection between "neon from a steel mill in Mariupol" and "my seat module supplier can't deliver" was invisible to most BOM cost management systems until it was too late.

Jubail petrochemical attack, April 2026. A missile strike hit the SABIC complex in Jubail, Saudi Arabia -- which produces approximately 70% of the world's high-purity PPE resin, a critical substrate for PCB laminates. Production halted. Within days, electronics and automotive suppliers globally faced severe PCB material shortages. This was a Tier 3 or Tier 4 input that most procurement teams had never mapped. The downstream effects are still rippling through global supply chains as of this writing.

The pattern is consistent: disruption doesn't hit where you're looking. It hits two or three tiers below your line of sight, at a convergence point you didn't know existed.

A useful test -- call it the "same phone call" test -- is simple: if Supplier A and Supplier B would both call the same sub-tier during a crisis, you do not have independent recovery paths. For each critical part, ask four questions:

Do our two suppliers share the same parent company, financial sponsor, or major sub-tier?

Do they depend on the same manufacturing site, even through different invoicing entities?

Do they rely on the same constrained input -- resin, gas, wafer capacity, specialty steel, plating chemistry?

Would a substitution still require months of requalification regardless of source count?

If any answer is yes, you may still want both suppliers. But you shouldn't call it a fully resilient design.

The Tariff Accelerant

The 2026 tariff environment isn't just adding cost. It's actively concentrating sub-tier supply chains.

The numbers are stark. BCG reports U.S. average trade-weighted tariffs at roughly 16% -- the highest since the Smoot-Hawley era of the 1930s. Effective tariffs on Chinese imports average 48%. Section 232 duties impose 25% on imported vehicles and auto parts. The combined impact: an estimated $85 billion in additional annual costs across the industry.

For Tier 1 suppliers, these tariffs create a three-way squeeze. First, direct cost increases on imported components. Second, OEM pressure to absorb those increases. Third -- and this is the one that gets less attention -- the downstream effects on your sub-tier suppliers.

Smaller Tier 2 and Tier 3 suppliers don't have the balance sheets to absorb a 25% tariff spike. Many can't invest in the compliance systems required for HTS classification and tariff drawback programs. The result is consolidation. Global automotive supplier M&A hit $35 billion in the first nine months of 2025, with average deal values doubling to $1.2 billion versus 2023. Liquidity pressure is pushing smaller sub-tier suppliers toward restructuring or acquisition.

Every acquisition that removes a sub-tier supplier from the market increases concentration risk. If your two "diversified" sources for a machined housing both relied on the same small Tier 3 heat-treatment shop, and that shop gets acquired by a larger player who rationalizes capacity -- your diversification just evaporated.

The automation gap compounds the problem. OEMs and Tier 1s invest adequately in robotics at rates of 51-62%. At Tier 2, that drops to 31%. At Tier 3, it's 23%. The suppliers most vulnerable to tariff-driven cost pressure are also the least equipped to adapt.

And there's a new bottleneck emerging from outside automotive entirely: DRAM. AI data center demand is pulling enormous memory capacity into servers. Vehicles are adding more memory content through ADAS, infotainment, and connected features. Even a Tier 1 with strong MCU supplier relationships may face allocation on memory because the shortage is driven by a different end market. The auto industry sometimes assumes its importance gives it priority. At data center margins, that assumption doesn't hold.

The USMCA Wild Card

Layered on top of the tariff environment is the USMCA six-year review, due by mid-2026. The agreement enables $1.6 trillion in annual North American trilateral trade -- including the deeply integrated automotive supply chain where parts cross the U.S., Mexico, and Canada borders multiple times before final assembly.

The U.S. administration has signaled it will seek tighter rules, potentially higher regional value content thresholds beyond the current 75% for vehicles, and has floated the possibility of replacing the trilateral agreement with bilateral deals. Canada's trade minister Dominic LeBlanc warned that the review uncertainty alone is causing a "break in investment decisions" -- net business investment in Canada is down as companies hesitate to build capacity without knowing the future tariff landscape.

