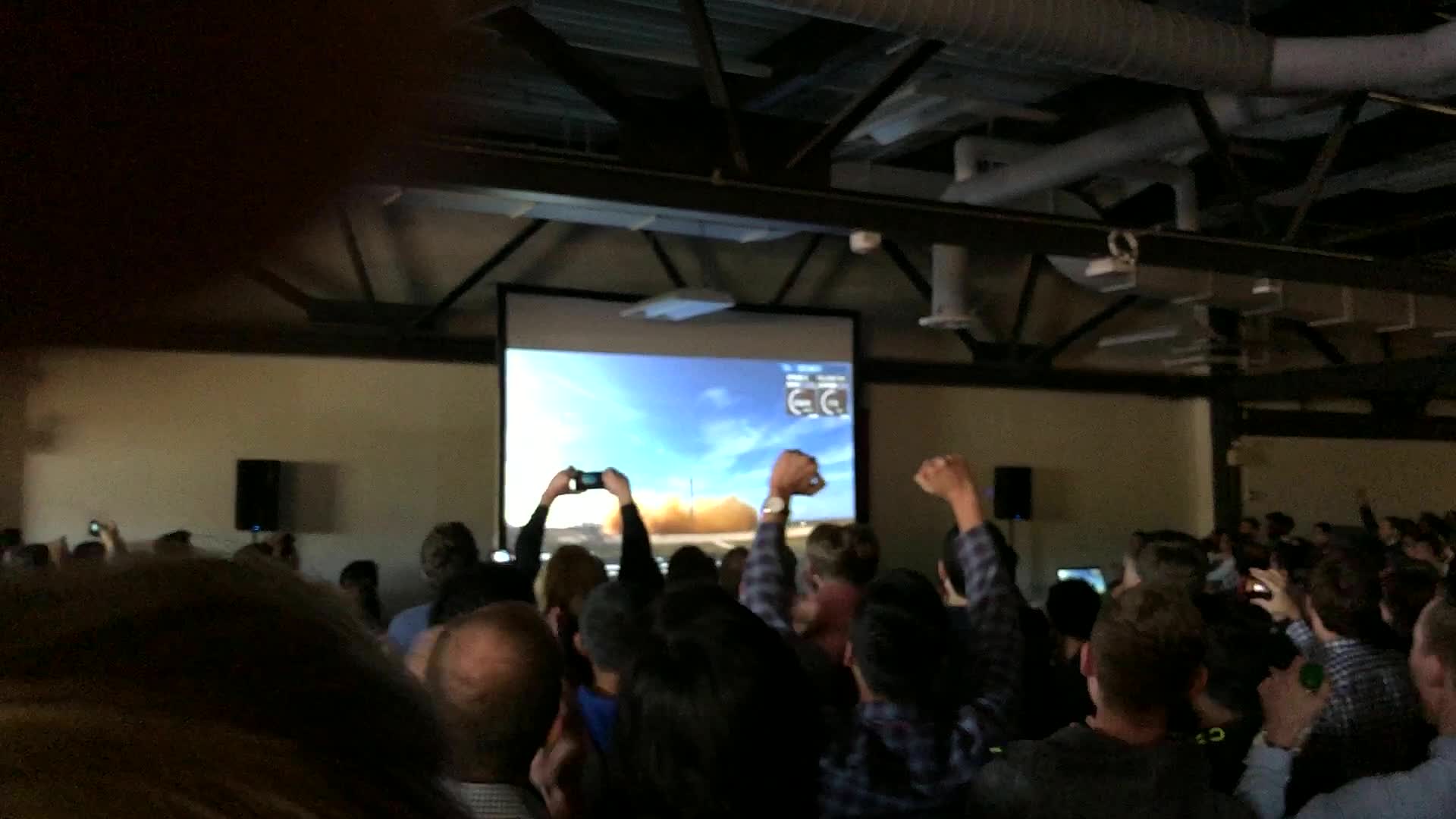

On February 6, 2018, a few hundred of us crowded into the lobby of Tesla's engineering R&D headquarters in Palo Alto to watch a rocket launch that had nothing to do with our day jobs. SpaceX was about to fly its Falcon Heavy for the first time, and the payload bolted to the top of the rocket was one of ours: a cherry-red Tesla Roadster, with a spacesuited mannequin named Starman in the driver's seat, "DON'T PANIC" on the dash, and David Bowie playing under the broadcast.

Tesla was already an intense place, and people did not stop work lightly. But when the two Falcon Heavy side boosters came down in perfect synchrony at Landing Zones 1 and 2 at Cape Canaveral, the room broke open. Phones went up, people climbed onto chairs, and a crowd of engineers who spent their days fighting millimeters and thermal budgets and supplier tooling sat watching a sports car leave Earth on the most visually absurd demonstration flight anyone had ever approved. I have been in a lot of rooms full of engineers, and I have never been in one quite like that.

The lobby of Tesla's engineering R&D headquarters as Falcon Heavy climbed out, February 6, 2018. Author's photo.

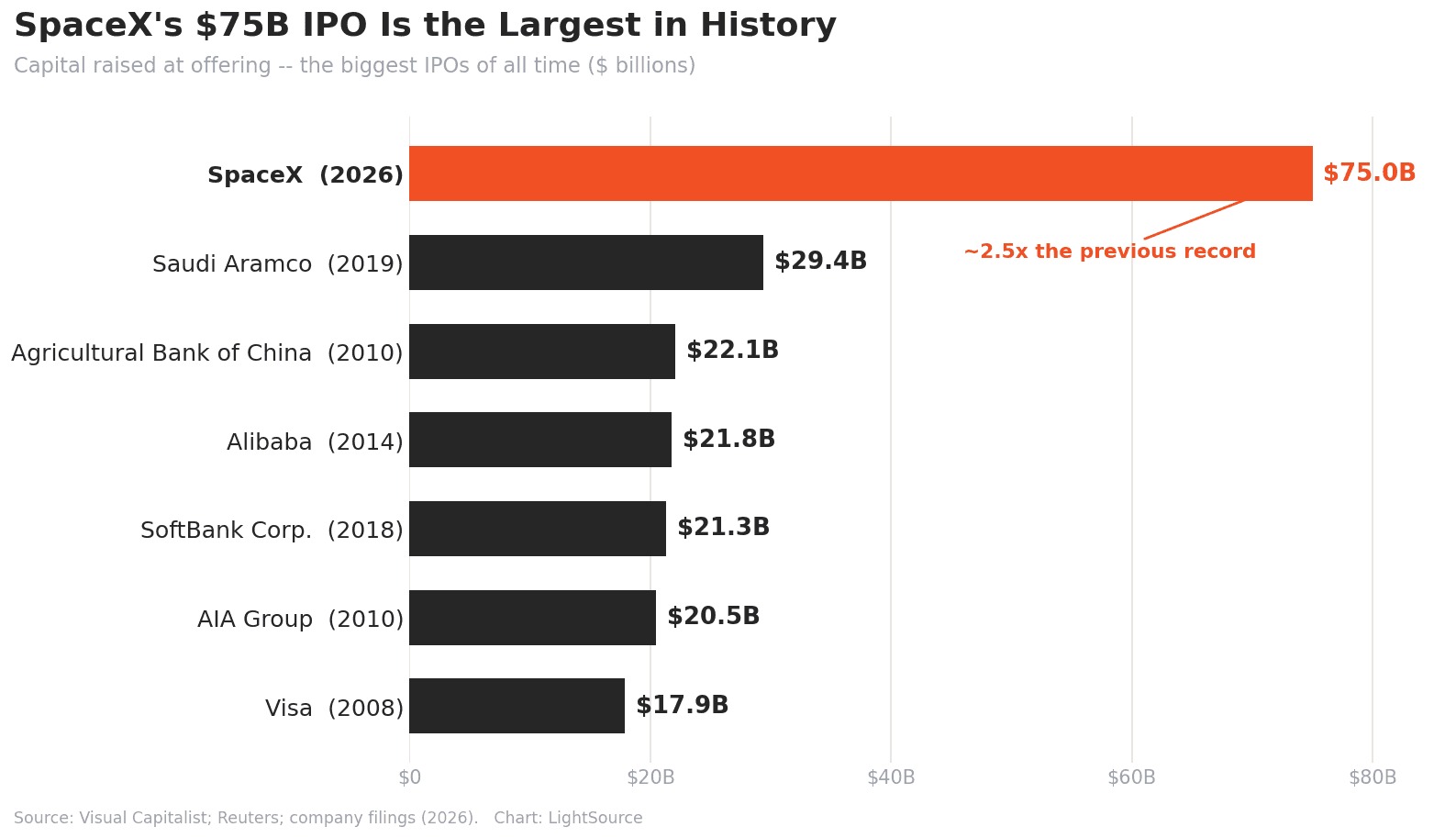

This week, eight years later, the market put a price on what that room felt. SpaceX priced its initial public offering at $135 a share, sold about 555 million shares, and raised roughly $75 billion, the largest IPO in history by a wide margin and around 2.5 times the $29.4 billion Saudi Aramco raised in 2019. It opened on the Nasdaq under the ticker SPCX, closed its first day up 19%, and by this week was trading near $206, a valuation north of $2 trillion. On paper it made Elon Musk the world's first trillionaire.