For a Tier 1 trying to nearshore supply into Mexico to dodge Section 232 tariffs, the USMCA review injects a second layer of uncertainty. You're moving supply chains to qualify for trade rules that might change within 18 months. And despite tariff pressure, only about 36% of companies are actively reshoring production to the U.S. The majority are nearshoring selectively, going further offshore, or simply waiting.

The critical nuance: "local" is not the same as "resilient." A local supplier can still be financially weak. A regional source can still depend on a single imported material. A tariff-friendly supplier can still create a new concentration risk if every Tier 1 in the region is onboarding them simultaneously.

What Real Resilience Requires

Dual sourcing is a necessary component of resilience. It's not sufficient. The Tier 1s that are genuinely resilient -- not just checking a box for OEM compliance -- share five characteristics:

1. They map constraints, not just suppliers. For each critical component, they identify the true constraint layer: manufacturing site, parent company, critical sub-tier, raw material input, semiconductor fab, tooling location, qualification path, and tariff exposure. The point isn't to map the entire world. It's to find the few places where apparent options collapse into one dependency. Supplier performance management that stops at OTIF and PPM is looking at history. Constraint mapping tells you what happens when a hidden node fails tomorrow.

2. They prioritize by line-stopper risk, not annual spend. A $2 connector with no substitute and a 9-month requalification path carries more risk than a $300 assembly with five qualified sources. The first cut should be: which parts stop customer production? Overlay revenue-at-risk, customer penalty exposure, and time-to-recover before overlay spend.

3. They use engineering as a sourcing lever. Pre-qualifying pin-compatible MCUs, maintaining approved alternate resins, documenting firmware impacts before a crisis -- these engineering decisions determine whether procurement has options later. This isn't procurement telling engineering how to design. It's bringing supply reality into design reviews early enough to matter.

4. They monitor sub-tier financial health. The next disruption may not be a fire or a missile. It may be a Tier 3 supplier quietly going bankrupt because they can't absorb the tariff increase. Monitoring credit ratings, payment patterns, and revenue concentration at Tier 2 and Tier 3 gives lead time to qualify alternatives before the failure reaches your line.

5. They model scenarios, not just suppliers. What happens if a key resin is allocated at 50% for six weeks? What if Section 232 duties hit this assembly and the customer refuses a price adjustment? What if USMCA rules of origin change for this program? The Tier 1s with real resilience can answer these questions before the scenario becomes reality -- because they've connected RFQs, BOMs, supplier data, cost breakdowns, and tariff exposure in one system rather than six spreadsheets.

LightSource works with manufacturers building exactly this kind of connected view -- linking engineering specs, procurement decisions, supplier quotes, and cost data so teams can see how sourcing choices affect both cost and supply exposure at the part and program level. The practical value isn't a dashboard. It's being able to compare sourcing options against tariff scenarios and concentration risk before a decision hardens.

The Hard Math

The average Tier 1 automotive supplier in 2026 is caught between competing demands. OEMs want dual sourcing. Margins can't fund it everywhere. Tariffs are rising. Sub-tier suppliers are consolidating. The USMCA review might rewrite North American trade rules. And the next chip bottleneck may come from AI data center demand, not automotive.

There's no version of this where resilience is free. The question is whether you spend the money on the right risks. Dual sourcing your commodity parts is table stakes. The harder, more valuable work is mapping sub-tier convergence points, monitoring the financial health of concentrated suppliers you can't easily replace, using engineering to pre-qualify alternate materials and components, and building cost models that treat tariff volatility and disruption probability as inputs rather than surprises.

The 2026 Working Relations Index showed OEM-supplier relationships improving for the first time in 26 years. That matters -- because the Tier 1s that can have honest conversations with their OEM customers about the cost of resilience will be better positioned than those that absorb it silently. But the relationships that matter most for resilience aren't between OEMs and Tier 1s. They're between Tier 1s and the Tier 2s and Tier 3s that the industry still can't see.

Sources

BCG 2026 Global Automotive Supplier Study -- supplier margin data (5.7% EBIT), tariff impact analysis, U.S. average tariff at 16%

KPMG: Beyond Tier 1 -- A New Playbook for Multi-Tier Supplier Risk -- sub-tier visibility framework, risk categories, seat manufacturer example

Moody's: Hidden Semiconductor Risks in Automotive Supply Chains -- Tier 2/3 concentration data, $210B lost revenue estimate, 12M vehicles removed from production

Automotive Logistics: Supply Chains Redesigned Amid Disruptions -- tariffs as #1 cost driver (45%), reshoring data (36% active), automation gap by tier

AP News: USMCA 2026 Review -- Canadian trade minister on investment uncertainty, $1.6T trilateral trade

AP News: U.S.-China Tariff Levels -- effective tariffs on Chinese imports at 48%, China's share of U.S. trade from 13% to 6%

Tom's Hardware: Jubail PCB Resin Attack -- SABIC complex producing 70% of global PPE resin

Reuters/Investing.com: Ukraine Neon Disruption -- 45-54% of semiconductor-grade neon, 4x price spike

Kloepfel Consulting: Single vs. Multiple Sourcing 2026 -- dual sourcing cost premiums (15% example), volume split best practices, 3-year amortization

PwC: Section 232 Auto Tariffs -- tariff compliance framework, supplier offset mechanisms

Embedded Computing: Renesas Fire Analysis -- 30% automotive MCU market share, 3-month recovery, production cuts at Toyota/Nissan

Frequently Asked Questions

What is sub-tier convergence in automotive supply chains?

Sub-tier convergence happens when multiple direct suppliers depend on the same upstream supplier, facility, material, or process. A Tier 1 may have two qualified suppliers on paper, but both may rely on the same semiconductor fab, resin plant, specialty gas source, or tooling provider. McKinsey found that a single Tier 2 supplier serves an average of 14 different Tier 1s to the same OEM -- meaning a failure at that convergence point cascades across the entire supply network simultaneously.

Why isn't dual sourcing enough to protect against supply chain disruptions?

Dual sourcing reduces risk at the direct supplier level but doesn't guarantee independence deeper in the network. The Renesas fire, Ukrainian neon disruption, and Jubail petrochemical attack all followed the same pattern: Tier 1s with dual-sourced assemblies discovered both sources depended on the same upstream node. Dual sourcing works best when combined with sub-tier visibility, constraint mapping, and engineering strategies that pre-qualify alternative materials and components.

How much does dual sourcing typically cost a Tier 1 automotive supplier?

The backup source typically charges a 10-20% premium due to lower volume allocation. Most Tier 1s use a 70/30 or 80/20 split, with the secondary source needing at least 20-30% of total volume to remain commercially viable. Additional costs include duplicate tooling (which can range from hundreds of thousands to millions for specialty parts), quality management overhead, and PPAP validation. For highly specialized components with expensive dedicated tooling, dual sourcing may be economically impossible at current Tier 1 margins of ~5.7% EBIT.

How are 2026 tariffs affecting Tier 1 supplier sourcing strategies?

U.S. import tariffs average 16% -- the highest since the 1930s -- with 48% on Chinese goods and 25% Section 232 duties on auto parts. The combined industry impact is estimated at $85 billion annually. Tariffs have become the number-one cost driver, cited by 45% of supplier executives. Many Tier 1s are nearshoring to Mexico, but the 2026 USMCA review creates uncertainty about whether those investments will continue to qualify for duty-free treatment. Tariffs are also accelerating sub-tier consolidation as smaller Tier 2/3 suppliers can't absorb the cost increases.

What should a Tier 1 supplier do first to improve real supply chain resilience?

Start by identifying line-stopper parts -- the components that stop customer production regardless of cost, not just the highest-spend items. Then map the true upstream constraints: sub-tier suppliers, manufacturing sites, raw material inputs, semiconductor fabs, and qualification paths. Apply the "same phone call" test: if both of your suppliers would call the same sub-tier during a crisis, you don't have independent recovery paths. From there, prioritize engineering pre-qualification of alternatives, sub-tier financial health monitoring, and scenario modeling that connects tariff exposure to sourcing decisions.