The number is staggering, but the thing I keep coming back to is what investors agreed to in order to pay it. They bought a company whose founder holds about 82% of the voting power and cannot, in any practical sense, be removed. In most public companies that would be a reason to pay less. At SpaceX it may be part of what they were paying for.

The trait is resistance to influence

Elon is usually described as a once-in-a-generation salesman, the person who can will capital and talent into existence by force of conviction. That is real, but I think it is the less important half of the story. Plenty of founders can raise money, recruit good engineers, and get a room excited. The rarer thing, and the one that actually separates him, is the ability to stay unmoved when credible, qualified people tell him his plan is impossible, impractical, irresponsible, or embarrassing.

Almost everything we did at Tesla, and almost everything the team did at SpaceX, was at the time considered one of those things by people who were, on paper, better positioned to judge. A reusable orbital rocket. A mass-market electric car from a company that had never mass-produced anything. The consensus against these ideas was neither quiet nor stupid; it was grounded in decades of experience. What the work required was the ability to take all of that in and still decide to go.

The resistance runs deeper than ignoring outside critics. Standing in front of SpaceX employees in Texas this month, minutes before he rang the opening bell, Musk said he had given the company "less than a 10% chance of succeeding at all" when he started it, and that he had told people so at the time. His own expected-value math said the rational move was not to try, and he tried anyway. George Bernard Shaw described the type in 1903: "The reasonable man adapts himself to the world; the unreasonable one persists in trying to adapt the world to himself. Therefore all progress depends on the unreasonable man." Musk is, in that specific sense, one of the most unreasonable people alive, and the trait carries a cost I will come back to.

The Falcon Heavy payload is the clearest example I can point to. Strapping your own sports car to the most powerful operational rocket in the world, putting a dummy in a spacesuit behind the wheel, cueing up Bowie, and aiming the whole thing past Mars is not a decision that survives a serious meeting. At Boeing, at Lockheed, at almost any public-company boardroom, the Roadster dies in the first review. Payload review asks for the business case, legal asks about reputational downside, communications asks whether it makes the company look unserious, and finance asks why a test flight needs a cultural artifact. Each objection is reasonable on its own, and together they add up to a no. Most organizations do not kill strange ideas because the people inside them lack imagination. They kill them because every function holds a legitimate veto, and the safest answer is the one nobody will have to defend later.

Two kinds of influence, and most companies confuse them

The usable lesson is narrower than "ignore people," which is both crude and usually wrong. The distinction that matters is between influence on the goal and influence on the execution, and most companies get the two backwards.

On execution, Elon's companies are relentlessly empirical. A rocket either lands or it does not. A battery pack either meets its cost, density, safety, and cycle-life targets or it does not. A supplier either makes the date or it does not. At Tesla a design review could be reduced to mass, cost, thermal performance, manufacturability, and schedule very quickly, and vague confidence did not last long against the numbers. On goals he is nearly immovable. Reusable rockets should exist; electric cars should be mass-market products; a private company should be able to fly NASA astronauts. None of that softened because incumbents found it naive.

Most companies run the opposite way. They accept influence on the goal, letting consensus quietly shrink the ambition, and then they resist influence on the execution, defending the original plan long after the facts have changed. Protecting the goal while staying honest about the plan is the harder discipline, and it is rare. Reusability is the clearest case. In 2014, NASA and France's CNES were openly skeptical that SpaceX could ever make booster recovery economical, and Stanford's Scott Hubbard called reusability "a holy grail," a phrase that captured how long the field had wanted it and how hard it had proven. Musk's response amounted to a should-cost analysis run at the scale of an industry: a rocket is aluminum-lithium, carbon fiber, titanium, copper, avionics, engines, and propellant, and he has said the raw materials run on the order of 2% of the traditional launch price. If that is even directionally true, the question stops being why rockets are expensive and becomes which part of the cost is physics and which part is markup, risk posture, and inherited practice. The same move underpins serious cost-down work in any industry. He resisted the conclusion, not the engineering.

An honest ledger: four misses for every world-changing six

Roughly four of every ten things these companies attempt fail outright or slip by years. I do not read that as an embarrassment so much as the price of the strategy, and admirers and critics both tend to misunderstand it.

The misses are real and worth listing plainly. Hyperloop has no working commercial system more than a decade after the proposal. The Cybertruck arrived years late, missed its original $40,000 price, and has had recalls. Full Self-Driving was promised at Level 5 on timelines that did not hold, and as of last year was still a supervised Level 2 system. Humans were supposed to be on Mars by 2024, the realistic date is now 2028 at the earliest, and Starship has spent years turning test articles into fireballs. Measured only on whether he hits the dates he announces, Musk is unreliable, and the people who say so are correct.

The wins sit on the other side of the same ledger. Reusable boosters were a fantasy until a Falcon 9 landed back at Cape Canaveral in December 2015, and by 2022 NASA's own science chief was saying he preferred to fly on flight-proven boosters, a full reversal of the 2014 consensus. SpaceX now puts more mass into orbit than every other provider on Earth combined. Crew Dragon returned human spaceflight to American soil in 2020. Starlink put working internet over places that had never had it. At Tesla, the Model 3 ramp that Musk called "production hell" drew a Moody's downgrade to junk in March 2018 and a public prediction from former GM vice-chairman Bob Lutz that the company was "headed for the graveyard," and it went on to become the best-selling electric car in the world.

What makes the trade worth taking has little to do with the hit rate and a lot to do with the shape of the payoffs. The downside of an unreasonable bet is bounded, and the upside is not. A failed Hyperloop costs a white paper and some embarrassment, while a working reusable rocket permanently lowers the cost of reaching orbit for everyone who comes after it. If four bets in ten fail and six change the world, the math favors making the bet, as long as you can survive the four. Most people and most companies cannot survive the four, financially or reputationally, and that is the real reason most of them never make it. The same logic ran through the best wartime production programs and through the challengers trying to develop on China-time cycles today, where the willingness to attempt the inadvisable, quickly, is the edge.

Starman and the Roadster on the live feed, watched from the Tesla lobby. Author's photo.

Why the misses don't sink the company

What turns all of this into value instead of wreckage is that the misses are built to be survivable, and that is the part the mythology tends to flatten.

Falcon Heavy's first flight shows it well, because even the triumph contained a failure. The side boosters landed together and produced one of the most memorable aerospace images of the decade. The center core did not. It ran low on TEA-TEB igniter fluid, relit only one of three engines, missed the drone ship Of Course I Still Love You, and hit the Atlantic at about 300 miles per hour roughly 100 meters away, throwing shrapnel across the deck and knocking out two of the ship's thrusters. The most iconic launch of the decade still missed a third of its landing. A clean retelling leaves that out, but the failure is the instructive part, because the mission was structured so that it did not erase the learning or the narrative. The side boosters proved one thing, the payload proved another, and the center core produced a specific failure mode and a list of fixes. The failure was not avoided so much as contained, made specific, and paid for by the parts that worked.

Convexity like that is easy to claim and hard to earn. "We take big swings" is not a strategy, and a big swing with no instrumentation is just a gamble. A big swing with staged tests, clear failure modes, fast supplier response, and a balance sheet that can absorb the loss is a different thing, and SpaceX nearly proved the fatal version of it firsthand. Falcon 1 failed three times before its fourth flight reached orbit on September 28, 2008, with the company almost out of money, and weeks later NASA's commercial cargo contract, worth about $1.6 billion, changed its survival math. That contract did not make the engineering any easier, but it kept the company alive long enough to keep taking shots. The unreasonable founder matters, and so do the contracts, customers, engineers, and suppliers who keep the system solvent long enough for the unreasonable bet to be tested. SpaceX's president, Gwynne Shotwell, is widely credited with talking Musk out of his least workable deadlines, and Musk himself eventually conceded that the heavy automation at Tesla had been a mistake and that he had underrated the people on the line. Resisting influence on the goal is necessary, but on its own it is not enough, and it is never free.

What investors were actually buying

SpaceX did not go public the way most companies do. It listed with a dual-class structure in which Class B shares carry ten votes each. According to the S-1, Musk holds roughly 42% of the equity but about 82% of the voting power, and he can be removed only by a vote he himself controls. For practical purposes, he is not removable.

Most of the machinery of a public company exists to prevent exactly that situation. Boards, independent directors, shareholder votes, and the rest are there to constrain the chief executive and to protect investors from one person's mistakes. Governance specialists looked at the SpaceX offering and saw that machinery missing. Harvard Law School's corporate governance forum analyzed it under the headline "Top IPO, Weak Governance," research from the European Corporate Governance Institute finds that the valuation premium on dual-class firms tends to decay into a discount seven to nine years after listing, and the S&P 500 stopped admitting new dual-class companies back in 2017 for this reason. The concerns are legitimate, and concentrated control genuinely does reduce accountability and create key-person risk.

The complication is that the same control is where the company's ambition comes from. The reusable rockets, the Roadster, the refusal to treat the launch industry's cost structure as fixed, all of it grew out of one person being able to overrule the people who would have said no. The thing the governance machinery is built to prevent is, in this case, the thing that built the company. So it is worth asking whether investors paid a near-$2 trillion valuation despite Musk's control or because of it. In most companies, oversight is the product on offer, the assurance that no single person can drive the whole enterprise into a wall. At SpaceX, the adventure is the product, and the adventure has only ever come from his hands being untied. Read that way, a valuation that high on a company whose founder cannot be removed looks less like a bet on an aerospace business and more like a bet on Elon himself, with his control treated as an asset rather than a discount.

There is some history behind that kind of bet. As a group, founder-led companies have earned a premium: an index of S&P 500 firms with active founders has beaten the rest by a factor of 3.1 over 15 years, and a Harvard Business Review analysis found founder-led firms returned 12% over three years against negative 26% for companies run by hired CEOs. The market has rewarded conviction-plus-control before. The catch is the one the ECGI data points to and the one every key-person discount is built around: you are betting that the person stays right, and that he stays at all. That is a different risk than most public investors are used to underwriting, and the SpaceX IPO is the largest version of it anyone has ever sold.

SpaceX's $75 billion raise dwarfs every prior IPO. Source: Visual Capitalist; Reuters; company filings (2026).

What this means if you're not Elon

"Resist all influence" is terrible advice for almost everyone, because most unreasonable bets really are wrong and most people pushing back on your idea are right. The usable version is narrower: build a way of working that sorts pushback into a few kinds and treats each differently.

Objections from physics deserve immediate respect, because if the thermal model says the pack will not survive the duty cycle, no amount of conviction changes that. Objections from economics deserve to be taken apart, because when a supplier quotes a part at $180 you need to know how much of that is material, cycle time, scrap, amortized tooling, margin, or risk premium, which is the daily work of should-cost and cost-down analysis. Objections from execution deserve a fast, cheap test rather than an argument, so if the team says a supplier cannot hit a date, run the tooling and the approval path to ground and shorten the loop between a decision and its result. Objections from convention deserve the most scrutiny of all, because "that is not how this is done" is sometimes hard-won wisdom and sometimes just inherited habit. Most of the skill is in telling those four apart.

This matters most for challengers. The larger incumbent has more capital, more suppliers, more installed process, and more people whose job is to prevent visible mistakes, and its one structural disadvantage is cycle time. A smaller company can decide on Monday, see supplier feedback on Wednesday, and change the design before the incumbent has finished routing the first approval. That is the same edge operators carry when they move from automotive into aerospace and defense, and it is why manufacturing capability increasingly reads as a strategic weapon rather than a back office, something I have written about in the context of defense and the factory floor. At LightSource we work with these challenger manufacturers, the ones running new-product timelines that look impractical from the outside, and the job is to lower the cost of each shot so a team can take more of them without turning every miss into a crisis. You do not need 82% of the votes to hold a line against bad influence. You need conviction on the few things that matter and a cheap enough way to test everything else that missing four times in ten does not end you.

The lobby understood before the market did

What I remember most from that lobby is not the Roadster, though the image is hard to beat. It is the way the engineers reacted when the side boosters landed. Everyone in that room knew how unforgiving hardware is, how many ways a design fails between CAD and production, how one late supplier or one bad assumption about heat or vibration turns a clean plan into months of recovery. That is why the moment hit the way it did. It was not magic to them; it was the visible output of thousands of specific decisions that had somehow survived contact with reality.

The Roadster was impractical, and it was also exactly the kind of impractical decision that tells you how a company really thinks. A normal organization optimizes its demo payload for defensibility. SpaceX optimized it for meaning, contained the risk, and accepted that the center core might not come home. It didn't; the side boosters did; Starman went past Mars, where the Roadster still is, looping the sun about every 557 days. Eight years later the market bought that company at a valuation near $2 trillion while accepting that its founder cannot be removed, which is, when you strip it down, a wager on the same trait that filled that lobby with noise. Whether the wager pays still depends on the question that was already hanging in the room in 2018, before anyone had attached a number to it: whether the misses stay survivable long enough for the wins to compound.

Sources

SpaceX prices record IPO -- NPR on the $135 price and ~$75 billion raise, the largest in history.

SPCX jumps 19% on debut -- CNBC on first-day trading on the Nasdaq.

Ranked: the biggest IPOs in history, and where SpaceX fits -- Visual Capitalist's comparison with Aramco, Alibaba, and Visa.

How Musk increases his power through the IPO -- TechCrunch on the dual-class voting structure (~42% equity, ~82% of the vote).

Top IPO, Weak Governance -- Harvard Law School Forum on Corporate Governance on the offering's investor protections.

Musk gave SpaceX "less than a 10% chance of succeeding" -- Inc. on what Musk told employees before the opening bell.

First flight of the Falcon Heavy -- NASA's account of the February 6, 2018 demo and the Roadster payload.

Falcon Heavy center core toppled after landing -- SpaceNews on the center-core failure and the drone-ship damage.

Starman's first orbit of the sun -- Space.com on the Roadster's heliocentric, beyond-Mars trajectory.

NASA, France skeptical of SpaceX reusable rocket project -- contemporaneous expert doubt about reusability.

Why Musk wants employees to use first principles -- CNBC on the "2% of the cost is materials" reasoning.

Elon Musk's biggest broken promises -- a survey of missed timelines, from FSD to Mars.

From Meta to SpaceX: how dual-class shares keep founders in control -- U.S. News explainer on the structure and its track record.

Frequently Asked Questions

How big was the SpaceX IPO, and what is the ticker?

SpaceX raised about $75 billion in June 2026 at a valuation near $1.75 trillion, making it the largest initial public offering in history, roughly 2.5 times the $29.4 billion Saudi Aramco raised in 2019. It trades on the Nasdaq under the ticker SPCX and rose 19% on its first day.

Does Elon Musk still control SpaceX after it went public?

Yes. SpaceX listed with a dual-class structure in which Class B shares carry ten votes each. According to the company's filings, Musk holds roughly 42% of the equity but around 82% of the voting power, and he can be removed only through a vote he effectively controls. Public investors own the economics but have limited governance say.

What was the Tesla Roadster doing on the Falcon Heavy?