Every Tier 1 supplier I talk to has the same line item on their 2026 strategic plan: dual-source critical components. After the semiconductor crisis, the Renesas fire, the Ukraine wire harness shutdown, and now the Jubail petrochemical attack, the logic feels obvious. Two sources are better than one. Spread the risk. Multi-sourcing as insurance policy.

The problem is that dual sourcing -- the way most Tier 1s are implementing it -- solves the wrong layer of the problem.

Let's say you're a mid-size Tier 1 building seat electronics assemblies. You have two contract manufacturers. One in Malaysia, one in Mexico. The second source costs more, but procurement did the right thing: kept it warm with 25% of the volume, ran PPAP, duplicated tooling. Then a resin plant three tiers upstream goes down. Both of your suppliers call within 48 hours. Different EMS sites, different freight lanes, different account managers -- but both of them buy PCB laminates from the same material supplier, who buys PPE resin from the same Saudi petrochemical complex.

On paper, you had two sources. In the real network, you had one choke point.

The 2026 tariff environment is making this convergence worse, not better. With U.S. average tariffs at their highest level since the 1930s and sub-tier suppliers consolidating under margin pressure, the industry is concentrating its upstream dependencies at the exact moment when diversification matters most.

What Dual Sourcing Actually Costs

The economics of dual sourcing aren't complicated. They're just unfriendly to a Tier 1 running on mid-single-digit margins.

BCG's 2026 Global Automotive Supplier Study puts the average Tier 1 EBIT margin at 5.7%. OEMs are simultaneously pushing price-downs -- not just annually anymore, but quarterly in some programs. Tariffs have displaced raw materials as the number-one cost driver, cited by 45% of supplier executives in the most recent Automotive Logistics survey versus 42% for raw materials. Against that backdrop, every dollar spent on resilience competes with every other use of capital. The total cost of ownership calculation now includes risk.

A secondary source typically charges a 10-20% premium over your primary supplier. That's structural, not exploitative -- a supplier receiving 25% of your demand can't match the unit cost of one receiving 75%. One European electronics supplier documented the math after shifting to a 75/25 split: the backup vendor charged roughly 15% more per PCB. The annual cost increase was meaningful -- but less than the EUR 1.8 million in lost margin from an 8-week outage the previous year. The extra sourcing costs amortized in three years.

The harder constraint is CapEx. Dual sourcing commodity stampings or injection-molded parts is manageable. Dual sourcing a specialty die-cast housing, a custom ASIC, or a high-pressure fuel rail with $2-5 million in dedicated tooling? The economics often break. When tooling costs are that high, splitting volume may be economically impossible at current margins.

The practical consensus among Tier 1 procurement teams in 2026 is a 70/30 or 80/20 volume split, with a minimum of 20-30% allocated to the secondary source. Anything less is theater. A supplier receiving 2% of your demand won't prioritize you in a crisis -- they'll serve their 30% customers first. It's not on the approved vendor list if it can't actually show up.

The counterargument to "dual source everything" is strongest here: most Tier 1s can't afford it across the full BOM, and they shouldn't try. A seat frame bracket, a decorative plastic trim, and a safety-critical ECU don't deserve the same treatment. The sourcing strategy has to start with revenue-at-risk and lead time to recover, not just annual spend. A $6 sensor with a 9-month qualification path carries more risk than a $300 assembly with five qualified suppliers.

If your should-cost model doesn't include a resilience premium -- treating the 10-20% backup source cost as insurance against multi-million-dollar shutdowns -- your landed cost calculations are incomplete. And in 2026, landed cost that doesn't factor in tariff scenarios, HTS classification, and duty drawback eligibility isn't landed cost. It's a guess.

The Convergence Illusion

Here's the part that should keep you up at night. Even the components you've successfully dual-sourced may not actually be diversified.