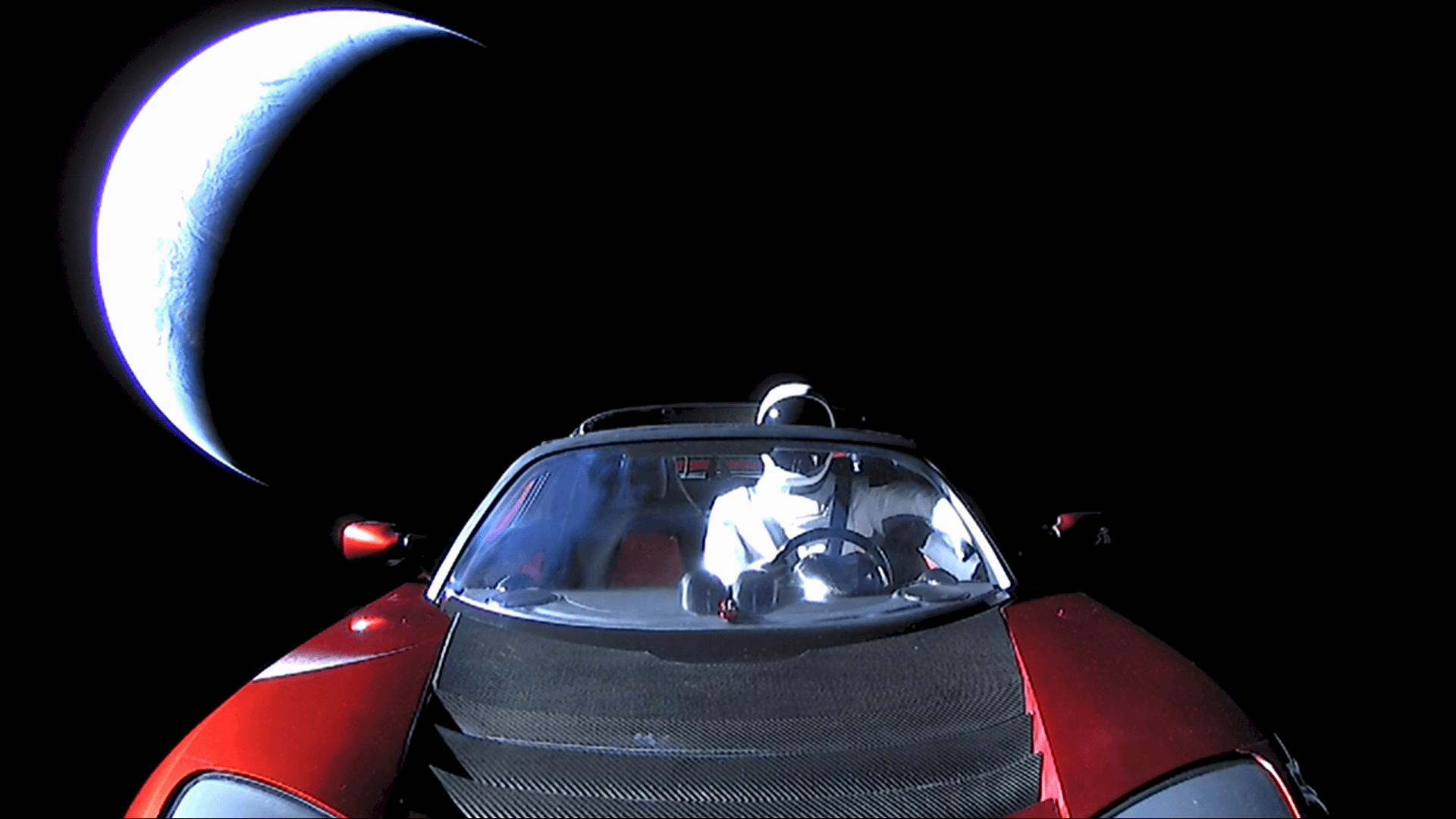

For Falcon Heavy's first test flight on February 6, 2018, SpaceX used Musk's personal cherry-red Tesla Roadster as the demonstration payload, with a spacesuited mannequin nicknamed "Starman" in the driver's seat and "DON'T PANIC" on the dashboard. It was sent into a heliocentric orbit that carries it out past Mars, and it is still in space today.

Did the first Falcon Heavy launch fully succeed?

Mostly, but not entirely. The two side boosters landed simultaneously at Cape Canaveral, but the center core ran low on igniter fluid, relit only one of three engines, and crashed into the ocean near the drone ship at about 300 miles per hour. The mission is remembered as a triumph, though it still missed one of its three planned landings, which is a fair reminder of the real success rate behind the headlines.

Why do founder-led companies like SpaceX tend to outperform?

Research suggests founder-led firms outperform partly because founders with strong control can resist the short-term, consensus-driven pressures that push hired CEOs toward safer choices. One index of S&P 500 companies with active founders beat the rest of the index 3.1 times over 15 years, and a Harvard Business Review study found founder-led firms returned 12% over three years versus negative 26% for non-founder CEOs. The same control that enables bold long-term bets also concentrates risk, which is why dual-class structures remain controversial.

What can operators learn from Musk without copying him?

The practical lesson is about sorting feedback rather than ignoring it. Objections about physics, economics, execution, and convention each deserve a different response: respect the physics, take the economics apart, test the execution quickly and cheaply, and reserve real skepticism for "that's not how it's done." Most companies are better served copying the discipline of fast, cheap learning than the personality or the governance structure.

On February 6, 2018, a few hundred of us crowded into the lobby of Tesla's engineering R&D headquarters in Palo Alto to watch a rocket launch that had nothing to do with our day jobs. SpaceX was about to fly its Falcon Heavy for the first time, and the payload bolted to the top of the rocket was one of ours: a cherry-red Tesla Roadster, with a spacesuited mannequin named Starman in the driver's seat, "DON'T PANIC" on the dash, and David Bowie playing under the broadcast.

Tesla was already an intense place, and people did not stop work lightly. But when the two Falcon Heavy side boosters came down in perfect synchrony at Landing Zones 1 and 2 at Cape Canaveral, the room broke open. Phones went up, people climbed onto chairs, and a crowd of engineers who spent their days fighting millimeters and thermal budgets and supplier tooling sat watching a sports car leave Earth on the most visually absurd demonstration flight anyone had ever approved. I have been in a lot of rooms full of engineers, and I have never been in one quite like that.

The lobby of Tesla's engineering R&D headquarters as Falcon Heavy climbed out, February 6, 2018. Author's photo.

This week, eight years later, the market put a price on what that room felt. SpaceX priced its initial public offering at $135 a share, sold about 555 million shares, and raised roughly $75 billion, the largest IPO in history by a wide margin and around 2.5 times the $29.4 billion Saudi Aramco raised in 2019. It opened on the Nasdaq under the ticker SPCX, closed its first day up 19%, and by this week was trading near $206, a valuation north of $2 trillion. On paper it made Elon Musk the world's first trillionaire.

The number is staggering, but the thing I keep coming back to is what investors agreed to in order to pay it. They bought a company whose founder holds about 82% of the voting power and cannot, in any practical sense, be removed. In most public companies that would be a reason to pay less. At SpaceX it may be part of what they were paying for.

The trait is resistance to influence

Elon is usually described as a once-in-a-generation salesman, the person who can will capital and talent into existence by force of conviction. That is real, but I think it is the less important half of the story. Plenty of founders can raise money, recruit good engineers, and get a room excited. The rarer thing, and the one that actually separates him, is the ability to stay unmoved when credible, qualified people tell him his plan is impossible, impractical, irresponsible, or embarrassing.

Almost everything we did at Tesla, and almost everything the team did at SpaceX, was at the time considered one of those things by people who were, on paper, better positioned to judge. A reusable orbital rocket. A mass-market electric car from a company that had never mass-produced anything. The consensus against these ideas was neither quiet nor stupid; it was grounded in decades of experience. What the work required was the ability to take all of that in and still decide to go.

The resistance runs deeper than ignoring outside critics. Standing in front of SpaceX employees in Texas this month, minutes before he rang the opening bell, Musk said he had given the company "less than a 10% chance of succeeding at all" when he started it, and that he had told people so at the time. His own expected-value math said the rational move was not to try, and he tried anyway. George Bernard Shaw described the type in 1903: "The reasonable man adapts himself to the world; the unreasonable one persists in trying to adapt the world to himself. Therefore all progress depends on the unreasonable man." Musk is, in that specific sense, one of the most unreasonable people alive, and the trait carries a cost I will come back to.

The Falcon Heavy payload is the clearest example I can point to. Strapping your own sports car to the most powerful operational rocket in the world, putting a dummy in a spacesuit behind the wheel, cueing up Bowie, and aiming the whole thing past Mars is not a decision that survives a serious meeting. At Boeing, at Lockheed, at almost any public-company boardroom, the Roadster dies in the first review. Payload review asks for the business case, legal asks about reputational downside, communications asks whether it makes the company look unserious, and finance asks why a test flight needs a cultural artifact. Each objection is reasonable on its own, and together they add up to a no. Most organizations do not kill strange ideas because the people inside them lack imagination. They kill them because every function holds a legitimate veto, and the safest answer is the one nobody will have to defend later.

Two kinds of influence, and most companies confuse them

The usable lesson is narrower than "ignore people," which is both crude and usually wrong. The distinction that matters is between influence on the goal and influence on the execution, and most companies get the two backwards.

On execution, Elon's companies are relentlessly empirical. A rocket either lands or it does not. A battery pack either meets its cost, density, safety, and cycle-life targets or it does not. A supplier either makes the date or it does not. At Tesla a design review could be reduced to mass, cost, thermal performance, manufacturability, and schedule very quickly, and vague confidence did not last long against the numbers. On goals he is nearly immovable. Reusable rockets should exist; electric cars should be mass-market products; a private company should be able to fly NASA astronauts. None of that softened because incumbents found it naive.

Most companies run the opposite way. They accept influence on the goal, letting consensus quietly shrink the ambition, and then they resist influence on the execution, defending the original plan long after the facts have changed. Protecting the goal while staying honest about the plan is the harder discipline, and it is rare. Reusability is the clearest case. In 2014, NASA and France's CNES were openly skeptical that SpaceX could ever make booster recovery economical, and Stanford's Scott Hubbard called reusability "a holy grail," a phrase that captured how long the field had wanted it and how hard it had proven. Musk's response amounted to a should-cost analysis run at the scale of an industry: a rocket is aluminum-lithium, carbon fiber, titanium, copper, avionics, engines, and propellant, and he has said the raw materials run on the order of 2% of the traditional launch price. If that is even directionally true, the question stops being why rockets are expensive and becomes which part of the cost is physics and which part is markup, risk posture, and inherited practice. The same move underpins serious cost-down work in any industry. He resisted the conclusion, not the engineering.

An honest ledger: four misses for every world-changing six

Roughly four of every ten things these companies attempt fail outright or slip by years. I do not read that as an embarrassment so much as the price of the strategy, and admirers and critics both tend to misunderstand it.

The misses are real and worth listing plainly. Hyperloop has no working commercial system more than a decade after the proposal. The Cybertruck arrived years late, missed its original $40,000 price, and has had recalls. Full Self-Driving was promised at Level 5 on timelines that did not hold, and as of last year was still a supervised Level 2 system. Humans were supposed to be on Mars by 2024, the realistic date is now 2028 at the earliest, and Starship has spent years turning test articles into fireballs. Measured only on whether he hits the dates he announces, Musk is unreliable, and the people who say so are correct.

The wins sit on the other side of the same ledger. Reusable boosters were a fantasy until a Falcon 9 landed back at Cape Canaveral in December 2015, and by 2022 NASA's own science chief was saying he preferred to fly on flight-proven boosters, a full reversal of the 2014 consensus. SpaceX now puts more mass into orbit than every other provider on Earth combined. Crew Dragon returned human spaceflight to American soil in 2020. Starlink put working internet over places that had never had it. At Tesla, the Model 3 ramp that Musk called "production hell" drew a Moody's downgrade to junk in March 2018 and a public prediction from former GM vice-chairman Bob Lutz that the company was "headed for the graveyard," and it went on to become the best-selling electric car in the world.

What makes the trade worth taking has little to do with the hit rate and a lot to do with the shape of the payoffs. The downside of an unreasonable bet is bounded, and the upside is not. A failed Hyperloop costs a white paper and some embarrassment, while a working reusable rocket permanently lowers the cost of reaching orbit for everyone who comes after it. If four bets in ten fail and six change the world, the math favors making the bet, as long as you can survive the four. Most people and most companies cannot survive the four, financially or reputationally, and that is the real reason most of them never make it. The same logic ran through the best wartime production programs and through the challengers trying to develop on China-time cycles today, where the willingness to attempt the inadvisable, quickly, is the edge.

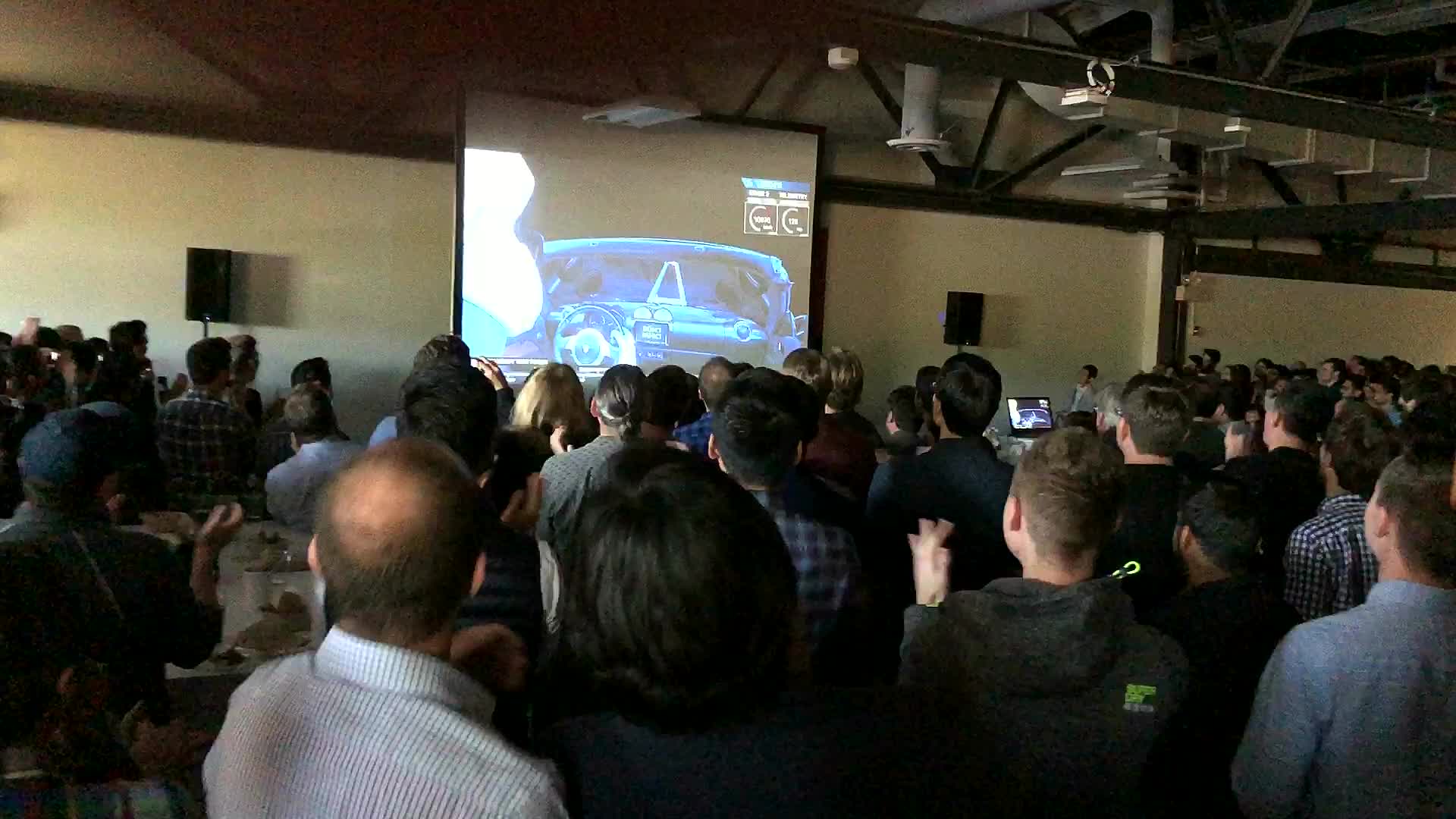

Starman and the Roadster on the live feed, watched from the Tesla lobby. Author's photo.

Why the misses don't sink the company

What turns all of this into value instead of wreckage is that the misses are built to be survivable, and that is the part the mythology tends to flatten.

Falcon Heavy's first flight shows it well, because even the triumph contained a failure. The side boosters landed together and produced one of the most memorable aerospace images of the decade. The center core did not. It ran low on TEA-TEB igniter fluid, relit only one of three engines, missed the drone ship Of Course I Still Love You, and hit the Atlantic at about 300 miles per hour roughly 100 meters away, throwing shrapnel across the deck and knocking out two of the ship's thrusters. The most iconic launch of the decade still missed a third of its landing. A clean retelling leaves that out, but the failure is the instructive part, because the mission was structured so that it did not erase the learning or the narrative. The side boosters proved one thing, the payload proved another, and the center core produced a specific failure mode and a list of fixes. The failure was not avoided so much as contained, made specific, and paid for by the parts that worked.

Convexity like that is easy to claim and hard to earn. "We take big swings" is not a strategy, and a big swing with no instrumentation is just a gamble. A big swing with staged tests, clear failure modes, fast supplier response, and a balance sheet that can absorb the loss is a different thing, and SpaceX nearly proved the fatal version of it firsthand. Falcon 1 failed three times before its fourth flight reached orbit on September 28, 2008, with the company almost out of money, and weeks later NASA's commercial cargo contract, worth about $1.6 billion, changed its survival math. That contract did not make the engineering any easier, but it kept the company alive long enough to keep taking shots. The unreasonable founder matters, and so do the contracts, customers, engineers, and suppliers who keep the system solvent long enough for the unreasonable bet to be tested. SpaceX's president, Gwynne Shotwell, is widely credited with talking Musk out of his least workable deadlines, and Musk himself eventually conceded that the heavy automation at Tesla had been a mistake and that he had underrated the people on the line. Resisting influence on the goal is necessary, but on its own it is not enough, and it is never free.

What investors were actually buying

SpaceX did not go public the way most companies do. It listed with a dual-class structure in which Class B shares carry ten votes each. According to the S-1, Musk holds roughly 42% of the equity but about 82% of the voting power, and he can be removed only by a vote he himself controls. For practical purposes, he is not removable.

Most of the machinery of a public company exists to prevent exactly that situation. Boards, independent directors, shareholder votes, and the rest are there to constrain the chief executive and to protect investors from one person's mistakes. Governance specialists looked at the SpaceX offering and saw that machinery missing. Harvard Law School's corporate governance forum analyzed it under the headline "Top IPO, Weak Governance," research from the European Corporate Governance Institute finds that the valuation premium on dual-class firms tends to decay into a discount seven to nine years after listing, and the S&P 500 stopped admitting new dual-class companies back in 2017 for this reason. The concerns are legitimate, and concentrated control genuinely does reduce accountability and create key-person risk.

The complication is that the same control is where the company's ambition comes from. The reusable rockets, the Roadster, the refusal to treat the launch industry's cost structure as fixed, all of it grew out of one person being able to overrule the people who would have said no. The thing the governance machinery is built to prevent is, in this case, the thing that built the company. So it is worth asking whether investors paid a near-$2 trillion valuation despite Musk's control or because of it. In most companies, oversight is the product on offer, the assurance that no single person can drive the whole enterprise into a wall. At SpaceX, the adventure is the product, and the adventure has only ever come from his hands being untied. Read that way, a valuation that high on a company whose founder cannot be removed looks less like a bet on an aerospace business and more like a bet on Elon himself, with his control treated as an asset rather than a discount.