A McKinsey study found that in a typical automotive supply chain, a single Tier 2 supplier serves an average of 14 different Tier 1 suppliers to the same OEM. Fourteen. When that shared Tier 2 goes down, your OEM customer doesn't lose one supply path -- they lose fourteen simultaneously. Your "backup" Tier 1 supplier was buying from the same upstream node you were.

The Deloitte CPO Survey puts the visibility problem in stark terms: only 15% of chief procurement officers have visibility beyond their Tier 1 suppliers. The other 85% are working from an incomplete map. They know who they buy from. They don't know who their suppliers buy from. And they definitely don't know where those supply chains converge three tiers deep.

This isn't abstract. Consider four convergence failures from the last 14 years, each one following the same pattern:

Evonik PA12 shortage, 2012. An explosion at Evonik's chemical plant in Marl, Germany disrupted production of cyclododecatriene -- a precursor for PA12 nylon used in automotive fuel lines, brake lines, and under-hood applications. The incident forced OEMs and Tier 1s into industry-wide scrambles for substitute materials. The constraint wasn't a Tier 1 assembly plant. It was a chemical input several steps upstream that most procurement teams had never mapped.

Renesas fire, March 2021. Renesas Electronics supplies roughly 30% of the global automotive microcontroller market. A fire at their Naka fab destroyed 23 manufacturing machines -- about 4% of the plant's equipment. Recovery took more than three months. Toyota, Nissan, Honda, and virtually every major OEM cut production. The total industry cost: an estimated $210 billion in lost automotive revenue and 12 million vehicles removed from global production in 2021-2022. Every Tier 1 ECU supplier, regardless of whether they had "dual sourced" their module production, traced back to the same handful of fabs.

Ukrainian neon, 2022. Two companies -- Ingas in Mariupol and Cryoin in Odesa -- produced 45-54% of the world's semiconductor-grade neon, a gas required for the laser lithography that makes every advanced chip. When Russia's invasion shut both facilities, neon prices quadrupled within weeks. Most Tier 1 buyers weren't sourcing neon -- they were sourcing ECUs, sensors, and power modules. But the chip fabs behind those components all depended on the same gas supply. The connection between "neon from a steel mill in Mariupol" and "my seat module supplier can't deliver" was invisible to most BOM cost management systems until it was too late.

Jubail petrochemical attack, April 2026. A missile strike hit the SABIC complex in Jubail, Saudi Arabia -- which produces approximately 70% of the world's high-purity PPE resin, a critical substrate for PCB laminates. Production halted. Within days, electronics and automotive suppliers globally faced severe PCB material shortages. This was a Tier 3 or Tier 4 input that most procurement teams had never mapped. The downstream effects are still rippling through global supply chains as of this writing.

The pattern is consistent: disruption doesn't hit where you're looking. It hits two or three tiers below your line of sight, at a convergence point you didn't know existed.

A useful test -- call it the "same phone call" test -- is simple: if Supplier A and Supplier B would both call the same sub-tier during a crisis, you do not have independent recovery paths. For each critical part, ask four questions:

Do our two suppliers share the same parent company, financial sponsor, or major sub-tier?

Do they depend on the same manufacturing site, even through different invoicing entities?

Do they rely on the same constrained input -- resin, gas, wafer capacity, specialty steel, plating chemistry?

Would a substitution still require months of requalification regardless of source count?

If any answer is yes, you may still want both suppliers. But you shouldn't call it a fully resilient design.

The Tariff Accelerant

The 2026 tariff environment isn't just adding cost. It's actively concentrating sub-tier supply chains.

The numbers are stark. BCG reports U.S. average trade-weighted tariffs at roughly 16% -- the highest since the Smoot-Hawley era of the 1930s. Effective tariffs on Chinese imports average 48%. Section 232 duties impose 25% on imported vehicles and auto parts. The combined impact: an estimated $85 billion in additional annual costs across the industry.

For Tier 1 suppliers, these tariffs create a three-way squeeze. First, direct cost increases on imported components. Second, OEM pressure to absorb those increases. Third -- and this is the one that gets less attention -- the downstream effects on your sub-tier suppliers.