There is some history behind that kind of bet. As a group, founder-led companies have earned a premium: an index of S&P 500 firms with active founders has beaten the rest by a factor of 3.1 over 15 years, and a Harvard Business Review analysis found founder-led firms returned 12% over three years against negative 26% for companies run by hired CEOs. The market has rewarded conviction-plus-control before. The catch is the one the ECGI data points to and the one every key-person discount is built around: you are betting that the person stays right, and that he stays at all. That is a different risk than most public investors are used to underwriting, and the SpaceX IPO is the largest version of it anyone has ever sold.

SpaceX's $75 billion raise dwarfs every prior IPO. Source: Visual Capitalist; Reuters; company filings (2026).

What this means if you're not Elon

"Resist all influence" is terrible advice for almost everyone, because most unreasonable bets really are wrong and most people pushing back on your idea are right. The usable version is narrower: build a way of working that sorts pushback into a few kinds and treats each differently.

Objections from physics deserve immediate respect, because if the thermal model says the pack will not survive the duty cycle, no amount of conviction changes that. Objections from economics deserve to be taken apart, because when a supplier quotes a part at $180 you need to know how much of that is material, cycle time, scrap, amortized tooling, margin, or risk premium, which is the daily work of should-cost and cost-down analysis. Objections from execution deserve a fast, cheap test rather than an argument, so if the team says a supplier cannot hit a date, run the tooling and the approval path to ground and shorten the loop between a decision and its result. Objections from convention deserve the most scrutiny of all, because "that is not how this is done" is sometimes hard-won wisdom and sometimes just inherited habit. Most of the skill is in telling those four apart.

This matters most for challengers. The larger incumbent has more capital, more suppliers, more installed process, and more people whose job is to prevent visible mistakes, and its one structural disadvantage is cycle time. A smaller company can decide on Monday, see supplier feedback on Wednesday, and change the design before the incumbent has finished routing the first approval. That is the same edge operators carry when they move from automotive into aerospace and defense, and it is why manufacturing capability increasingly reads as a strategic weapon rather than a back office, something I have written about in the context of defense and the factory floor. At LightSource we work with these challenger manufacturers, the ones running new-product timelines that look impractical from the outside, and the job is to lower the cost of each shot so a team can take more of them without turning every miss into a crisis. You do not need 82% of the votes to hold a line against bad influence. You need conviction on the few things that matter and a cheap enough way to test everything else that missing four times in ten does not end you.

The lobby understood before the market did

What I remember most from that lobby is not the Roadster, though the image is hard to beat. It is the way the engineers reacted when the side boosters landed. Everyone in that room knew how unforgiving hardware is, how many ways a design fails between CAD and production, how one late supplier or one bad assumption about heat or vibration turns a clean plan into months of recovery. That is why the moment hit the way it did. It was not magic to them; it was the visible output of thousands of specific decisions that had somehow survived contact with reality.

The Roadster was impractical, and it was also exactly the kind of impractical decision that tells you how a company really thinks. A normal organization optimizes its demo payload for defensibility. SpaceX optimized it for meaning, contained the risk, and accepted that the center core might not come home. It didn't; the side boosters did; Starman went past Mars, where the Roadster still is, looping the sun about every 557 days. Eight years later the market bought that company at a valuation near $2 trillion while accepting that its founder cannot be removed, which is, when you strip it down, a wager on the same trait that filled that lobby with noise. Whether the wager pays still depends on the question that was already hanging in the room in 2018, before anyone had attached a number to it: whether the misses stay survivable long enough for the wins to compound.

Sources

SpaceX prices record IPO -- NPR on the $135 price and ~$75 billion raise, the largest in history.

SPCX jumps 19% on debut -- CNBC on first-day trading on the Nasdaq.

Ranked: the biggest IPOs in history, and where SpaceX fits -- Visual Capitalist's comparison with Aramco, Alibaba, and Visa.

How Musk increases his power through the IPO -- TechCrunch on the dual-class voting structure (~42% equity, ~82% of the vote).

Top IPO, Weak Governance -- Harvard Law School Forum on Corporate Governance on the offering's investor protections.

Musk gave SpaceX "less than a 10% chance of succeeding" -- Inc. on what Musk told employees before the opening bell.

First flight of the Falcon Heavy -- NASA's account of the February 6, 2018 demo and the Roadster payload.

Falcon Heavy center core toppled after landing -- SpaceNews on the center-core failure and the drone-ship damage.

Starman's first orbit of the sun -- Space.com on the Roadster's heliocentric, beyond-Mars trajectory.

NASA, France skeptical of SpaceX reusable rocket project -- contemporaneous expert doubt about reusability.

Why Musk wants employees to use first principles -- CNBC on the "2% of the cost is materials" reasoning.

Elon Musk's biggest broken promises -- a survey of missed timelines, from FSD to Mars.

From Meta to SpaceX: how dual-class shares keep founders in control -- U.S. News explainer on the structure and its track record.

Frequently Asked Questions

How big was the SpaceX IPO, and what is the ticker?

SpaceX raised about $75 billion in June 2026 at a valuation near $1.75 trillion, making it the largest initial public offering in history, roughly 2.5 times the $29.4 billion Saudi Aramco raised in 2019. It trades on the Nasdaq under the ticker SPCX and rose 19% on its first day.

Does Elon Musk still control SpaceX after it went public?

Yes. SpaceX listed with a dual-class structure in which Class B shares carry ten votes each. According to the company's filings, Musk holds roughly 42% of the equity but around 82% of the voting power, and he can be removed only through a vote he effectively controls. Public investors own the economics but have limited governance say.

What was the Tesla Roadster doing on the Falcon Heavy?

For Falcon Heavy's first test flight on February 6, 2018, SpaceX used Musk's personal cherry-red Tesla Roadster as the demonstration payload, with a spacesuited mannequin nicknamed "Starman" in the driver's seat and "DON'T PANIC" on the dashboard. It was sent into a heliocentric orbit that carries it out past Mars, and it is still in space today.

Did the first Falcon Heavy launch fully succeed?

Mostly, but not entirely. The two side boosters landed simultaneously at Cape Canaveral, but the center core ran low on igniter fluid, relit only one of three engines, and crashed into the ocean near the drone ship at about 300 miles per hour. The mission is remembered as a triumph, though it still missed one of its three planned landings, which is a fair reminder of the real success rate behind the headlines.

Why do founder-led companies like SpaceX tend to outperform?

Research suggests founder-led firms outperform partly because founders with strong control can resist the short-term, consensus-driven pressures that push hired CEOs toward safer choices. One index of S&P 500 companies with active founders beat the rest of the index 3.1 times over 15 years, and a Harvard Business Review study found founder-led firms returned 12% over three years versus negative 26% for non-founder CEOs. The same control that enables bold long-term bets also concentrates risk, which is why dual-class structures remain controversial.

What can operators learn from Musk without copying him?

The practical lesson is about sorting feedback rather than ignoring it. Objections about physics, economics, execution, and convention each deserve a different response: respect the physics, take the economics apart, test the execution quickly and cheaply, and reserve real skepticism for "that's not how it's done." Most companies are better served copying the discipline of fast, cheap learning than the personality or the governance structure.

On February 6, 2018, a few hundred of us crowded into the lobby of Tesla's engineering R&D headquarters in Palo Alto to watch a rocket launch that had nothing to do with our day jobs. SpaceX was about to fly its Falcon Heavy for the first time, and the payload bolted to the top of the rocket was one of ours: a cherry-red Tesla Roadster, with a spacesuited mannequin named Starman in the driver's seat, "DON'T PANIC" on the dash, and David Bowie playing under the broadcast.

Tesla was already an intense place, and people did not stop work lightly. But when the two Falcon Heavy side boosters came down in perfect synchrony at Landing Zones 1 and 2 at Cape Canaveral, the room broke open. Phones went up, people climbed onto chairs, and a crowd of engineers who spent their days fighting millimeters and thermal budgets and supplier tooling sat watching a sports car leave Earth on the most visually absurd demonstration flight anyone had ever approved. I have been in a lot of rooms full of engineers, and I have never been in one quite like that.

The lobby of Tesla's engineering R&D headquarters as Falcon Heavy climbed out, February 6, 2018. Author's photo.

This week, eight years later, the market put a price on what that room felt. SpaceX priced its initial public offering at $135 a share, sold about 555 million shares, and raised roughly $75 billion, the largest IPO in history by a wide margin and around 2.5 times the $29.4 billion Saudi Aramco raised in 2019. It opened on the Nasdaq under the ticker SPCX, closed its first day up 19%, and by this week was trading near $206, a valuation north of $2 trillion. On paper it made Elon Musk the world's first trillionaire.

The number is staggering, but the thing I keep coming back to is what investors agreed to in order to pay it. They bought a company whose founder holds about 82% of the voting power and cannot, in any practical sense, be removed. In most public companies that would be a reason to pay less. At SpaceX it may be part of what they were paying for.

The trait is resistance to influence

Elon is usually described as a once-in-a-generation salesman, the person who can will capital and talent into existence by force of conviction. That is real, but I think it is the less important half of the story. Plenty of founders can raise money, recruit good engineers, and get a room excited. The rarer thing, and the one that actually separates him, is the ability to stay unmoved when credible, qualified people tell him his plan is impossible, impractical, irresponsible, or embarrassing.