Smaller Tier 2 and Tier 3 suppliers don't have the balance sheets to absorb a 25% tariff spike. Many can't invest in the compliance systems required for HTS classification and tariff drawback programs. The result is consolidation. Global automotive supplier M&A hit $35 billion in the first nine months of 2025, with average deal values doubling to $1.2 billion versus 2023. Liquidity pressure is pushing smaller sub-tier suppliers toward restructuring or acquisition.

Every acquisition that removes a sub-tier supplier from the market increases concentration risk. If your two "diversified" sources for a machined housing both relied on the same small Tier 3 heat-treatment shop, and that shop gets acquired by a larger player who rationalizes capacity -- your diversification just evaporated.

The automation gap compounds the problem. OEMs and Tier 1s invest adequately in robotics at rates of 51-62%. At Tier 2, that drops to 31%. At Tier 3, it's 23%. The suppliers most vulnerable to tariff-driven cost pressure are also the least equipped to adapt.

And there's a new bottleneck emerging from outside automotive entirely: DRAM. AI data center demand is pulling enormous memory capacity into servers. Vehicles are adding more memory content through ADAS, infotainment, and connected features. Even a Tier 1 with strong MCU supplier relationships may face allocation on memory because the shortage is driven by a different end market. The auto industry sometimes assumes its importance gives it priority. At data center margins, that assumption doesn't hold.

The USMCA Wild Card

Layered on top of the tariff environment is the USMCA six-year review, due by mid-2026. The agreement enables $1.6 trillion in annual North American trilateral trade -- including the deeply integrated automotive supply chain where parts cross the U.S., Mexico, and Canada borders multiple times before final assembly.

The U.S. administration has signaled it will seek tighter rules, potentially higher regional value content thresholds beyond the current 75% for vehicles, and has floated the possibility of replacing the trilateral agreement with bilateral deals. Canada's trade minister Dominic LeBlanc warned that the review uncertainty alone is causing a "break in investment decisions" -- net business investment in Canada is down as companies hesitate to build capacity without knowing the future tariff landscape.

For a Tier 1 trying to nearshore supply into Mexico to dodge Section 232 tariffs, the USMCA review injects a second layer of uncertainty. You're moving supply chains to qualify for trade rules that might change within 18 months. And despite tariff pressure, only about 36% of companies are actively reshoring production to the U.S. The majority are nearshoring selectively, going further offshore, or simply waiting.

The critical nuance: "local" is not the same as "resilient." A local supplier can still be financially weak. A regional source can still depend on a single imported material. A tariff-friendly supplier can still create a new concentration risk if every Tier 1 in the region is onboarding them simultaneously.

What Real Resilience Requires

Dual sourcing is a necessary component of resilience. It's not sufficient. The Tier 1s that are genuinely resilient -- not just checking a box for OEM compliance -- share five characteristics:

1. They map constraints, not just suppliers. For each critical component, they identify the true constraint layer: manufacturing site, parent company, critical sub-tier, raw material input, semiconductor fab, tooling location, qualification path, and tariff exposure. The point isn't to map the entire world. It's to find the few places where apparent options collapse into one dependency. Supplier performance management that stops at OTIF and PPM is looking at history. Constraint mapping tells you what happens when a hidden node fails tomorrow.

2. They prioritize by line-stopper risk, not annual spend. A $2 connector with no substitute and a 9-month requalification path carries more risk than a $300 assembly with five qualified sources. The first cut should be: which parts stop customer production? Overlay revenue-at-risk, customer penalty exposure, and time-to-recover before overlay spend.

3. They use engineering as a sourcing lever. Pre-qualifying pin-compatible MCUs, maintaining approved alternate resins, documenting firmware impacts before a crisis -- these engineering decisions determine whether procurement has options later. This isn't procurement telling engineering how to design. It's bringing supply reality into design reviews early enough to matter.

4. They monitor sub-tier financial health. The next disruption may not be a fire or a missile. It may be a Tier 3 supplier quietly going bankrupt because they can't absorb the tariff increase. Monitoring credit ratings, payment patterns, and revenue concentration at Tier 2 and Tier 3 gives lead time to qualify alternatives before the failure reaches your line.

5. They model scenarios, not just suppliers. What happens if a key resin is allocated at 50% for six weeks? What if Section 232 duties hit this assembly and the customer refuses a price adjustment? What if USMCA rules of origin change for this program? The Tier 1s with real resilience can answer these questions before the scenario becomes reality -- because they've connected RFQs, BOMs, supplier data, cost breakdowns, and tariff exposure in one system rather than six spreadsheets.

LightSource works with manufacturers building exactly this kind of connected view -- linking engineering specs, procurement decisions, supplier quotes, and cost data so teams can see how sourcing choices affect both cost and supply exposure at the part and program level. The practical value isn't a dashboard. It's being able to compare sourcing options against tariff scenarios and concentration risk before a decision hardens.

The Hard Math

The average Tier 1 automotive supplier in 2026 is caught between competing demands. OEMs want dual sourcing. Margins can't fund it everywhere. Tariffs are rising. Sub-tier suppliers are consolidating. The USMCA review might rewrite North American trade rules. And the next chip bottleneck may come from AI data center demand, not automotive.

There's no version of this where resilience is free. The question is whether you spend the money on the right risks. Dual sourcing your commodity parts is table stakes. The harder, more valuable work is mapping sub-tier convergence points, monitoring the financial health of concentrated suppliers you can't easily replace, using engineering to pre-qualify alternate materials and components, and building cost models that treat tariff volatility and disruption probability as inputs rather than surprises.

The 2026 Working Relations Index showed OEM-supplier relationships improving for the first time in 26 years. That matters -- because the Tier 1s that can have honest conversations with their OEM customers about the cost of resilience will be better positioned than those that absorb it silently. But the relationships that matter most for resilience aren't between OEMs and Tier 1s. They're between Tier 1s and the Tier 2s and Tier 3s that the industry still can't see.

Sources

BCG 2026 Global Automotive Supplier Study -- supplier margin data (5.7% EBIT), tariff impact analysis, U.S. average tariff at 16%

KPMG: Beyond Tier 1 -- A New Playbook for Multi-Tier Supplier Risk -- sub-tier visibility framework, risk categories, seat manufacturer example

Moody's: Hidden Semiconductor Risks in Automotive Supply Chains -- Tier 2/3 concentration data, $210B lost revenue estimate, 12M vehicles removed from production

Automotive Logistics: Supply Chains Redesigned Amid Disruptions -- tariffs as #1 cost driver (45%), reshoring data (36% active), automation gap by tier

AP News: USMCA 2026 Review -- Canadian trade minister on investment uncertainty, $1.6T trilateral trade

AP News: U.S.-China Tariff Levels -- effective tariffs on Chinese imports at 48%, China's share of U.S. trade from 13% to 6%

Tom's Hardware: Jubail PCB Resin Attack -- SABIC complex producing 70% of global PPE resin

Reuters/Investing.com: Ukraine Neon Disruption -- 45-54% of semiconductor-grade neon, 4x price spike

Kloepfel Consulting: Single vs. Multiple Sourcing 2026 -- dual sourcing cost premiums (15% example), volume split best practices, 3-year amortization

PwC: Section 232 Auto Tariffs -- tariff compliance framework, supplier offset mechanisms

Embedded Computing: Renesas Fire Analysis -- 30% automotive MCU market share, 3-month recovery, production cuts at Toyota/Nissan

Frequently Asked Questions

What is sub-tier convergence in automotive supply chains?

Sub-tier convergence happens when multiple direct suppliers depend on the same upstream supplier, facility, material, or process. A Tier 1 may have two qualified suppliers on paper, but both may rely on the same semiconductor fab, resin plant, specialty gas source, or tooling provider. McKinsey found that a single Tier 2 supplier serves an average of 14 different Tier 1s to the same OEM -- meaning a failure at that convergence point cascades across the entire supply network simultaneously.

Why isn't dual sourcing enough to protect against supply chain disruptions?