Almost everything we did at Tesla, and almost everything the team did at SpaceX, was at the time considered one of those things by people who were, on paper, better positioned to judge. A reusable orbital rocket. A mass-market electric car from a company that had never mass-produced anything. The consensus against these ideas was neither quiet nor stupid; it was grounded in decades of experience. What the work required was the ability to take all of that in and still decide to go.

The resistance runs deeper than ignoring outside critics. Standing in front of SpaceX employees in Texas this month, minutes before he rang the opening bell, Musk said he had given the company "less than a 10% chance of succeeding at all" when he started it, and that he had told people so at the time. His own expected-value math said the rational move was not to try, and he tried anyway. George Bernard Shaw described the type in 1903: "The reasonable man adapts himself to the world; the unreasonable one persists in trying to adapt the world to himself. Therefore all progress depends on the unreasonable man." Musk is, in that specific sense, one of the most unreasonable people alive, and the trait carries a cost I will come back to.

The Falcon Heavy payload is the clearest example I can point to. Strapping your own sports car to the most powerful operational rocket in the world, putting a dummy in a spacesuit behind the wheel, cueing up Bowie, and aiming the whole thing past Mars is not a decision that survives a serious meeting. At Boeing, at Lockheed, at almost any public-company boardroom, the Roadster dies in the first review. Payload review asks for the business case, legal asks about reputational downside, communications asks whether it makes the company look unserious, and finance asks why a test flight needs a cultural artifact. Each objection is reasonable on its own, and together they add up to a no. Most organizations do not kill strange ideas because the people inside them lack imagination. They kill them because every function holds a legitimate veto, and the safest answer is the one nobody will have to defend later.

Two kinds of influence, and most companies confuse them

The usable lesson is narrower than "ignore people," which is both crude and usually wrong. The distinction that matters is between influence on the goal and influence on the execution, and most companies get the two backwards.

On execution, Elon's companies are relentlessly empirical. A rocket either lands or it does not. A battery pack either meets its cost, density, safety, and cycle-life targets or it does not. A supplier either makes the date or it does not. At Tesla a design review could be reduced to mass, cost, thermal performance, manufacturability, and schedule very quickly, and vague confidence did not last long against the numbers. On goals he is nearly immovable. Reusable rockets should exist; electric cars should be mass-market products; a private company should be able to fly NASA astronauts. None of that softened because incumbents found it naive.

Most companies run the opposite way. They accept influence on the goal, letting consensus quietly shrink the ambition, and then they resist influence on the execution, defending the original plan long after the facts have changed. Protecting the goal while staying honest about the plan is the harder discipline, and it is rare. Reusability is the clearest case. In 2014, NASA and France's CNES were openly skeptical that SpaceX could ever make booster recovery economical, and Stanford's Scott Hubbard called reusability "a holy grail," a phrase that captured how long the field had wanted it and how hard it had proven. Musk's response amounted to a should-cost analysis run at the scale of an industry: a rocket is aluminum-lithium, carbon fiber, titanium, copper, avionics, engines, and propellant, and he has said the raw materials run on the order of 2% of the traditional launch price. If that is even directionally true, the question stops being why rockets are expensive and becomes which part of the cost is physics and which part is markup, risk posture, and inherited practice. The same move underpins serious cost-down work in any industry. He resisted the conclusion, not the engineering.

An honest ledger: four misses for every world-changing six

Roughly four of every ten things these companies attempt fail outright or slip by years. I do not read that as an embarrassment so much as the price of the strategy, and admirers and critics both tend to misunderstand it.

The misses are real and worth listing plainly. Hyperloop has no working commercial system more than a decade after the proposal. The Cybertruck arrived years late, missed its original $40,000 price, and has had recalls. Full Self-Driving was promised at Level 5 on timelines that did not hold, and as of last year was still a supervised Level 2 system. Humans were supposed to be on Mars by 2024, the realistic date is now 2028 at the earliest, and Starship has spent years turning test articles into fireballs. Measured only on whether he hits the dates he announces, Musk is unreliable, and the people who say so are correct.

The wins sit on the other side of the same ledger. Reusable boosters were a fantasy until a Falcon 9 landed back at Cape Canaveral in December 2015, and by 2022 NASA's own science chief was saying he preferred to fly on flight-proven boosters, a full reversal of the 2014 consensus. SpaceX now puts more mass into orbit than every other provider on Earth combined. Crew Dragon returned human spaceflight to American soil in 2020. Starlink put working internet over places that had never had it. At Tesla, the Model 3 ramp that Musk called "production hell" drew a Moody's downgrade to junk in March 2018 and a public prediction from former GM vice-chairman Bob Lutz that the company was "headed for the graveyard," and it went on to become the best-selling electric car in the world.

What makes the trade worth taking has little to do with the hit rate and a lot to do with the shape of the payoffs. The downside of an unreasonable bet is bounded, and the upside is not. A failed Hyperloop costs a white paper and some embarrassment, while a working reusable rocket permanently lowers the cost of reaching orbit for everyone who comes after it. If four bets in ten fail and six change the world, the math favors making the bet, as long as you can survive the four. Most people and most companies cannot survive the four, financially or reputationally, and that is the real reason most of them never make it. The same logic ran through the best wartime production programs and through the challengers trying to develop on China-time cycles today, where the willingness to attempt the inadvisable, quickly, is the edge.

Starman and the Roadster on the live feed, watched from the Tesla lobby. Author's photo.

Why the misses don't sink the company

What turns all of this into value instead of wreckage is that the misses are built to be survivable, and that is the part the mythology tends to flatten.

Falcon Heavy's first flight shows it well, because even the triumph contained a failure. The side boosters landed together and produced one of the most memorable aerospace images of the decade. The center core did not. It ran low on TEA-TEB igniter fluid, relit only one of three engines, missed the drone ship Of Course I Still Love You, and hit the Atlantic at about 300 miles per hour roughly 100 meters away, throwing shrapnel across the deck and knocking out two of the ship's thrusters. The most iconic launch of the decade still missed a third of its landing. A clean retelling leaves that out, but the failure is the instructive part, because the mission was structured so that it did not erase the learning or the narrative. The side boosters proved one thing, the payload proved another, and the center core produced a specific failure mode and a list of fixes. The failure was not avoided so much as contained, made specific, and paid for by the parts that worked.

Convexity like that is easy to claim and hard to earn. "We take big swings" is not a strategy, and a big swing with no instrumentation is just a gamble. A big swing with staged tests, clear failure modes, fast supplier response, and a balance sheet that can absorb the loss is a different thing, and SpaceX nearly proved the fatal version of it firsthand. Falcon 1 failed three times before its fourth flight reached orbit on September 28, 2008, with the company almost out of money, and weeks later NASA's commercial cargo contract, worth about $1.6 billion, changed its survival math. That contract did not make the engineering any easier, but it kept the company alive long enough to keep taking shots. The unreasonable founder matters, and so do the contracts, customers, engineers, and suppliers who keep the system solvent long enough for the unreasonable bet to be tested. SpaceX's president, Gwynne Shotwell, is widely credited with talking Musk out of his least workable deadlines, and Musk himself eventually conceded that the heavy automation at Tesla had been a mistake and that he had underrated the people on the line. Resisting influence on the goal is necessary, but on its own it is not enough, and it is never free.

What investors were actually buying

SpaceX did not go public the way most companies do. It listed with a dual-class structure in which Class B shares carry ten votes each. According to the S-1, Musk holds roughly 42% of the equity but about 82% of the voting power, and he can be removed only by a vote he himself controls. For practical purposes, he is not removable.

Most of the machinery of a public company exists to prevent exactly that situation. Boards, independent directors, shareholder votes, and the rest are there to constrain the chief executive and to protect investors from one person's mistakes. Governance specialists looked at the SpaceX offering and saw that machinery missing. Harvard Law School's corporate governance forum analyzed it under the headline "Top IPO, Weak Governance," research from the European Corporate Governance Institute finds that the valuation premium on dual-class firms tends to decay into a discount seven to nine years after listing, and the S&P 500 stopped admitting new dual-class companies back in 2017 for this reason. The concerns are legitimate, and concentrated control genuinely does reduce accountability and create key-person risk.

The complication is that the same control is where the company's ambition comes from. The reusable rockets, the Roadster, the refusal to treat the launch industry's cost structure as fixed, all of it grew out of one person being able to overrule the people who would have said no. The thing the governance machinery is built to prevent is, in this case, the thing that built the company. So it is worth asking whether investors paid a near-$2 trillion valuation despite Musk's control or because of it. In most companies, oversight is the product on offer, the assurance that no single person can drive the whole enterprise into a wall. At SpaceX, the adventure is the product, and the adventure has only ever come from his hands being untied. Read that way, a valuation that high on a company whose founder cannot be removed looks less like a bet on an aerospace business and more like a bet on Elon himself, with his control treated as an asset rather than a discount.