Dual sourcing reduces risk at the direct supplier level but doesn't guarantee independence deeper in the network. The Renesas fire, Ukrainian neon disruption, and Jubail petrochemical attack all followed the same pattern: Tier 1s with dual-sourced assemblies discovered both sources depended on the same upstream node. Dual sourcing works best when combined with sub-tier visibility, constraint mapping, and engineering strategies that pre-qualify alternative materials and components.

How much does dual sourcing typically cost a Tier 1 automotive supplier?

The backup source typically charges a 10-20% premium due to lower volume allocation. Most Tier 1s use a 70/30 or 80/20 split, with the secondary source needing at least 20-30% of total volume to remain commercially viable. Additional costs include duplicate tooling (which can range from hundreds of thousands to millions for specialty parts), quality management overhead, and PPAP validation. For highly specialized components with expensive dedicated tooling, dual sourcing may be economically impossible at current Tier 1 margins of ~5.7% EBIT.

How are 2026 tariffs affecting Tier 1 supplier sourcing strategies?

U.S. import tariffs average 16% -- the highest since the 1930s -- with 48% on Chinese goods and 25% Section 232 duties on auto parts. The combined industry impact is estimated at $85 billion annually. Tariffs have become the number-one cost driver, cited by 45% of supplier executives. Many Tier 1s are nearshoring to Mexico, but the 2026 USMCA review creates uncertainty about whether those investments will continue to qualify for duty-free treatment. Tariffs are also accelerating sub-tier consolidation as smaller Tier 2/3 suppliers can't absorb the cost increases.

What should a Tier 1 supplier do first to improve real supply chain resilience?

Start by identifying line-stopper parts -- the components that stop customer production regardless of cost, not just the highest-spend items. Then map the true upstream constraints: sub-tier suppliers, manufacturing sites, raw material inputs, semiconductor fabs, and qualification paths. Apply the "same phone call" test: if both of your suppliers would call the same sub-tier during a crisis, you don't have independent recovery paths. From there, prioritize engineering pre-qualification of alternatives, sub-tier financial health monitoring, and scenario modeling that connects tariff exposure to sourcing decisions.

Read more

Source Code Episode 9: Source Code: Shashi Mandapaty, Former Chief Procurement Officer at Johnson & Johnson, on Why One Throne Isn't Enough

Source Code Episode 8: Running on Paper: Rick McDonald, Chief Supply Chain Officer at Clorox, on Why Supplier Trust Is the Real Business Continuity Plan

The IEEPA Ruling Wasn't a Win. Here's What Procurement Leaders Are Missing.

Read more

Source Code Episode 9: Source Code: Shashi Mandapaty, Former Chief Procurement Officer at Johnson & Johnson, on Why One Throne Isn't Enough

Source Code Episode 8: Running on Paper: Rick McDonald, Chief Supply Chain Officer at Clorox, on Why Supplier Trust Is the Real Business Continuity Plan

The IEEPA Ruling Wasn't a Win. Here's What Procurement Leaders Are Missing.

Read more

Source Code Episode 9: Source Code: Shashi Mandapaty, Former Chief Procurement Officer at Johnson & Johnson, on Why One Throne Isn't Enough

Source Code Episode 8: Running on Paper: Rick McDonald, Chief Supply Chain Officer at Clorox, on Why Supplier Trust Is the Real Business Continuity Plan

The IEEPA Ruling Wasn't a Win. Here's What Procurement Leaders Are Missing.

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Trusted by:

Trusted by:

Trusted by:

*GARTNER is a registered trademark and service mark of Gartner, Inc. and/or its affiliates in the U.S. and internationally, and COOL VENDORS is a registered trademark of Gartner, Inc. and/or its affiliates and are used herein with permission. All rights reserved. Gartner does not endorse any vendor, product or service depicted in its research publications, and does not advise technology users to select only those vendors with the highest ratings or other designation. Gartner research publications consist of the opinions of Gartner’s research organization and should not be construed as statements of fact. Gartner disclaims all warranties, expressed or implied, with respect to this research, including any warranties of merchantability or fitness for a particular purpose.