There is some history behind that kind of bet. As a group, founder-led companies have earned a premium: an index of S&P 500 firms with active founders has beaten the rest by a factor of 3.1 over 15 years, and a Harvard Business Review analysis found founder-led firms returned 12% over three years against negative 26% for companies run by hired CEOs. The market has rewarded conviction-plus-control before. The catch is the one the ECGI data points to and the one every key-person discount is built around: you are betting that the person stays right, and that he stays at all. That is a different risk than most public investors are used to underwriting, and the SpaceX IPO is the largest version of it anyone has ever sold.

SpaceX's $75 billion raise dwarfs every prior IPO. Source: Visual Capitalist; Reuters; company filings (2026).

What this means if you're not Elon

"Resist all influence" is terrible advice for almost everyone, because most unreasonable bets really are wrong and most people pushing back on your idea are right. The usable version is narrower: build a way of working that sorts pushback into a few kinds and treats each differently.

Objections from physics deserve immediate respect, because if the thermal model says the pack will not survive the duty cycle, no amount of conviction changes that. Objections from economics deserve to be taken apart, because when a supplier quotes a part at $180 you need to know how much of that is material, cycle time, scrap, amortized tooling, margin, or risk premium, which is the daily work of should-cost and cost-down analysis. Objections from execution deserve a fast, cheap test rather than an argument, so if the team says a supplier cannot hit a date, run the tooling and the approval path to ground and shorten the loop between a decision and its result. Objections from convention deserve the most scrutiny of all, because "that is not how this is done" is sometimes hard-won wisdom and sometimes just inherited habit. Most of the skill is in telling those four apart.

This matters most for challengers. The larger incumbent has more capital, more suppliers, more installed process, and more people whose job is to prevent visible mistakes, and its one structural disadvantage is cycle time. A smaller company can decide on Monday, see supplier feedback on Wednesday, and change the design before the incumbent has finished routing the first approval. That is the same edge operators carry when they move from automotive into aerospace and defense, and it is why manufacturing capability increasingly reads as a strategic weapon rather than a back office, something I have written about in the context of defense and the factory floor. At LightSource we work with these challenger manufacturers, the ones running new-product timelines that look impractical from the outside, and the job is to lower the cost of each shot so a team can take more of them without turning every miss into a crisis. You do not need 82% of the votes to hold a line against bad influence. You need conviction on the few things that matter and a cheap enough way to test everything else that missing four times in ten does not end you.

The lobby understood before the market did

What I remember most from that lobby is not the Roadster, though the image is hard to beat. It is the way the engineers reacted when the side boosters landed. Everyone in that room knew how unforgiving hardware is, how many ways a design fails between CAD and production, how one late supplier or one bad assumption about heat or vibration turns a clean plan into months of recovery. That is why the moment hit the way it did. It was not magic to them; it was the visible output of thousands of specific decisions that had somehow survived contact with reality.

The Roadster was impractical, and it was also exactly the kind of impractical decision that tells you how a company really thinks. A normal organization optimizes its demo payload for defensibility. SpaceX optimized it for meaning, contained the risk, and accepted that the center core might not come home. It didn't; the side boosters did; Starman went past Mars, where the Roadster still is, looping the sun about every 557 days. Eight years later the market bought that company at a valuation near $2 trillion while accepting that its founder cannot be removed, which is, when you strip it down, a wager on the same trait that filled that lobby with noise. Whether the wager pays still depends on the question that was already hanging in the room in 2018, before anyone had attached a number to it: whether the misses stay survivable long enough for the wins to compound.

Sources

SpaceX prices record IPO -- NPR on the $135 price and ~$75 billion raise, the largest in history.

SPCX jumps 19% on debut -- CNBC on first-day trading on the Nasdaq.

Ranked: the biggest IPOs in history, and where SpaceX fits -- Visual Capitalist's comparison with Aramco, Alibaba, and Visa.

How Musk increases his power through the IPO -- TechCrunch on the dual-class voting structure (~42% equity, ~82% of the vote).

Top IPO, Weak Governance -- Harvard Law School Forum on Corporate Governance on the offering's investor protections.

Musk gave SpaceX "less than a 10% chance of succeeding" -- Inc. on what Musk told employees before the opening bell.

First flight of the Falcon Heavy -- NASA's account of the February 6, 2018 demo and the Roadster payload.

Falcon Heavy center core toppled after landing -- SpaceNews on the center-core failure and the drone-ship damage.

Starman's first orbit of the sun -- Space.com on the Roadster's heliocentric, beyond-Mars trajectory.

NASA, France skeptical of SpaceX reusable rocket project -- contemporaneous expert doubt about reusability.

Why Musk wants employees to use first principles -- CNBC on the "2% of the cost is materials" reasoning.

Elon Musk's biggest broken promises -- a survey of missed timelines, from FSD to Mars.

From Meta to SpaceX: how dual-class shares keep founders in control -- U.S. News explainer on the structure and its track record.

Frequently Asked Questions

How big was the SpaceX IPO, and what is the ticker?

SpaceX raised about $75 billion in June 2026 at a valuation near $1.75 trillion, making it the largest initial public offering in history, roughly 2.5 times the $29.4 billion Saudi Aramco raised in 2019. It trades on the Nasdaq under the ticker SPCX and rose 19% on its first day.

Does Elon Musk still control SpaceX after it went public?

Yes. SpaceX listed with a dual-class structure in which Class B shares carry ten votes each. According to the company's filings, Musk holds roughly 42% of the equity but around 82% of the voting power, and he can be removed only through a vote he effectively controls. Public investors own the economics but have limited governance say.

What was the Tesla Roadster doing on the Falcon Heavy?

For Falcon Heavy's first test flight on February 6, 2018, SpaceX used Musk's personal cherry-red Tesla Roadster as the demonstration payload, with a spacesuited mannequin nicknamed "Starman" in the driver's seat and "DON'T PANIC" on the dashboard. It was sent into a heliocentric orbit that carries it out past Mars, and it is still in space today.

Did the first Falcon Heavy launch fully succeed?

Mostly, but not entirely. The two side boosters landed simultaneously at Cape Canaveral, but the center core ran low on igniter fluid, relit only one of three engines, and crashed into the ocean near the drone ship at about 300 miles per hour. The mission is remembered as a triumph, though it still missed one of its three planned landings, which is a fair reminder of the real success rate behind the headlines.

Why do founder-led companies like SpaceX tend to outperform?

Research suggests founder-led firms outperform partly because founders with strong control can resist the short-term, consensus-driven pressures that push hired CEOs toward safer choices. One index of S&P 500 companies with active founders beat the rest of the index 3.1 times over 15 years, and a Harvard Business Review study found founder-led firms returned 12% over three years versus negative 26% for non-founder CEOs. The same control that enables bold long-term bets also concentrates risk, which is why dual-class structures remain controversial.

What can operators learn from Musk without copying him?

The practical lesson is about sorting feedback rather than ignoring it. Objections about physics, economics, execution, and convention each deserve a different response: respect the physics, take the economics apart, test the execution quickly and cheaply, and reserve real skepticism for "that's not how it's done." Most companies are better served copying the discipline of fast, cheap learning than the personality or the governance structure.

Read more

Source Code Episode 9: Source Code: Shashi Mandapaty, Former Chief Procurement Officer at Johnson & Johnson, on Why One Throne Isn't Enough

Source Code Episode 8: Running on Paper: Rick McDonald, Chief Supply Chain Officer at Clorox, on Why Supplier Trust Is the Real Business Continuity Plan

The IEEPA Ruling Wasn't a Win. Here's What Procurement Leaders Are Missing.

Read more

Source Code Episode 9: Source Code: Shashi Mandapaty, Former Chief Procurement Officer at Johnson & Johnson, on Why One Throne Isn't Enough

Source Code Episode 8: Running on Paper: Rick McDonald, Chief Supply Chain Officer at Clorox, on Why Supplier Trust Is the Real Business Continuity Plan

The IEEPA Ruling Wasn't a Win. Here's What Procurement Leaders Are Missing.

Read more

Source Code Episode 9: Source Code: Shashi Mandapaty, Former Chief Procurement Officer at Johnson & Johnson, on Why One Throne Isn't Enough

Source Code Episode 8: Running on Paper: Rick McDonald, Chief Supply Chain Officer at Clorox, on Why Supplier Trust Is the Real Business Continuity Plan

The IEEPA Ruling Wasn't a Win. Here's What Procurement Leaders Are Missing.

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Trusted by:

Trusted by:

Trusted by:

*GARTNER is a registered trademark and service mark of Gartner, Inc. and/or its affiliates in the U.S. and internationally, and COOL VENDORS is a registered trademark of Gartner, Inc. and/or its affiliates and are used herein with permission. All rights reserved. Gartner does not endorse any vendor, product or service depicted in its research publications, and does not advise technology users to select only those vendors with the highest ratings or other designation. Gartner research publications consist of the opinions of Gartner’s research organization and should not be construed as statements of fact. Gartner disclaims all warranties, expressed or implied, with respect to this research, including any warranties of merchantability or fitness for a particular purpose.